Yahoo Finance

Yahoo Finance 3 SGX Stocks That May Be Trading Below Their Estimated Intrinsic Value By Up To 47.2%

As the Singapore market shows signs of robust activity, with innovative companies like Currensea successfully raising significant funds through crowdfunding, it highlights a growing investor confidence and interest in diverse sectors. In this context, identifying stocks that are potentially trading below their intrinsic value could offer attractive opportunities for investors looking to capitalize on current market conditions.

Top 5 Undervalued Stocks Based On Cash Flows In Singapore

Name | Current Price | Fair Value (Est) | Discount (Est) |

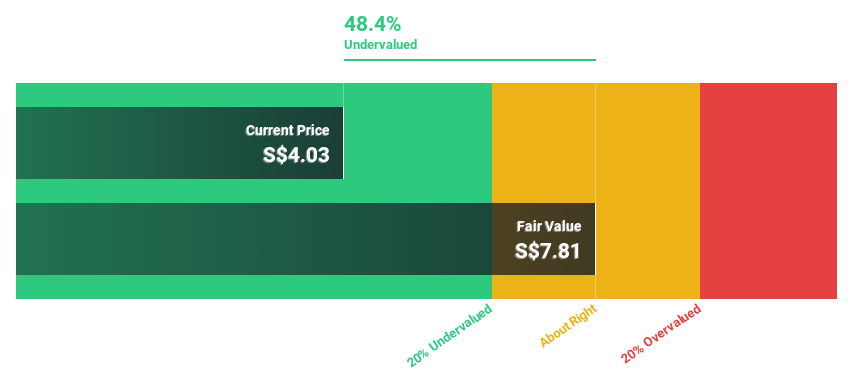

Singapore Technologies Engineering (SGX:S63) | SGD4.29 | SGD8.12 | 47.2% |

LHN (SGX:41O) | SGD0.335 | SGD0.37 | 10.1% |

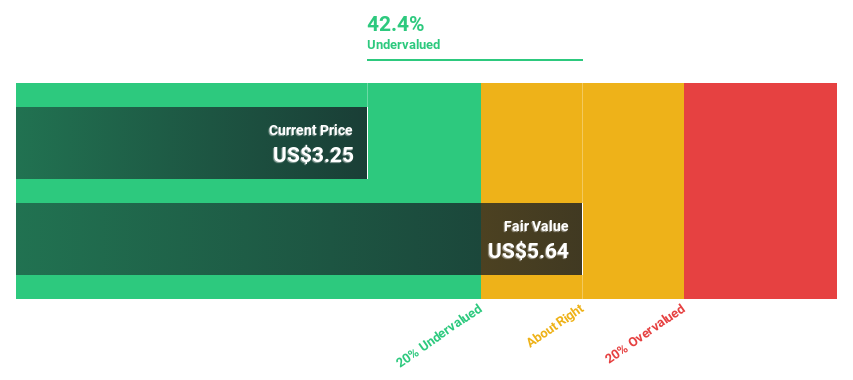

Hongkong Land Holdings (SGX:H78) | US$3.24 | US$5.78 | 43.9% |

Seatrium (SGX:5E2) | SGD1.44 | SGD2.59 | 44.4% |

Frasers Logistics & Commercial Trust (SGX:BUOU) | SGD0.945 | SGD1.65 | 42.9% |

Digital Core REIT (SGX:DCRU) | US$0.58 | US$1.11 | 47.8% |

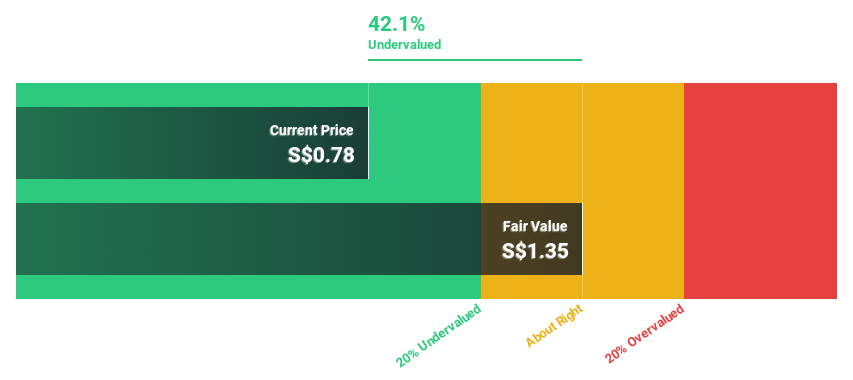

Nanofilm Technologies International (SGX:MZH) | SGD0.83 | SGD1.45 | 42.7% |

Below we spotlight a couple of our favorites from our exclusive screener

Hongkong Land Holdings

Overview: Hongkong Land Holdings Limited operates in property investment, development, and management across Hong Kong, Macau, Mainland China, Southeast Asia, and other international locations with a market capitalization of approximately $7.15 billion.

Operations: The company generates revenue from two main segments: Investment Properties, which brought in $1.08 billion, and Development Properties, contributing $0.76 billion.

Estimated Discount To Fair Value: 43.9%

Hongkong Land Holdings is currently priced at S$3.24, below the estimated fair value of S$5.78, indicating significant undervaluation based on discounted cash flows. Despite a forecasted revenue growth of 4.6% per year, which lags behind the market's top performers, earnings are expected to surge by 43.34% annually over the next three years, suggesting potential for future profitability improvement. However, its low forecasted return on equity at 2.4% and a dividend yield of 6.79%, not well-covered by earnings, reflect some financial vulnerabilities.

Nanofilm Technologies International

Overview: Nanofilm Technologies International Limited operates in the field of nanotechnology solutions across Singapore, China, Japan, and Vietnam with a market capitalization of approximately SGD 540.34 million.

Operations: Nanofilm Technologies International's revenue is generated through four key segments: Sydrogen (SGD 1.05 million), Nanofabrication (SGD 16.05 million), Advanced Materials (SGD 141.54 million), and Industrial Equipment (SGD 37.17 million).

Estimated Discount To Fair Value: 42.7%

Nanofilm Technologies International, with a current price of SGD0.83, is valued below the calculated fair value of SGD1.45, suggesting notable undervaluation. Despite a recent dip in net profit margin to 1.8%, the company forecasts robust revenue growth at 15.1% annually and even stronger earnings growth projected at 50.7% per year, significantly outpacing the Singapore market average. The optimistic financial outlook for FY2024 underpins these expectations, although its forecasted return on equity remains modest at 9%.

Singapore Technologies Engineering

Overview: Singapore Technologies Engineering Ltd is a global technology, defense, and engineering group with a market capitalization of approximately SGD 13.38 billion.

Operations: The company generates revenue from three primary segments: Commercial Aerospace (SGD 3.97 billion), Urban Solutions & Satcom (SGD 1.98 billion), and Defence & Public Security (SGD 4.29 billion).

Estimated Discount To Fair Value: 47.2%

Singapore Technologies Engineering, priced at S$4.29, trades below its estimated fair value of S$8.12, indicating a significant undervaluation based on discounted cash flows. The company's earnings have grown modestly by 1.1% annually over the past five years and are expected to increase by 11.62% per year moving forward. Although it carries a high level of debt, its revenue growth is projected to surpass the Singapore market average at 6.9% per year compared to 3.6%. Recent initiatives include a share buyback program and consistent dividend payments, enhancing shareholder returns despite an unstable dividend track record.

Key Takeaways

Get an in-depth perspective on all 7 Undervalued SGX Stocks Based On Cash Flows by using our screener here.

Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Want To Explore Some Alternatives?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include SGX:H78 SGX:MZH and SGX:S63.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com