Yahoo Finance

Yahoo Finance Ashland's (NYSE:ASH) Shareholders Will Receive A Bigger Dividend Than Last Year

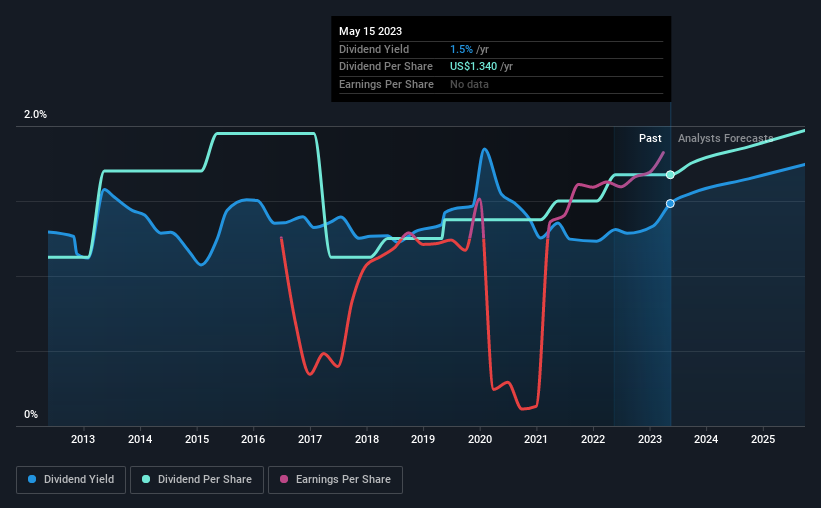

Ashland Inc. (NYSE:ASH) will increase its dividend on the 15th of June to $0.385, which is 15% higher than last year's payment from the same period of $0.335. Despite this raise, the dividend yield of 1.5% is only a modest boost to shareholder returns.

Check out our latest analysis for Ashland

Ashland's Payment Has Solid Earnings Coverage

If it is predictable over a long period, even low dividend yields can be attractive. Based on the last payment, Ashland was earning enough to cover the dividend, but free cash flows weren't positive. We think that cash flows should take priority over earnings, so this is definitely a worry for the dividend going forward.

Over the next year, EPS is forecast to expand by 59.5%. If the dividend continues along recent trends, we estimate the payout ratio will be 18%, which is in the range that makes us comfortable with the sustainability of the dividend.

Dividend Volatility

The company has a long dividend track record, but it doesn't look great with cuts in the past. The annual payment during the last 10 years was $0.90 in 2013, and the most recent fiscal year payment was $1.34. This works out to be a compound annual growth rate (CAGR) of approximately 4.1% a year over that time. Modest growth in the dividend is good to see, but we think this is offset by historical cuts to the payments. It is hard to live on a dividend income if the company's earnings are not consistent.

The Dividend Looks Likely To Grow

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. Ashland has impressed us by growing EPS at 34% per year over the past five years. Rapid earnings growth and a low payout ratio suggest this company has been effectively reinvesting in its business. Should that continue, this company could have a bright future.

Our Thoughts On Ashland's Dividend

In summary, while it's always good to see the dividend being raised, we don't think Ashland's payments are rock solid. While the low payout ratio is a redeeming feature, this is offset by the minimal cash to cover the payments. We don't think Ashland is a great stock to add to your portfolio if income is your focus.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. Earnings growth generally bodes well for the future value of company dividend payments. See if the 10 Ashland analysts we track are forecasting continued growth with our free report on analyst estimates for the company. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here