Yahoo Finance

Yahoo Finance 4 Reasons Why You Should Avoid Nordson (NDSN) Stock Now

We issued a research report on Nordson Corporation NDSN on Aug 31. We believe that weak projections for the upcoming quarter, risks arising from international diversification and escalating costs and debt levels, and competitive threats have weakened the company’s prospects.

It currently carries a Zacks Rank #4 (Sell).

Also, the company’s stock price performance has been weak in the last three months. Its shares have lost roughly 7.5%, wider than 1.5% decline of the industry it belongs to.

Here’s why Nordson should be currently avoided as an investment choice:

Weak Guidance: Despite delivering improved year-over-year results, we believe that projections for the fiscal fourth quarter were disappointing. Net sales are anticipated to grow 4-8% year over year, including organic volume decline of 3% to 7%. The projections are weaker compared with 20% sales growth and 11% organic volume growth recorded in the previous quarter. Also, margin is expected to decline to 21% in the fiscal fourth quarter from 26% in the previous quarter.

Diversification Woes: We believe Nordson’s geographical expansion has exposed it to risks arising from foreign currencies movements and geopolitical issues. Notably, the company operates in more than 35 countries, with manufacturing facilities primarily in the United States, the People’s Republic of China, Germany, Mexico, the Netherlands, Thailand and the United Kingdom. In third quarter fiscal 2017 (ended Jul 31, 2017), the company sourced nearly 69% of its revenues from international operations. Uncertainties in the economic growth of the countries served will severely impact the company’s businesses.

Rising Costs and Debt Levels: Over time, Nordson’s profitability suffered from higher costs and expenses. For instance, in the first nine months of fiscal 2017, its cost of sales grew 14.6% from the year-ago period while operating expenses rose 12%. Another issue currently faced by the company is its huge debt level, which was approximately $1,569.7 million at the end of the fiscal third quarter. We believe that, if unchecked, higher costs and operating expenses as well as rising debt levels will prove detrimental to the company’s profitability.

Others: In addition to the above-mentioned headwinds, we believe that complex and competitive environment due to its wide diversity of products as well as vastness of the markets served remain an issue for Nordson. Also, failure of new products and technologies in the market may hurt the company’s competitive position.

Stocks to Consider

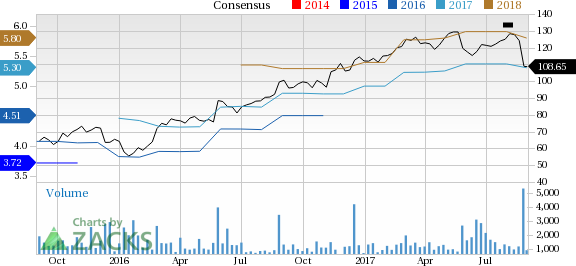

Nordson currently has $6.3 billion market capitalization. Notably, over the last 30 days, the stock’s Zacks Consensus Estimate decreased 1.3% to $5.30 per share for fiscal 2017 (ending October 2017) and by 1.9% to $5.80 for fiscal 2018.

Nordson Corporation Price and Consensus

Nordson Corporation Price and Consensus | Nordson Corporation Quote

In the same space some better-ranked stocks are Altra Industrial Motion Corporation AIMC, Kadant Inc. KAI and Sun Hydraulics Corporation SNHY. All these stocks sport a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Altra Industrial Motion’s earnings estimates for 2017 and 2018 were revised upward in the last 60 days. Also, the company pulled off an average positive earnings surprise of 16.95% over the last four quarters.

Kadant’s average earnings surprise for the last four quarters was a positive 19.29%. Also, earnings expectations for 2017 and 2018 improved over the past 60 days.

Sun Hydraulics’ earnings estimates for 2017 and 2018 were revised upward in the last 60 days. Also, the company performed well in the last quarter, delivering a positive earnings surprise of 33.33%.

One Simple Trading Idea

Since 1988, the Zacks system has more than doubled the S&P 500 with an average gain of +25% per year. With compounding, rebalancing, and exclusive of fees, it can turn thousands into millions of dollars.

This proven stock-picking system is grounded on a single big idea that can be fortune shaping and life changing. You can apply it to your portfolio starting today.

Learn more >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Sun Hydraulics Corporation (SNHY) : Free Stock Analysis Report

Kadant Inc (KAI) : Free Stock Analysis Report

Altra Industrial Motion Corp. (AIMC) : Free Stock Analysis Report

To read this article on Zacks.com click here.