Yahoo Finance

Yahoo Finance Is Argonaut Gold (TSE:AR) A Risky Investment?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies Argonaut Gold Inc. (TSE:AR) makes use of debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Argonaut Gold

What Is Argonaut Gold's Debt?

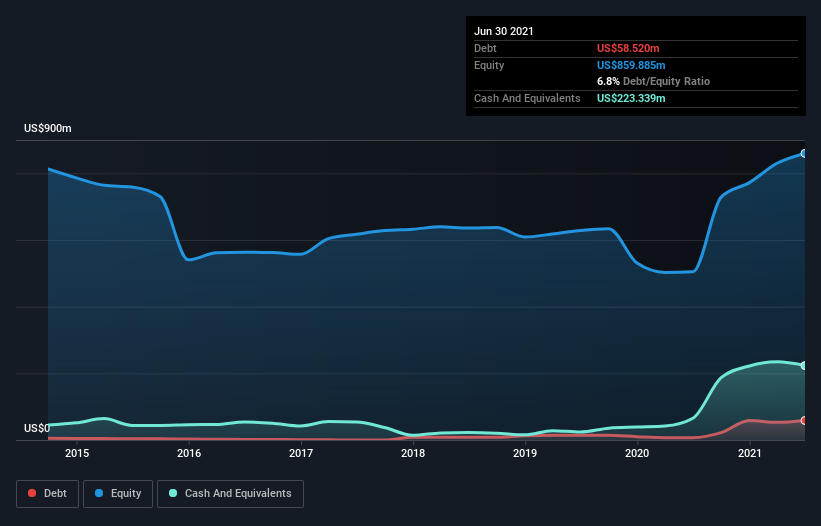

The image below, which you can click on for greater detail, shows that at June 2021 Argonaut Gold had debt of US$58.5m, up from US$7.00m in one year. However, its balance sheet shows it holds US$223.3m in cash, so it actually has US$164.8m net cash.

How Healthy Is Argonaut Gold's Balance Sheet?

According to the last reported balance sheet, Argonaut Gold had liabilities of US$131.4m due within 12 months, and liabilities of US$190.0m due beyond 12 months. On the other hand, it had cash of US$223.3m and US$26.5m worth of receivables due within a year. So it has liabilities totalling US$71.6m more than its cash and near-term receivables, combined.

Given Argonaut Gold has a market capitalization of US$732.5m, it's hard to believe these liabilities pose much threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. Despite its noteworthy liabilities, Argonaut Gold boasts net cash, so it's fair to say it does not have a heavy debt load!

Although Argonaut Gold made a loss at the EBIT level, last year, it was also good to see that it generated US$144m in EBIT over the last twelve months. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Argonaut Gold's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. While Argonaut Gold has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Considering the last year, Argonaut Gold actually recorded a cash outflow, overall. Debt is far more risky for companies with unreliable free cash flow, so shareholders should be hoping that the past expenditure will produce free cash flow in the future.

Summing up

We could understand if investors are concerned about Argonaut Gold's liabilities, but we can be reassured by the fact it has has net cash of US$164.8m. So we are not troubled with Argonaut Gold's debt use. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 1 warning sign for Argonaut Gold that you should be aware of before investing here.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.