Yahoo Finance

Yahoo Finance 3 Stocks for Warren Buffett Fans

Berkshire Hathaway Inc (NYSE: BRK-A)(NYSE: BRK-B) CEO Warren Buffett has few peers as an investor. His half-century career is full of lessons many of us can use to improve our own investing results. The best lesson for most of us is undoubtedly Buffett's maxim, to paraphrase, "buy great businesses at reasonable prices, and hold for as long as possible." This has worked incredibly well for Berkshire investors, who have enjoyed more than 4,000% returns over the past 30 years as Buffett has built one of the strongest, most profitable companies in the world.

If you're looking for the next great "Buffett-style" stocks for your own portfolio, our contributing investors have identified Starbucks Corporation (NASDAQ: SBUX), Brookfield Renewable Partners LP (NYSE: BEP), and Sherwin-Williams Co (NYSE: SHW) as the kinds of companies that fit the Warren Buffett mold. They're reasonably priced, high-quality companies with strong competitive positions -- which Buffett says can lead to wonderful returns for long-term investors.

These stocks could leave you smiling like Warren Buffett. Image source: The Motley Fool.

Could this be the next Coca-Cola?

Jason Hall (Starbucks): When Warren Buffett bought a billion-dollar stake in Coca-Cola (NYSE: KO) for Berkshire Hathaway in the late 1980s, he was able to snap up the shares at a bargain price, but invested with the expectations that Coke, with its powerful brand appeal and decades of success, would continue to be a strong, highly profitable business for many years to come. To say it's worked out well would be a huge understatement. The $1.3 billion Berkshire spent on its stake in Coke is worth $18 billion at recent prices, and it pays Berkshire over $500 million every year in dividends.

It may not seem like it, but Starbucks isn't that far removed from where Coke was when Buffett added it to the Berkshire portfolio. Coca-Cola was a hugely popular brand with global appeal and decades of success already behind it 30 years ago, but early in its international expansion. Today, Starbucks is in a similar situation, with its Americas business generating more than four times as much operating income than its China/Asia Pacific segment.

Image source: Starbucks.

But its Asian business is growing much faster, as Chinese and Southeast Asian economic growth drive a massive expansion in the region's middle class. This is creating an enormous number of new Starbucks consumers, just as past global economic expansion was a big part of adding millions of new Coke drinkers around the world during the 1980s and 1990s.

It may not be trading at the discount Coke was when Buffett invested in that company, but at around 30 times earnings, Starbucks shares are cheaper than they have been over much of the past several years. Also like Coke, Starbucks pays a solid dividend, increasing the payout regularly since inception, and management has made repurchasing shares -- and driving up per-share value -- a priority with excess cash flows.

Between the growth prospects, likelihood of dividend growth, and plans to continue repurchasing shares, fans of Buffett-style investing should give Starbucks a close look.

Covering all the bases

Rich Duprey (Sherwin-Williams): Warren Buffett owns nearly 50 stocks, and he's dumped over $1 billion in almost half of them. But four companies actually account for more than half of his portfolio's holdings: Kraft Heinz, Wells Fargo, Apple, and Coca-Cola. Three of those are dominant consumer-oriented businesses and arguably also meet Buffett's general guideline of being simple businesses to understand.

It's why I think fans of the Oracle would like paint and coverings leader Sherwin-Williams. First, rival Benjamin Moore is a subsidiary of Berkshire Hathaway; it's clear Buffett likes paint. And that could be because paint is something that works well in bull markets, when there's a lot of construction going on, and in bear markets, where consumers can slap on a coat as a cheap, quick, and easy way to spruce up a home. And that's been borne out by Sherwin-Williams' performance.

Image source: Getty Images.

Since 2000, the paint specialist has returned some 1,850% compared to an 80% return by the S&P 500. Although Sherwin-Williams has traditionally been geared more toward the professional painter than the homeowner, with its network of 4,200 independent stores -- just like Benjamin Moore -- its purchase of Valspar helps balance that out.

And as an added bonus, Sherwin-Williams also qualifies as a Dividend Aristocrat because it has raised its payout to shareholders every year since 1979, though the $3.40 dividend does yield only a very modest 0.8%.

In all, Sherwin-Williams looks like a stock that Warren Buffett fans could get behind.

An energy stock Buffett should love

Travis Hoium (Brookfield Renewable Partners): We know that Warren Buffett loves companies that generate consistent cash flows and trade at a reasonable value. Brookfield Energy Partners fits that profile because it owns clean electricity-generating assets around the world and pays a strong dividend, which currently yields 5.7% per share.

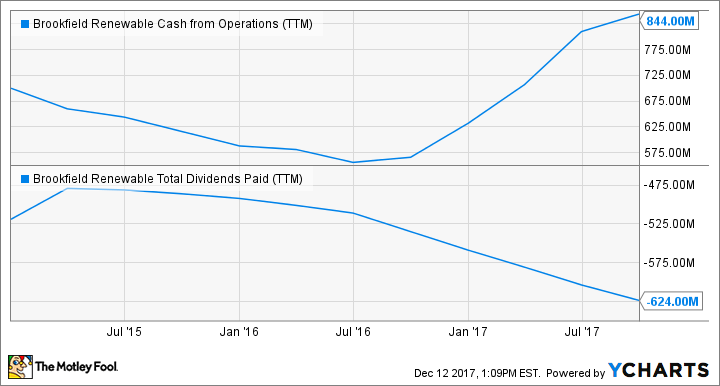

85% of Brookfield Renewable Partners' assets are hydroelectric power plants, which generate predictable cash flows and drive continued growth. Management aims to pay out most of its cash flow in the form of dividends, but it also wants to keep enough cash to grow distributions 5% to 9% organically. You can see below that the company generates more operating cash flow than it pays in dividends, which is what allows for long-term growth.

BEP Cash from Operations (TTM) data by YCharts

Brookfield Renewable Partners also isn't reliant on a low dividend yield to grow, something that hinders most yieldcos, and it's not tied to one form of energy. The company also owns wind assets in Brazil and North America and could be a buyer of solar plants in the future as well. Given Warren Buffett's affinity for companies with strong recurring cash flows and reliable dividends, this is a dividend stock that's great for Buffett fans.

More From The Motley Fool

6 Years Later, 6 Charts That Show How Far Apple, Inc. Has Come Since Steve Jobs' Passing

Why You're Smart to Buy Shopify Inc. (US) -- Despite Citron's Report

Jason Hall owns shares of Apple, Berkshire Hathaway (B shares), Coca-Cola, and Starbucks. Rich Duprey has no position in any of the stocks mentioned. Travis Hoium owns shares of Apple, Berkshire Hathaway (B shares), and Wells Fargo. The Motley Fool owns shares of and recommends Apple, Berkshire Hathaway (B shares), and Starbucks. The Motley Fool has the following options: long January 2020 $150 calls on Apple and short January 2020 $155 calls on Apple. The Motley Fool recommends Sherwin-Williams. The Motley Fool has a disclosure policy.