Yahoo Finance

Yahoo Finance 3 International Upstream Oil & Gas Stocks You Need to Track

The Zacks Oil and Gas - Exploration and Production - International industry has lately been pegged back by investor skepticism toward risky assets and lower realizations, to go with uncertainties related to slowing global economic growth and inflationary pressures. Although macro challenges are leading to some demand concerns, we think the space still has fuel left in the tank, especially for the operators that target growth opportunities and operating efficiency initiatives. We advise investors to focus on Tullow Oil TUWOY, VAALCO Energy EGY and EnQuest PLC ENQUF.

Industry Overview

The Zacks Oil and Gas - International E&P industry consists of companies primarily operating outside the United States and focused on the exploration and production (E&P) of oil and natural gas. These firms find hydrocarbon reservoirs, drill oil and gas wells, and produce and sell these materials to be refined later into products such as gasoline, fuel oil, distillate, etc. The economics of oil and gas supply and demand is the fundamental driver of this industry. In particular, a producer’s cash flow is primarily determined by the realized commodity prices. In fact, all E&P companies are vulnerable to historically volatile prices in the energy markets. A change in realizations affects their returns on drilling inventory and causes them to alter production growth rates. These operators are also exposed to exploration risks where drilling results are uncertain.

3 Key Investing Trends to Watch in the Oil and Gas - International E&P Industry

Plunging Energy Prices: Energy remains the worst S&P 500 sector this year. The space has witnessed a total return of -11.7% in 2023 against the S&P 500’s gain of around 2.9%. Of late, the going has been particularly tricky for “black gold.” With investors dumping risky assets in the wake of the biggest U.S. bank collapse since 2008 and the Credit Suisse blowup, oil is trading below $70 for the first time since December 2021. It’s not any different for natural gas. The fuel slumped to a 25-year low in June 2020 but hit $10 per MMBtu for the first time since 2008 in August last year. Now, it has gone below $2.50, on adverse weather predictions and concerns that the banking crisis could prompt an economic slowdown that would hurt the consumption of energy.

Effects of High Inflation: Most energy companies (including the upstream operators) have been experiencing rising costs in the form of increased expenses related to maintenance and inventory. The inflationary environment, together with supply-chain tightness, is not only pushing costs higher but also affecting their capital programs. Apart from being hard to ignore, escalation in expenses is also drowning out the benefits of any commodity price increase. In our view, the inflation-associated headwinds will continue to challenge growth and margin numbers with little chance of a quick resolution. Finally, what this means is that the central banks will be persistent with their aggressive policy of raising rates to stem inflation. This may lead to a rough road for oil/gas equities. In particular, worries about weaker energy demand due to the threat of recession (spurred by rising interest rates and slowing consumer spending) might jeopardize the commodity’s ascent.

Companies Prioritizing Returning More Cash to Shareholders: The sharp increase in crude prices last year allowed the upstream operators to deliver a solid financial performance. In particular, cash from operations is on a sustainable path with revenues improving and companies slashing capital expenditures from the pre-pandemic levels amid higher commodity realizations. To put it simply, the environment of strong prices in 2022 helped the E&P firms to generate significant “excess cash,” which they intend to use to boost investor returns. In fact, more and more energy companies are allocating their increasing cash pile by way of dividends and buybacks to pacify the long-suffering shareholders.

Zacks Industry Rank Reflects Bearish Outlook

The Zacks Oil and Gas – International E&P industry is a 9-stock group within the broader Zacks Oil - Energy sector. It currently carries a Zacks Industry Rank #218, which places it in the bottom 12% of around 250 Zacks industries.

The group’s Zacks Industry Rank, which is basically the average of the Zacks Rank of all the member stocks, indicates challenging near-term prospects. Our research shows that the top 50% of the Zacks-ranked industries outperforms the bottom 50% by a factor of more than 2 to 1.

The industry’s position in the bottom 50% of the Zacks-ranked industries is a result of a negative earnings outlook for the constituent companies in aggregate. Looking at the aggregate earnings estimate revisions, it appears that analysts are becoming pessimistic about this group’s earnings growth potential. While the industry’s earnings estimates for 2023 have gone down 48.4% since December, the same for 2024 have fallen 36.1% over the same timeframe.

Despite the dim near-term prospects of the industry, we will present a few stocks that you may want to consider for your portfolio. But it’s worth taking a look at the industry’s shareholder returns and current valuation first.

Industry Underperforms Sector & S&P 500

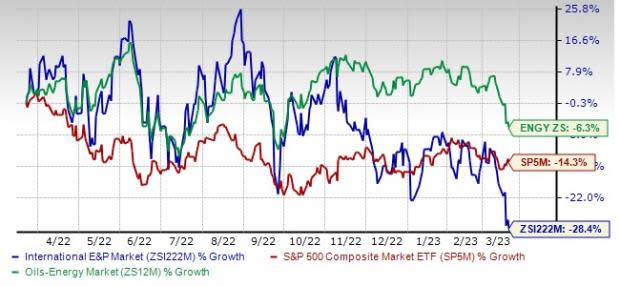

The Zacks Oil and Gas - International E&P industry has fared worse than the broader Zacks Oil - Energy Sector as well as the Zacks S&P 500 composite over the past year.

The industry has fallen 28.4% over this period compared with the broader sector’s decrease of 6.3%. Meanwhile, the S&P 500 has lost 14.3%.

One-Year Price Performance

Industry's Current Valuation

Since oil and gas companies are debt-laden, it makes sense to value them based on the EV/EBITDA (Enterprise Value/ Earnings before Interest Tax Depreciation and Amortization) ratio. This is because the valuation metric takes into account not just equity but also the level of debt. For capital-intensive companies, EV/EBITDA is a better valuation metric because it is not influenced by changing capital structures and ignores the effect of non-cash expenses.

On the basis of the trailing 12-month enterprise value-to EBITDA (EV/EBITDA) ratio, the industry is currently trading at 2.95X, significantly lower than the S&P 500’s 11.90X. However, tt is slightly higher than the sector’s trailing-12-month EV/EBITDA of 2.73X.

Over the past five years, the industry has traded as high as 16.32X, as low as 2.17X, with a median of 6.84X.

Trailing 12-Month Enterprise Value-to EBITDA (EV/EBITDA) Ratio (Past Five Years)

3 Oil and Gas - International E&P Stocks to Watch For

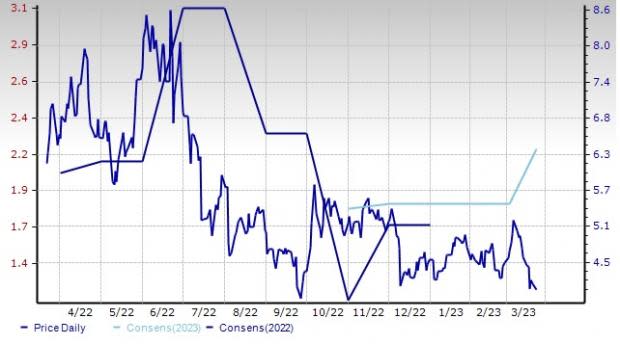

VAALCO Energy: Founded in 1985, VAALCO Energy’s productive capacity is based offshore West Africa, where it focuses on growth through a combination of acquisitions and active drilling. The operator of Gabon offshore Etame license, EGY is known for its operational excellence and cost discipline, which are expected to generate significant free cash flows at current strip pricing.

Valued at around $450.8 million, VAALCO Energy has a trailing four-quarter earnings surprise of roughly 61.8%, on average. EGY currently carries a Zacks Rank #2 (Buy). VAALCO Energy’s shares have lost 35.3% in a year.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Price and Consensus: EGY

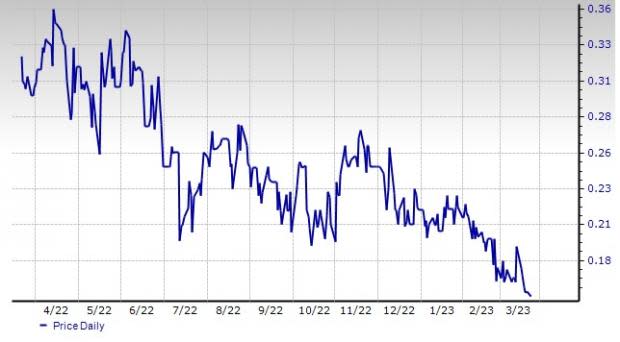

Tullow Oil: Tullow Oil is a London-based hydrocarbon producer and explorer, focusing mainly on Africa. TUWOY’s significant positions in discovered and emerging basins and focus on capital discipline should result in a noticeable improvement in profitability. In particular, the oil and gas finder’s operational excellence and technical expertise stand it in good stead.

The 2023 Zacks Consensus Estimate for TUWOY indicates 32.4% year-over-year revenue growth. Tullow Oil carries a Zacks Rank #3 (Hold). TUWOY’s shares have lost 48.4% in a year.

Price and Consensus: TUWOY

EnQuest: This London-based upstream operator has key operations in the UK North Sea and Malaysia. The company’s impressive production efficiency across the portfolio is at the crux of ENQUF’s growth story. EnQuest has adjusted its capital plans to the prevailing market conditions, resulting in strong operating cash flows. ENQUF also possesses an active hedging program that provides further downside protection from commodity price fluctuations.

The 2023 Zacks Consensus Estimate for EnQuest Energy indicates 30.8% earnings per share growth over 2022. The #3 Ranked ENQUF’s shares are down 38% in a year.

Price and Consensus: ENQUF

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Tullow Oil PLC (TUWOY) : Free Stock Analysis Report

Vaalco Energy Inc (EGY) : Free Stock Analysis Report

EnQuest (ENQUF) : Free Stock Analysis Report