Yahoo Finance

Yahoo Finance Analyst Forecasts Just Became More Bearish On Trainline Plc (LON:TRN)

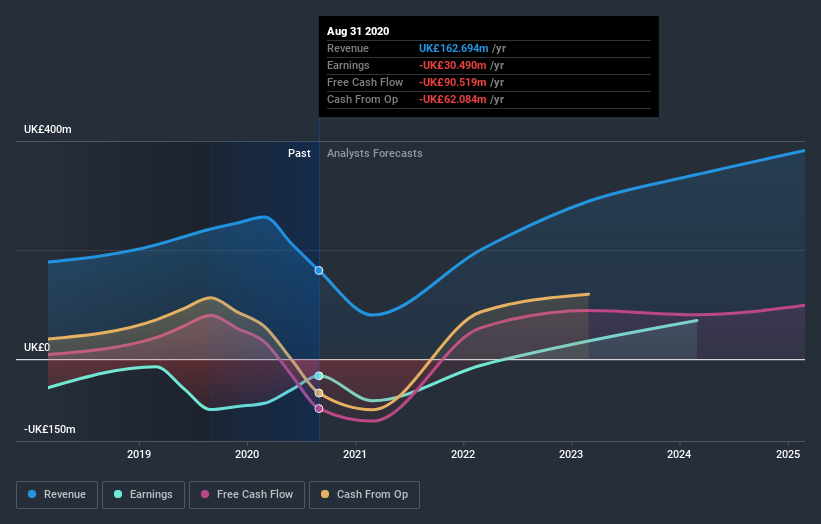

The latest analyst coverage could presage a bad day for Trainline Plc (LON:TRN), with the analysts making across-the-board cuts to their statutory estimates that might leave shareholders a little shell-shocked. Revenue estimates were cut sharply as the analysts signalled a weaker outlook - perhaps a sign that investors should temper their expectations as well.

Following the downgrade, the consensus from eight analysts covering Trainline is for revenues of UK£81m in 2021, implying a painful 50% decline in sales compared to the last 12 months. Per-share losses are expected to explode, reaching UK£0.16 per share. However, before this estimates update, the consensus had been expecting revenues of UK£91m and UK£0.16 per share in losses. So there's definitely been a change in sentiment in this update, with the analysts administering a substantial haircut to this year's revenue estimates, while at the same time holding losses per share steady.

See our latest analysis for Trainline

The consensus price target was broadly unchanged at UK£4.64, implying that the business is performing roughly in line with expectations, despite a downwards adjustment to forecast sales this year. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. The most optimistic Trainline analyst has a price target of UK£5.35 per share, while the most pessimistic values it at UK£3.60. There are definitely some different views on the stock, but the range of estimates is not wide enough as to imply that the situation is unforecastable, in our view.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. Over the past year, revenues have declined around 32% annually. Worse, forecasts are essentially predicting the decline to accelerate, with the estimate for a 50% decline in revenue next year. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenue grow 17% per year. So it's pretty clear that, while it does have declining revenues, the analysts also expect Trainline to suffer worse than the wider industry.

The Bottom Line

Unfortunately analysts also downgraded their revenue estimates, and industry data suggests that Trainline's revenues are expected to grow slower than the wider market. Often, one downgrade can set off a daisy-chain of cuts, especially if an industry is in decline. So we wouldn't be surprised if the market became a lot more cautious on Trainline after today.

So things certainly aren't looking great, and you should also know that we've spotted some potential warning signs with Trainline, including recent substantial insider selling. For more information, you can click here to discover this and the 2 other concerns we've identified.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are downgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.