Yahoo Finance

Yahoo Finance Vulcan (VMC) Q1 Earnings Beat, Adjusted EBITDA Margin Up

Vulcan Materials Company VMC reported better-than-expected results for the first quarter of 2024, wherein earnings and revenues surpassed their respective Zacks Consensus Estimate. On a year-over-year basis, both metrics decreased year over year due to lower Aggregate shipments.

Shares of the company gained 0.7% in the pre-market trading session on May 2, after the earnings release.

Inside the Headlines

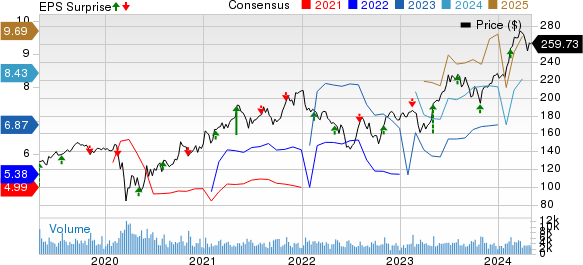

Adjusted earnings of 80 cents per share beat the consensus mark of 76 cents by 5.3% but decreased 15.8% from the year-ago level of 95 cents.

Vulcan Materials Company Price, Consensus and EPS Surprise

Vulcan Materials Company price-consensus-eps-surprise-chart | Vulcan Materials Company Quote

Total revenues of $1.55 billion topped the consensus mark of $1.53 billion by 1.3% but decreased 6.2% year over year.

Segments in Detail

Aggregates

Revenues from the segment were down 0.4% year over year to $1.29 billion. Aggregate shipments (volumes) declined 7.1% year over year to 48.1 million tons. We expected Aggregate revenues of $1.31 billion on 49.7 million tons of shipments.

Freight-adjusted average sales price rose 10.2% to $20.59 per ton from the prior-year level of $18.69. Our estimate for the same was $20.73 per ton. Freight-adjusted revenues rose 2.4% from the prior-year quarter to $991.4 million.

Gross profit of $305 million inched up from the prior-year figure of $302 million. Cash gross profit per ton improved to $8.86 from $8.03, backed by continued pricing momentum and solid execution despite lower shipments due to unfavorable weather conditions for most of the quarter.

Asphalt and Concrete

Revenues from the Asphalt segment were $186.2 million, up 9.7% year over year. The segment generated a solid gross profit of $4.7 million compared with $0.8 million a year ago. Volumes grew 3%, and prices improved 6% year over year. Strong shipments in Arizona and California (its largest asphalt markets) were partially offset by lower shipments in Texas due to inclement weather. We expected Asphalt revenues of $239.8 million.

Total revenues from the Concrete segment were $148.3 million, down 48% year over year. Gross profit totaled ($3.1) million compared with ($2.4) million in the year-ago period. Shipments fell to 0.8 million cubic yards from 1.8 million cubic yards year over year. Average selling prices increased 13.3% from the prior-year level. We expected Concrete revenues of $266.4 million.

Operating Highlights

Selling, administrative and general (SAG) expenses — as a percentage of total revenues — rose 130 basis points to 8.4% from a year ago.

Adjusted EBITDA margin was up 40 bps to 20.9% year over year.

Financials

As of Mar 31, 2024, cash and cash equivalents were $292.4 million, down from $931.1 million at 2023-end. Long-term debt was $3.33 billion at March-end, down from the 2023 level of $3.88 billion.

At March-end, total debt to trailing-12-months adjusted EBITDA was 1.7x, down from 1.9x at the end of 2023.

For the first quarter, net cash provided by operating activities was $173.4 million compared with $221.3 million a year ago.

2024 Guidance Maintained

Vulcan anticipates adjusted EBITDA in the range of $2.15-$2.30 billion (up from $2.01 billion in 2023) and net earnings of $1.07-$1.19 billion versus $933 million in the prior year.

SAG expenses are expected to be in the range of $550-$560 million (versus $543 million in 2023), with interest expenses of approximately $155 million, depreciation, depletion, accretion, and amortization expenses of nearly $610 million, and an effective tax rate of 22-23%.

In the Aggregates segment, cash gross profit per ton is likely to improve from the 2023 level of $9.46. Total shipments are likely to be flat to down 4%, freight-adjusted price growth is likely to be in the range of 10-12% and freight-adjusted cash cost is estimated to increase by mid-single digits.

In the Asphalt, Concrete and Calcium segment, cash gross profit is expected to be $275 million. Asphalt is anticipated to contribute nearly 70% of non-aggregates cash gross profit, while Concrete is likely to add approximately 30% of the same.

The company expects capital expenditures between $625 million and $675 million for maintenance and growth projects.

Zacks Rank & Recent Construction Releases

VMC currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Martin Marietta Materials, Inc. MLM reported mixed results for first-quarter 2024, with earnings surpassing the Zacks Consensus Estimate but revenues missed the same. Both the top and bottom lines decreased on a year-over-year basis.

Going forward, MLM anticipates record federal-level and state-level infrastructure investments, large-scale heavy industrial activity, data centers, and energy projects to offset softer residential and warehouse construction demand, as well as anticipated moderation in light non-residential activity. Impressively, MLM increased full-year adjusted EBITDA guidance to $2.37 billion at the midpoint.

EMCOR Group, Inc. EME reported impressive results for the first quarter of 2024. Its earnings surpassed the Zacks Consensus Estimate and increased year over year, backed by its focus on operational excellence.

Revenues also grew from the previous year due to a continued strong mix and pipeline of projects in large and growing market sectors with long-term secular trends, including high-tech and traditional manufacturing and network & communications.

Weyerhaeuser Company WY reported mixed results for first-quarter 2024. Its earnings beat the Zacks Consensus Estimate but net sales missed the same.

On a year-over-year basis, both metrics declined due to lower fee harvest volumes in the West, a decrease in domestic sales volumes as well as sales realizations accompanied by increased lumber manufacturing and raw materials costs. Also, export sales volumes were softer, especially in China.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Weyerhaeuser Company (WY) : Free Stock Analysis Report

Vulcan Materials Company (VMC) : Free Stock Analysis Report

EMCOR Group, Inc. (EME) : Free Stock Analysis Report

Martin Marietta Materials, Inc. (MLM) : Free Stock Analysis Report