Yahoo Finance

Yahoo Finance AnaptysBio (NASDAQ:ANAB) shareholders are up 11% this past week, but still in the red over the last three years

AnaptysBio, Inc. (NASDAQ:ANAB) shareholders should be happy to see the share price up 13% in the last month. But that is small recompense for the exasperating returns over three years. Tragically, the share price declined 59% in that time. Some might say the recent bounce is to be expected after such a bad drop. The rise has some hopeful, but turnarounds are often precarious.

While the stock has risen 11% in the past week but long term shareholders are still in the red, let's see what the fundamentals can tell us.

Check out our latest analysis for AnaptysBio

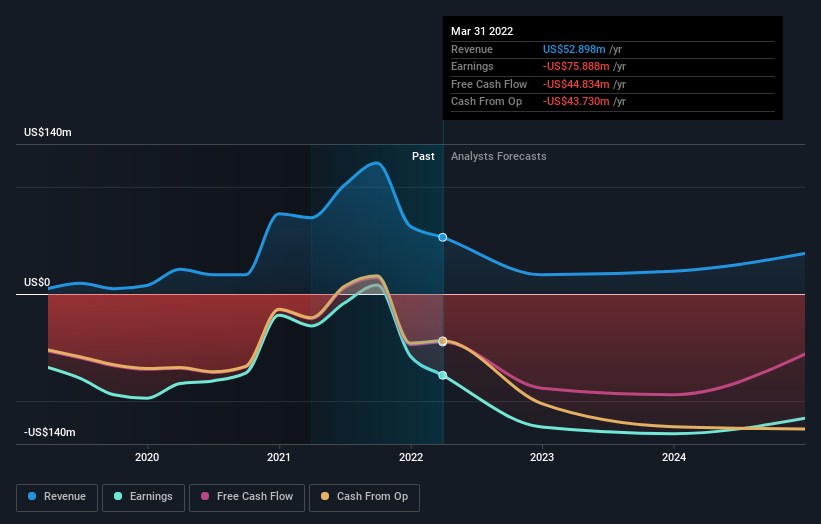

Given that AnaptysBio didn't make a profit in the last twelve months, we'll focus on revenue growth to form a quick view of its business development. Generally speaking, companies without profits are expected to grow revenue every year, and at a good clip. That's because fast revenue growth can be easily extrapolated to forecast profits, often of considerable size.

Over three years, AnaptysBio grew revenue at 73% per year. That's well above most other pre-profit companies. In contrast, the share price is down 17% compound, over three years - disappointing by most standards. It seems likely that the market is worried about the continual losses. But a share price drop of that magnitude could well signal that the market is overly negative on the stock.

The graphic below depicts how earnings and revenue have changed over time (unveil the exact values by clicking on the image).

It's probably worth noting that the CEO is paid less than the median at similar sized companies. But while CEO remuneration is always worth checking, the really important question is whether the company can grow earnings going forward. If you are thinking of buying or selling AnaptysBio stock, you should check out this free report showing analyst profit forecasts.

A Different Perspective

While it's never nice to take a loss, AnaptysBio shareholders can take comfort that their trailing twelve month loss of 9.7% wasn't as bad as the market loss of around 19%. Unfortunately, last year's performance may indicate unresolved challenges, given that it's worse than the annualised loss of 1.7% over the last half decade. Whilst Baron Rothschild does tell the investor "buy when there's blood in the streets, even if the blood is your own", buyers would need to examine the data carefully to be comfortable that the business itself is sound. It's always interesting to track share price performance over the longer term. But to understand AnaptysBio better, we need to consider many other factors. Even so, be aware that AnaptysBio is showing 2 warning signs in our investment analysis , you should know about...

But note: AnaptysBio may not be the best stock to buy. So take a peek at this free list of interesting companies with past earnings growth (and further growth forecast).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on US exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.