Yahoo Finance

Yahoo Finance Analysts Are More Bearish On 3i Group plc (LON:III) Than They Used To Be

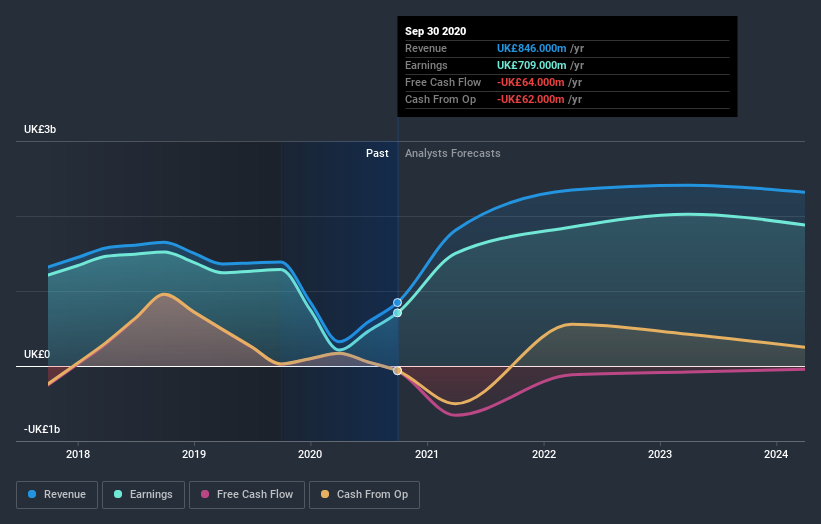

The latest analyst coverage could presage a bad day for 3i Group plc (LON:III), with the analysts making across-the-board cuts to their statutory estimates that might leave shareholders a little shell-shocked. Both revenue and earnings per share (EPS) forecasts went under the knife, suggesting analysts have soured majorly on the business.

Following the downgrade, the current consensus from 3i Group's five analysts is for revenues of UK£1.8b in 2021 which - if met - would reflect a major 114% increase on its sales over the past 12 months. Per-share earnings are expected to leap 112% to UK£1.56. Prior to this update, the analysts had been forecasting revenues of UK£2.1b and earnings per share (EPS) of UK£1.79 in 2021. Indeed, we can see that the analysts are a lot more bearish about 3i Group's prospects, administering a measurable cut to revenue estimates and slashing their EPS estimates to boot.

Check out our latest analysis for 3i Group

Analysts made no major changes to their price target of UK£13.55, suggesting the downgrades are not expected to have a long-term impact on 3i Group's valuation. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. Currently, the most bullish analyst values 3i Group at UK£14.25 per share, while the most bearish prices it at UK£12.60. With such a narrow range of valuations, analysts apparently share similar views on what they think the business is worth.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the 3i Group's past performance and to peers in the same industry. For example, we noticed that 3i Group's rate of growth is expected to accelerate meaningfully, with revenues forecast to exhibit 4x growth to the end of 2021 on an annualised basis. That is well above its historical decline of 5.3% a year over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in the industry are forecast to see their revenue grow 3.2% per year. So it looks like 3i Group is expected to grow faster than its competitors, at least for a while.

The Bottom Line

The biggest issue in the new estimates is that analysts have reduced their earnings per share estimates, suggesting business headwinds lay ahead for 3i Group. While analysts did downgrade their revenue estimates, these forecasts still imply revenues will perform better than the wider market. The lack of change in the price target is puzzling in light of the downgrade but, with a serious decline expected this year, we wouldn't be surprised if investors were a bit wary of 3i Group.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. At Simply Wall St, we have a full range of analyst estimates for 3i Group going out to 2024, and you can see them free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.