Yahoo Finance

Yahoo Finance 3 Things to Look For When Ballard Power Systems Reports Q4 Earnings

Ballard Power Systems (NASDAQ: BLDP), a leader in hydrogen fuel-cell solutions, is due to report fourth-quarter earnings on March 1. Whereas Ballard's stock soared 167% higher in 2017, shares have dropped more than 20% so far this year. Predominantly, the culprit for the stock's nosedive is a negative note from Spruce Point Capital. A strong earnings report, however, can certainly send the stock on an upward trajectory.

Analysts estimate Ballard will report a loss -- though less than $0.01 per share -- but in the fuel-cell industry, that's not too shabby, considering the market is still waiting for proof that providing hydrogen fuel-cell solutions can be a lucrative enterprise. Let's look at some things we can expect management to address.

Image source: Getty Images.

On the road to sales growth

Unlike its peer Plug Power (NASDAQ: PLUG), Ballard is not too keen on issuing guidance; however, the company felt compelled to release a revenue forecast in response to the negative note from Spruce Point Capital. According to preliminary results, Ballard estimates it will report fiscal 2017 revenue of $120 million -- which would be a company record for annual sales, and a 41% increase over the $85 million the company reported in fiscal 2016. In order to achieve this figure, Ballard will have to report quarterly revenue of $39 million.

Management believes the company's success in China, specifically in the heavy-duty motive segment, will be the main driver of revenue growth in fiscal 2017. For example, Ballard expects shipments in this segment to grow more than 150% in fiscal 2017 from fiscal 2016. Investors should be keenly focused on the company's progress in China as it represents the crux of Spruce Point Capital's skepticism, so realizing growth would be some vindication for the company.

Driving toward the bottom line

In addition to achieving a company record in terms of revenue, Ballard is confident that it will report significant growth further down the income statement. Based on preliminary results, management expects to report positive adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) for fiscal 2017. For some context, the company has averaged adjusted EBITDA of negative $14.6 million over the past three years.

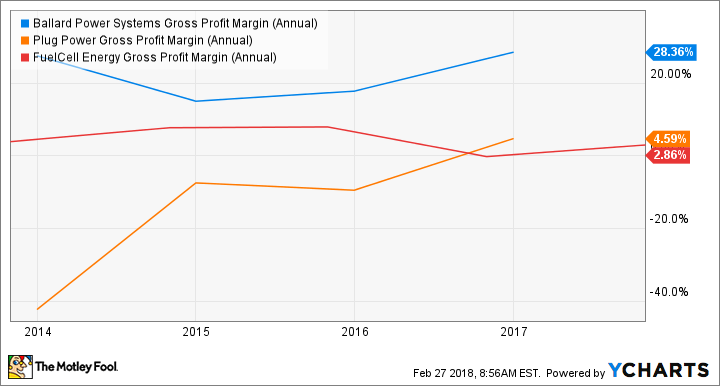

The expected growth on the bottom line stems from an improved product mix. With increasing sales from higher-margin segments like heavy duty motive and technology solutions, management forecasts Ballard's gross margin will expand to 35%. This is no small feat considering the company reported gross margins of 18% and 28% in fiscal years 2015 and 2016, respectively.

Aside from looking for the company to surpass past performance, investors should confirm that Ballard is continuing to grow its presence in the Chinese heavy-duty motive market since it plays such a prominent role in the company's bottom-line growth. This focus sets the company apart from other fuel-cell companies that primarily serve other markets. For example, Plug Power deals largely in the material handling business, and FuelCell Energy (NASDAQ: FCEL) is focused on utility-scale and on-site power generation solutions.

BLDP Gross Profit Margin (Annual) data by YCharts.

According to preliminary results, Plug Power will report adjusted gross margin of approximately 1% for fiscal 2017.

A precious few details about a non-precious-metal catalyst

Lastly, it'll be worth looking for management's commentary regarding Ballard's new 30-watt FCgen-1040 fuel-cell stack product, which was expected to launch during the fourth quarter. The development of the FCgen-1040 deserves recognition because it includes a non-precious-metal catalyst (NPMC); consequently, it uses 80% less platinum. This is noteworthy since platinum is about 10% to 15% of a traditional fuel-cell stack's cost. Ballard believes that in addition to its applications in material handling equipment applications, the NPMC technology could be used to generate electricity in laptop and cellphone chargers, and in military soldier power devices.

Revenue associated with NPMC sales falls under Ballard's technology solutions segment. Since this is one of the company's higher margin businesses, rising sales of NPMC products could go along way in helping the company to increase profitability and achieve its target of more than $30 million in annual adjusted EBITDA by 2020.

What to expect when Ballard reports

Suggesting that Ballard will set a company record for annual revenue, management has clearly set the bar high for its earnings report. Should the company, in fact, report fiscal 2017 revenue of $120 million, investors may breathe a sigh of relief -- albeit temporarily -- in regard to the critical note from Spruce Point Capital. Moreover, they may feel assured that the company is on track to meet its fiscal 2020 revenue target of $250 million. Of course, investors should also confirm that the company has achieved its gross margin and adjusted EBITDA guidance.

Although Ballard seems poised to report some impressive achievements for fiscal 2017, this should not overexcite investors who are bullish on hydrogen-power solutions. In terms of investments, the fuel-cell industry still remains an extremely speculative option and should only garner the attention of those who recognize the underlying risks.

More From The Motley Fool

Scott Levine has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.