Yahoo Finance

Yahoo Finance 3 Reasons Home Depot Is a Better Dividend Stock Than Walmart

They each pay about the same annual yield that's just above the broader market's 2%. And both Walmart (NYSE: WMT) and Home Depot (NYSE: HD) are successful retailers that dominate their respective niches. However, one stock stands out as preferable for income investors seeking a strong, quickly growing dividend.

Below, we'll look at a few reasons Home Depot wins this dividend stock matchup.

1. Stronger sales growth

Walmart has enjoyed a modest growth rebound lately but its expansion pace isn't in the same league as Home Depot's. The retailing titan's comparable-store sales inched higher by 2% in 2017 to put it modestly ahead of rivals like Target and Kroger, which each grew comps by 1% during the period.

Image source: Getty Images.

Home Depot's comps improved at a blistering 7% last year, which marked an acceleration over the prior year's 6% gain. The retailer isn't simply benefiting from an expanding home improvement industry, either. Rival Lowe's grew comps by just 4% last year, which suggests continued success by the market leader at expanding its market share position.

2. More financial ammunition

Home Depot also stands out both in its own industry and against Walmart when it comes to financial efficiency. Operating margin recently passed 14.5% of sales, compared to 9% for Lowe's. That core profitability figure is climbing, too, while Walmart's has dipped to 4% from 6% five years ago.

WMT Return on Invested Capital (TTM) data by YCharts.

The same trend holds for return on invested capital, which has soared to over 30% for Home Depot while shrinking to single digits for the king of retail.

These financial wins translate into a very different earnings picture for the two companies. Home Depot has seen its net income haul spike to $8.6 billion last year, or 8.6% of sales, from $7 billion, or 7.9% of sales in 2015. Walmart's comparable figure has declined to $13.6 billion, or 2.8% of sales, from $16.2 billion, or 3.3% of sales three years ago.

3. Room for growth

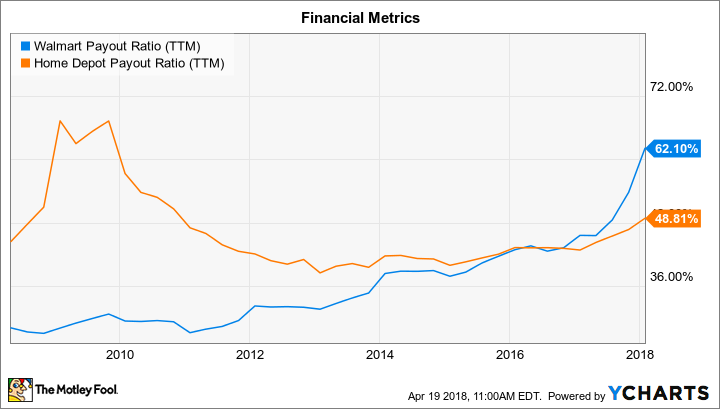

That declining earnings profile means that Walmart executives have fewer resources available to allocate toward annual payout hikes. The retailer's dividend is eating up over 60% of annual profits right now, compared to less than 50% for Home Depot.

WMT Payout Ratio (TTM) data by YCharts.

It's no surprise, then, that Home Depot's income growth far outpaces Walmart's lately. Walmart's management lifted the dividend by roughly 2% in each of the last three fiscal years. Home Depot's raise was 29% this year, 26% in 2017, and 17% in 2016.

Worth the extra risk?

Investors who prize stability might prefer Walmart's dividend since that payout is supported by a larger sales base that doesn't rely on the cyclical housing industry. That stability, after all, has translated into 44 consecutive years of annual dividend raises for Walmart. Home Depot, on the other hand, had to suspend its increases during the worst of the housing market crash.

Yet its business has grown much stronger since the recession, and those gains should support this generous payout through the next cyclical downturn. In the meantime, income investors have every reason to expect continued market-thumping sales and profit growth from Home Depot as the company extends its sales base beyond $100 billion to get closer to Walmart's $486 billion annual haul.

More From The Motley Fool

Demitrios Kalogeropoulos owns shares of Home Depot. The Motley Fool has the following options: short May 2018 $175 calls on Home Depot and long January 2020 $110 calls on Home Depot. The Motley Fool recommends Home Depot and Lowe's. The Motley Fool has a disclosure policy.