Yahoo Finance

Yahoo Finance 3 Stocks to Watch From the Mortgage & Related Services Industry

The Zacks Mortgage & Related Services industry continues to suffer from the receding mortgage origination tide. Rising mortgage rates continue to affect mortgage volumes, particularly refinancing. Housing shortages and price appreciation are near-term headwinds for purchase origination.

Despite these, robust servicing opportunities and a focus on improving operating leverage will be saving grace for the mortgage industry players. The focus on investments in mortgage service rights (MSR) and technological enhancements are anticipated to drive Walker & Dunlop, Inc. WD, Velocity Financial, Inc. VEL and Ocwen Financial Corporation OCN.

Industry Description

The Zacks Mortgage & Related Services industry comprises providers of mortgage-related loans, refinancing and other loan-servicing facilities. Numerous banks have been retreating from the mortgage business due to higher compliance and capital requirements. This provided an opportunity for non-banks to increase the capacity to gain market share in the mortgage loans business, which accounts for the largest class of U.S. consumer debt. Players in the industry are somewhat dependent on the interest rates determined by the Federal Reserve, as prevailing rates influence customers' decisions to apply for mortgages. The companies also generate investment income from several financial assets such as residential or commercial mortgage-backed securities, and asset-backed securities. Further, the firms make equity investments in mortgage-related entities, among others.

3 Mortgage & Related Services Industry Trends to Watch

Rising Rates to Hinder Origination Volume: Amid the tight labor markets and all-time high inflation level, the Federal Reserve is in the midst of a shift from quantitative easing to tightening, with a reduction in asset purchases and hiking short-term interest rates. Since the yield curve impacts the path of mortgage rates, the macroeconomic backdrop indicates that mortgage rates will continue to witness an uptick in the upcoming period. This, combined with supply issues and robust home price appreciation over the past two years, has challenged housing affordability. These factors are likely to lead to lower purchase origination volumes and refinancing, as incentives for borrowers to refinance loans are likely to fade. This might impede revenue growth for the industry participants.

Servicing Segment Performance to Improve With Rising Rates: Amidthesignificant declines in gain-on-sale margins and lower loan origination volume, industry players are likely to increase reliance on the service segment for profitability. In a rising rate environment, the servicing segment offers a natural operational hedge to the origination business. We expect MSR tailwinds to accelerate, with companies anticipating significant mark-ups and reduced amortization expenses. With the primary-secondary mortgage spread compression, mortgage originator profitability has declined. This has been incentivizing MSR sales to generate cash returns. Hence, MSR investments are poised to deliver significant value appreciation and offer attractive unlevered yield. Such MSR appreciation can drive the book value.

Operational Enhancements to Provide Respite: Amid the ongoing mortgage market deterioration, industry players have been rationalizing and improving operations. Specifically, companies have resorted to cutting down workforces, and are enhancing technology platforms and user experience for longer-term origination expansions. Moreover, digitization has been helping the industry participants to enhance customer experience, lower costs by saving compensation expenses and reduce the possibility of fraud. Such automation and process enhancements will continue to drive cost savings, productivity and operating leverage amid the industry challenges.

Zacks Industry Rank Reflects Rosy Prospects

The Zacks Mortgage & Related Services industry, housed within the broader Zacks Finance sector, currently carries a Zacks Industry Rank #78, which places it in the top 31% of more than 250 Zacks industries.

The group's Zacks Industry Rank, which is basically the average of the Zacks Rank of all the member stocks, indicates bleak prospects in the near term. Our research shows that the top 50% of the Zacks-ranked industries outperforms the bottom 50% by a factor of more than 2 to 1.

However, looking at the aggregate earnings estimate revisions, it appears that analysts are gradually losing confidence in this group's earnings growth potential. Over the past year, the industry's earnings estimates for the current year have been revised 46.3% downward.

Before we present a few stocks that you may want to consider for your portfolio, let's take a look at the industry's recent stock market performance and the valuation picture.

Industry Underperforms Sector and S&P 500

The Zacks Mortgage & Related Services industry has underperformed the broader Zacks Finance sector and the S&P 500 composite over the past year.

The industry has declined 28.9% in this period, wider than the broader sector's fall of 8.6%. The S&P 500 composite has dipped 7.6% in the past year.

One-Year Price Performance

Image Source: Zacks Investment Research

Industry's Current Valuation

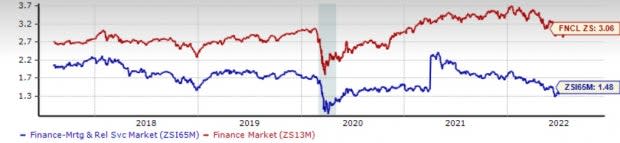

On the basis of the price-to-book ratio (P/B), which is commonly used for valuing mortgage loan providers, the industry currently trades at 1.48X compared with the S&P 500's 5.81X.

Over the last five years, the industry has traded as high as 2.43X, as low as 0.78X, and at the median of 1.48X, as the chart below shows.

Price-to-Book Ratio (TTM)

Image Source: Zacks Investment Research

As finance stocks typically have a lower P/B ratio, comparing mortgage loan providers with the S&P 500 may not make sense to many investors. But a comparison of the group's P/B ratio with that of its broader sector ensures that the group is trading at a decent discount. The Zacks Finance sector's trailing 12-month P/B of 3.06X for the same period is above the Zacks Mortgage & Related Services industry's ratio, as the chart shows below.

Price-to-Book Ratio (TTM)

Image Source: Zacks Investment Research

3 Mortgage & Related Services Stocks to Keep a Close Eye on

Ocwen Financial: The company is a preeminent non-bank mortgage servicer and originator that provides solutions through its primary brands, PHH Mortgage and Liberty Reverse Mortgage. The company’s balanced and diversified business model -- diversified originations sources and servicing business -- provides a competitive advantage against peers.

The company’s servicing financial performance is poised to improve with rising interest rates. The company has also been driving expense reduction and making right-sizing actions. Also, favorable demographics and home price appreciation expected to drive continued growth in reverse mortgage market.

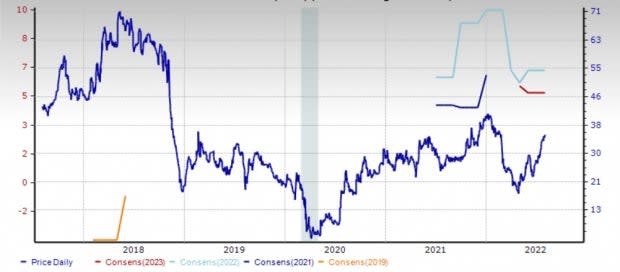

The Zacks Consensus Estimate for OCN is $6.50 and $5.22 for 2022 and 2023 earnings. Earnings estimates have been unchanged over the past month. Also, for the ongoing and the next year, its revenues are expected to increase 4.6% and 1.04%, respectively. The company carries a Zacks Rank of 2 (Buy) at present.

You can see the complete list of today's Zacks #1 (Strong Buy) Rank stocks here.

Price and Consensus: OCN

Image Source: Zacks Investment Research

Velocity Financial: Based in Westlake Village, CA, Velocity Financial is a vertically integrated real estate finance firm, which offers and manages investor loans for 1-4 unit residential rental and small commercial properties. VEL originates loans across the United States through its extensive network of independent mortgage brokers.

Considering the increased economic activity, supported by market normalization and the reopening of the economy, the demand for investor properties is anticipated to remain robust. This is expected to drive investor loan demand. Given Velocity Financial's expanded liquidity capacity, it is well-poised to capitalize on growth in the addressable market and, thereby, fund loan volume in the upcoming period.

The Zacks Consensus Estimate for VEL's 2022 and 2023 earnings has been unchanged over the past month. Also, for the ongoing and the next year, its revenues are expected to increase 20.4% and 33.4%, respectively. The company carries a Zacks Rank of 3 (Hold) at present.

Price and Consensus: VEL

Image Source: Zacks Investment Research

Walker & Dunlop: Based in Bethesda, MD, Walker & Dunlop is one of the largest U.S. providers of capital to the multifamily industry and the fourth-largest lender for all commercial real estate, including industrial, office, retail and hospitality. The company's expansion strategies, and strengthening of the online lending platform through acquisitions are likely to drive the top line. Further, Walker & Dunlop's commitment to capturing market share on the back of heavy investments in artificial intelligence and machine-learning capabilities is commendable.

Of late, the company has been making expansion moves, including acquisitions and additional hirings. Last month, WD expanded its property sales team, Walker & Dunlop Investment Sales, with the buyout of Avalon Real Estate Partners, a boutique commercial real estate brokerage firm. The latter specializes in land brokerage, investment consultation and capital sources services. The buyout is in line with WD’s efforts to expand and become a preeminent property sales practice in the United States.

The Zacks Rank #3 company’s earnings estimates has been unchanged over the past month to $9.38 and $10.54, respectively. Walker & Dunlop's earnings for the ongoing and the following year are projected to witness year-over-year growth of 15.1% and 12.3%, respectively. Revenues for 2022 and 2023 are projected to increase 17.5% and 9.9% year over year.

Price and Consensus: WD

Image Source: Zacks Investment Research

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Walker & Dunlop, Inc. (WD) : Free Stock Analysis Report

Ocwen Financial Corporation (OCN) : Free Stock Analysis Report

Velocity Financial, Inc. (VEL) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research