Yahoo Finance

Yahoo Finance AppFolio (NASDAQ:APPF) delivers shareholders massive 40% CAGR over 5 years, surging 9.5% in the last week alone

We think all investors should try to buy and hold high quality multi-year winners. While not every stock performs well, when investors win, they can win big. For example, the AppFolio, Inc. (NASDAQ:APPF) share price is up a whopping 434% in the last half decade, a handsome return for long term holders. And this is just one example of the epic gains achieved by some long term investors. It's even up 9.5% in the last week.

Since it's been a strong week for AppFolio shareholders, let's have a look at trend of the longer term fundamentals.

View our latest analysis for AppFolio

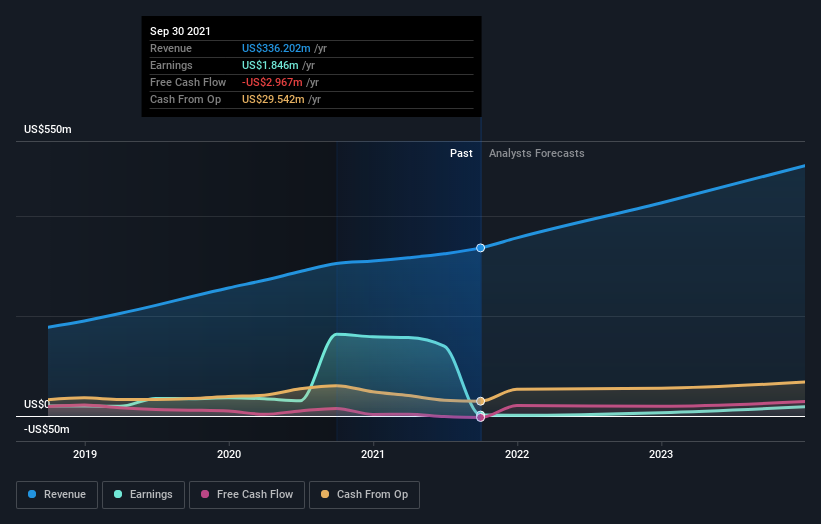

We don't think that AppFolio's modest trailing twelve month profit has the market's full attention at the moment. We think revenue is probably a better guide. As a general rule, we think this kind of company is more comparable to loss-making stocks, since the actual profit is so low. For shareholders to have confidence a company will grow profits significantly, it must grow revenue.

In the last 5 years AppFolio saw its revenue grow at 24% per year. That's well above most pre-profit companies. Arguably, this is well and truly reflected in the strong share price gain of 40%(per year) over the same period. Despite the strong run, top performers like AppFolio have been known to go on winning for decades. So we'd recommend you take a closer look at this one, but keep in mind the market seems optimistic.

The company's revenue and earnings (over time) are depicted in the image below (click to see the exact numbers).

It's probably worth noting we've seen significant insider buying in the last quarter, which we consider a positive. That said, we think earnings and revenue growth trends are even more important factors to consider. So it makes a lot of sense to check out what analysts think AppFolio will earn in the future (free profit forecasts).

A Different Perspective

Investors in AppFolio had a tough year, with a total loss of 29%, against a market gain of about 21%. Even the share prices of good stocks drop sometimes, but we want to see improvements in the fundamental metrics of a business, before getting too interested. On the bright side, long term shareholders have made money, with a gain of 40% per year over half a decade. If the fundamental data continues to indicate long term sustainable growth, the current sell-off could be an opportunity worth considering. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. Consider risks, for instance. Every company has them, and we've spotted 3 warning signs for AppFolio you should know about.

AppFolio is not the only stock that insiders are buying. For those who like to find winning investments this free list of growing companies with recent insider purchasing, could be just the ticket.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on US exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.