Yahoo Finance

Yahoo Finance 3 High-Yield Stocks at Rock-Bottom Prices

High-yield stocks generally have high yields for a reason; for instance, the stock price has dropped because things are going wrong with the business. But fickle Mr. Market sometimes overreacts to the problems a company is facing. That appears to be the case with telecom giant Verizon Communications (NYSE: VZ), drugmaker AbbVie (NYSE: ABBV), and retail property owner Tanger Factory Outlet Centers (NYSE: SKT). Wall Street's negative sentiment, however, might be your opportunity to pick up a few fat dividend yields.

Still the best of breed in telecom

Brian Stoffel (Verizon Communications): Before starting, it's worth noting that I'm not a dividend investor. I still have three decades before calling upon my retirement funds, and I'm more focused on small, fast-growing disruptive companies.

That said, if I was nearing retirement, Verizon would be on the top of my list of stocks to invest in. The price is a relative bargain; the dividend is safe, large, and sustainable; and the company has an edge over the competition.

Image source: Getty Images.

Verizon's attempts at branching out of its core communications mission -- through acquisitions of AOL and parts of Yahoo! -- have largely failed. Having acknowledged that, we can focus on what Verizon does best: connecting people with high-speed internet and mobile service.

Verizon is the first to market with 5G, and it has the largest market share in mobile subscription plans in the nation. It has either been tied -- with AT&T -- or in the lead in market share every quarter for over five years.

And it's hard to argue with a 4% dividend yield. Over the past year, that payout has only eaten up 55% of the company's $17.7 billion in free cash flow. That means the dividend is relatively safe and has room for growth. Verizon stock also trades for 14 times that free cash flow figure -- a more-than-fair price for a market leader.

Arguably the best big pharma stock on the market

Keith Speights (AbbVie): I can't think of a big pharma stock that checks off as many boxes as AbbVie does. Actually, it's hard for me to think of many stocks in any industry that deliver the full package like AbbVie.

Let's start with the dividend. AbbVie's dividend currently yields nearly 5.4%. That high yield shouldn't be in any jeopardy given the drugmaker uses only around 45% of its free cash flow to fund the dividend program. AbbVie certainly prioritizes its dividend, having increased it 168% since being spun off from parent Abbott Labs in 2013.

AbbVie stock is also dirt cheap. Shares trade at around 8.4 times expected earnings. This discounted price tag stems primarily from the fact that some investors are worried about declining sales for AbbVie's top-selling drug, Humira, in the face of biosimilar competition in Europe. However, the company appears to have a solid plan to transition beyond Humira over the coming years.

One key part of that transition is AbbVie's current lineup, including fast-growing cancer drugs Imbruvica and Venclexta. It also has a rising star in endometriosis drug Orilissa. But the crown jewels are in the company's pipeline, with approvals expected this year for immunology drugs risankizumab and upadacitinib.

Overall, AbbVie thinks that it can generate $35 billion in non-Humira sales by 2025. That's nearly $3 billion more than the drugmaker made in total last year. With its great dividend, bargain price, and solid growth prospects, I think that AbbVie is arguably the best big pharma stock on the market.

Down, but not out

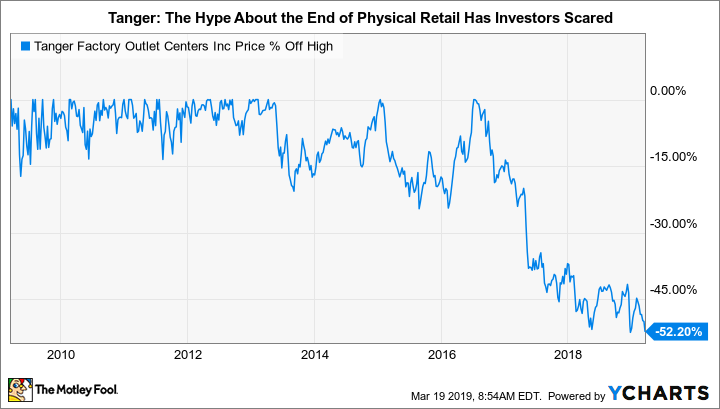

Reuben Gregg Brewer (Tanger Factory Outlet Centers): The shares of real estate investment trust (REIT) Tanger are down roughly 50% from their 2016 peak. Although recent results have been relatively weak, including a slight dip in occupancy at its 44 outlet centers and a 1.3% decline in same-store net operating income in 2018, its performance hasn't been all that bad. The real issue is that investors are worried that Tanger won't be able to weather the so-called "retail apocalypse."

The fear is understandable, but the whole issue is overblown. What's really transpiring is a shift in the way customers shop. This is not the first time this has happened, and, with online shops like Amazon.com increasingly focused on physical stores, it is unlikely that brick-and-mortar malls will disappear. Sure, weaker mall operators could go out of business -- but Tanger is not a weak mall operator.

The company's debt is rated investment grade. Total debt to adjusted assets is just 50%, so Tanger is far from overleveraged. Interest expenses are covered more than five times. And the dividend eats up less than 60% of funds from operations, leaving the REIT plenty of cash to reinvest in its properties and adjust to the changing retail landscape.

The transition at Tanger isn't likely to be a smooth one, as recent results show. But for more aggressive investors, the steep drop in the share price and the historically high 6.9% yield are ample compensation for the uncertainty here. Plus, Tanger has increased its dividend annually for 25 consecutive years, indicating it strongly believes in rewarding investors for sticking around through both the good times and bad.

More From The Motley Fool

John Mackey, CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool's board of directors. Brian Stoffel owns shares of AMZN. Keith Speights owns shares of AbbVie. Reuben Gregg Brewer owns shares of Tanger Factory Outlet Centers. The Motley Fool owns shares of and recommends AMZN. The Motley Fool recommends Tanger Factory Outlet Centers and Verizon Communications. The Motley Fool has a disclosure policy.