Yahoo Finance

Yahoo Finance American Express (AXP) Jumps 10.4% YTD: More Upside Left?

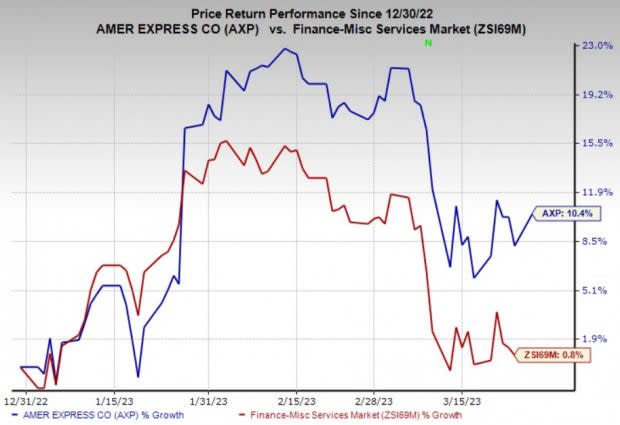

American Express Company AXP shares have jumped 10.4% in the year-to-date period despite volatilities, outperforming the 0.8% rise of the industry. Upbeat view, a growing international business and efficient capital deployment are driving the stock.

Headquartered in New York, American Express benefits from innovative service offerings and consumer spending resilience. It is a diversified financial services company, offering charge and credit payment card products, and travel-related services worldwide. It currently has a market cap of $118.9 billion.

Image Source: Zacks Investment Research

Can It Retain Momentum?

The answer is yes and before we get into the details, let us show you how its estimates for 2023 stand. The Zacks Consensus Estimate for 2023 earnings per share currently stands at $11.25, signaling a 14.2% year-over-year increase. AXP beat earnings estimates in three of the past four quarters and missed once, with the average surprise being 4.5%.

Also, the consensus mark for 2023 revenues is pegged at $61.1 billion, predicting 15.6% growth from the 2022 level.

Now let’s delve into what’s driving this Zacks Rank #2 (Buy) stock.

Strong financials are positioning the company for expedited growth. The company had $34 billion in cash and cash equivalents at fourth quarter-end, which jumped 55% year over year. It had a manageable short-term borrowing of $1 billion. Also, a solid cash position places it in a comfortable spot to service its financial commitments. Free cash flows jumped 46.8% year over year to $19.2 billion in the trailing 12-month period.

Its financial strength is supporting shareholder value boosting efforts. The company bought back 20 million common shares worth $3.3 billion last year and paid dividends worth $1.6 billion. Earlier this month, it announced a new buyback plan, equipping it to repurchase up to 120 million common shares. Also, AXP approved a 15% hike in the quarterly dividend.

American Express currently has a VGM Score of A. Our research shows that stocks with a VGM Score of A or B, combined with a Zacks Rank #1 (Strong Buy) or 2, offer the best investment opportunities for investors. Thus, the company appears to be a compelling investment proposition at the moment. You can see the complete list of today’s Zacks #1 Rank stocks here.

AXP’s focus on enhancing innovative service offerings and global footprint will drive long-term growth. In a bid to benefit its consumers and small business Card Members, the company collaborated with Australia-based payment solutions provider Cuscal to introduce the card bill PayID service throughout the country. Its focus on capturing market share of growing economies is praiseworthy.

American Express’s coverage in the UK and other regions continues to accelerate as leading businesses across home improvement, food-to-go and broader retail sectors are partnering with the company. Discount revenues are the largest revenue source of the company and are likely to increase as more merchants team up with AXP.

Risks

Despite the upside potential, there are a few factors that investors should keep in mind.

Rising expenses are eating into profits. Throughout 2021 and 2022, AXP’s total expenses jumped 22% and 24% year over year, respectively. Also, its forward 12-month price to earnings of 14.1% is higher than the industry average of 10.7%, making it an expensive stock. Nevertheless, we believe that a systematic and strategic plan of action will drive long-term growth.

Other Key Picks in Finance

Meanwhile, investors interested in the broader finance space can look into other top-ranked stocks like Euronet Worldwide, Inc. EEFT, Mr. Cooper Group Inc. COOP and Burford Capital Limited BUR, each carrying a Zacks Rank #2 at present.

The Zacks Consensus Estimate for Euronet Worldwide’s 2023 earnings suggests 15.5% year-over-year growth. Also, the consensus mark for EEFT’s revenues in 2023 suggests 9.2% year-over-year growth.

The consensus mark for Mr. Cooper Group’s 2023 earnings indicates a 127.4% year-over-year increase. COOP beat earnings estimates in all the past four quarters, with an average of 200.7%.

The Zacks Consensus Estimate for Burford Capital’s 2023 earnings is pegged at $1.34 per share, indicating a massive improvement from the year-ago loss of 33 cents. Also, the consensus mark for BUR’s revenues in 2023 suggests 229.1% year-over-year growth.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

American Express Company (AXP) : Free Stock Analysis Report

Euronet Worldwide, Inc. (EEFT) : Free Stock Analysis Report

MR. COOPER GROUP INC (COOP) : Free Stock Analysis Report