Yahoo Finance

Yahoo Finance 3 Great Stocks to Buy on the Dip in July Down At Least 30%

Today’s episode of Full Court Finance at Zacks dives into where the market stands heading into July and the second half of 2024. The episode then explores three hard-hit S&P 500 stocks—Lululemon (LULU), ON Semiconductor (ON), and Ulta Beauty, Inc. (ULTA)—trading at least 30% below their highs that investors might want to buy on the dip to start the third quarter.

The stock market’s boring two-day stretch on Wednesday and Thursday came after the S&P 500 and the Nasdaq bounced back on Tuesday to end a three-session skid.

The Nasdaq found buyers before it had to test its 21-day moving average. The question is whether the bulls race to fresh highs before the start of Q2 earnings season, or take more profits heading into the Fourth of July?

Thankfully, no matter what happens in the near term, the Wall Street bulls have the two biggest driving forces propelling them forward: earnings growth and rate cuts.

Investors should focus on taking advantage of the next market pullback whenever it comes and look for strong stocks that have already been punished for fading earnings outlooks and other near-term headwinds in the first half of 2024.

Lululemon (LULU)

Lululemon has tumbled 40% in 2024 for the worst performance in the S&P 500. Wall Street is worried about slowing growth in a key demographic amid challenges from rivals Alo and Vuori and changing fashion trends. The athleisure firm is coming up against a very difficult to compete against stretch of growth and the law of large numbers means its YoY expansion won’t look as impressive.

Image Source: Zacks Investment Research

These are real concerns and LULU’s outlook showcases significantly lower sales and EPS growth. But Lululemon averaged 25% sales expansion in the past five years and grew its adjusted EPS by 27% last year and 30% in 2022. Lululemon is projected to post 11.4% revenue growth in FY24 and 10% higher sales next year to boost its adjusted EPS by 12% and 10%, respectively.

Lululemon is set to make up for slowing growth in its U.S. women’s segment by doubling men's and e-commerce and quadrupling international sales between 2021 and 2026. Lululemon’s margins remain almost unmatched in the nonluxury apparel space. On top of that, LULU’s FY24 and FY25 earnings estimates remain above where they were 12 months ago.

Image Source: Zacks Investment Research

LULU has climbed 660% in the past 10 years to blow away the S&P 500’s 190%, Nike’s (NKE) 140%, and its industry’s 18% downturn. Yet, Lululemon trades 40% below its peaks in terms of price and at a 70% discount to its highs at 20.5X forward earnings, which is near its decade-long lows.

Lululemon appears to be finding support around its lows over the last four years while trading at historically oversold RSI levels. Plus, it has no debt and boosted its stock buyback program by $1 billion.

Ulta Beauty (ULTA)

Ulta Beauty is the largest specialty U.S. beauty retailer. The firm reshaped the industry over the last 30-plus years by bringing the entire cosmetic and beauty space under one roof. Ulta sells an array of brands across multiple areas and price points from higher-end companies to its store brands.

Ulta operates roughly 1,400 locations across the U.S. Ulta’s e-commerce offerings have gained traction and it’s benefitting from growth in how-to-style videos, tips, and tutorials across social media and beyond.

Image Source: Zacks Investment Research

Ulta shares soared off their Covid lows until they tumbled between May 2023 and October 2023. Ulta went on another massive boom and bust run that sent it to fresh highs in March 2024.

The stock has plummeted 33% since then, driven lower by slowing comparable sales growth as consumers pullback on spending. Ulta’s lower-income shoppers are being hit hard by inflation and are fading after several years of blowout spending.

Ulta’s consensus earnings estimates for FY24 and FY25 are down just 3.5% over the last year. On top of that, beauty is historically resilient during economic uncertainty when people choose to spend money on the little things. Ulta is projected to post 3% revenue growth in FY24 and 6% higher sales next year, while its adjusted EPS dips slightly this year and jumps 11% higher next year.

Image Source: Zacks Investment Research

Ulta shares are up 13% in the last three years vs. the Zacks Retail sector’s 7% drop. This is part of a 300% run the last decade to destroy the benchmark and its sector. Ulta trades 32% below its highs and 25% under its average Zacks price target.

Ulta appears to be finding support at its lows over the last three years as it hovers just below its 200-week moving average and at historically oversold levels. Ulta also trades at a 60% discount to its highs and 35% below its sector at 14.4X forward earnings (lowest levels outside of the Covid selloff).

ON Semiconductor (ON)

ON Semiconductor operates in the important but less flashy analog segment of the chip industry. ON Semiconductor’s solutions play key roles in the industrial and automotive markets.

ON has thrived in the connected vehicle world and expanded on the back of EVs, energy storage, solar energy, and much more. “As power continues to play a critical role in the world’s increasing energy demands, efficiency is paramount, and we are positioned to continue to gain share with our portfolio of industry-leading power and sensing technologies,” CEO Hassane El-Khoury said last quarter.

Image Source: Zacks Investment Research

ON Semiconductor has been rocked by a cyclical downturn across the industrial and automotive sectors. ON’s fiscal 2024 earnings estimate has tumbled 24% over the last 12 months, with its FY25 outlook 17% lower.

ON Semiconductor’s adjusted FY24 earnings are projected to fall 26% YoY on 13% lower sales. This downturn isn’t uncommon in the historically cyclical industry, and ON is projected to post 10% revenue growth next year and 27% higher adjusted EPS.

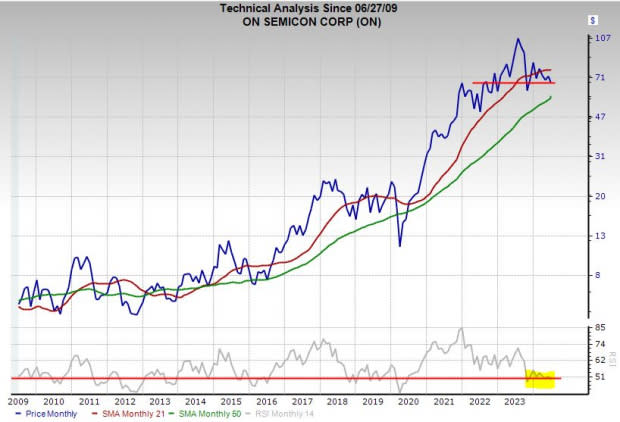

ON Semiconductor shares have fallen around 37% from their 2023 peaks. ON is down 25% over the last year vs. Tech’s 40% run and the Zacks Semiconductor market’s 110% AI-fueled boom. The recent divergence means ON lags firmly behind the chip industry over the past 10 years. Still, its 630% run nearly doubles the Tech sector.

Image Source: Zacks Investment Research

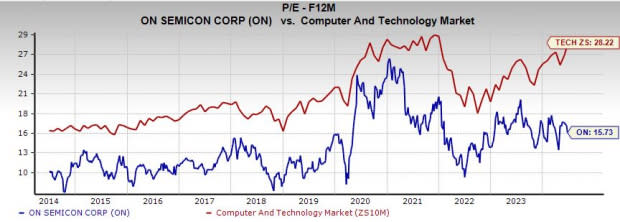

ON trades around where it was in late 2021 and 24% below its average Zacks price target. ON Semiconductor trades between its 21-month and 50-month moving averages and below neutral RSI levels. ON stock trades 40% below its highs, 60% below the chip industry, and at a 45% discount to the Zacks Tech sector.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

NIKE, Inc. (NKE) : Free Stock Analysis Report

Ulta Beauty Inc. (ULTA) : Free Stock Analysis Report

lululemon athletica inc. (LULU) : Free Stock Analysis Report

ON Semiconductor Corporation (ON) : Free Stock Analysis Report