Yahoo Finance

Yahoo Finance These 4 Measures Indicate That Cohort (LON:CHRT) Is Using Debt Reasonably Well

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Cohort plc (LON:CHRT) does carry debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Cohort

What Is Cohort's Net Debt?

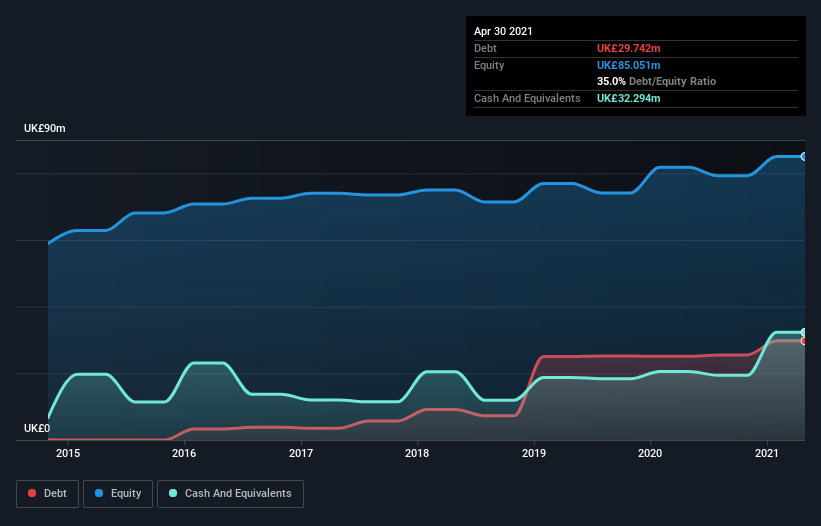

You can click the graphic below for the historical numbers, but it shows that as of April 2021 Cohort had UK£29.7m of debt, an increase on UK£25.1m, over one year. But it also has UK£32.3m in cash to offset that, meaning it has UK£2.55m net cash.

How Healthy Is Cohort's Balance Sheet?

We can see from the most recent balance sheet that Cohort had liabilities of UK£58.2m falling due within a year, and liabilities of UK£47.6m due beyond that. Offsetting these obligations, it had cash of UK£32.3m as well as receivables valued at UK£57.1m due within 12 months. So it has liabilities totalling UK£16.4m more than its cash and near-term receivables, combined.

Given Cohort has a market capitalization of UK£235.7m, it's hard to believe these liabilities pose much threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. Despite its noteworthy liabilities, Cohort boasts net cash, so it's fair to say it does not have a heavy debt load!

The modesty of its debt load may become crucial for Cohort if management cannot prevent a repeat of the 26% cut to EBIT over the last year. When a company sees its earnings tank, it can sometimes find its relationships with its lenders turn sour. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Cohort can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. While Cohort has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Happily for any shareholders, Cohort actually produced more free cash flow than EBIT over the last three years. There's nothing better than incoming cash when it comes to staying in your lenders' good graces.

Summing up

While it is always sensible to look at a company's total liabilities, it is very reassuring that Cohort has UK£2.55m in net cash. And it impressed us with free cash flow of UK£15m, being 111% of its EBIT. So we are not troubled with Cohort's debt use. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 2 warning signs with Cohort , and understanding them should be part of your investment process.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.