Yahoo Finance

Yahoo Finance Average UK house price has jumped by £24,000 during year of Covid-19 lockdowns

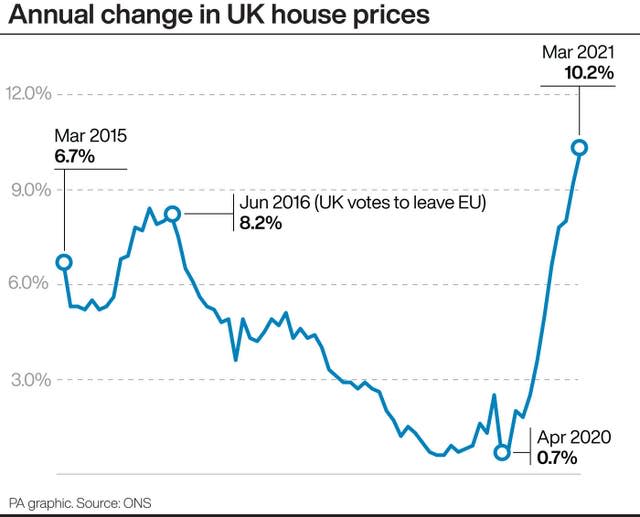

The average UK house price has surged by £24,000 during the past year of coronavirus lockdowns, according to the Office for National Statistics (ONS).

Property values jumped by 10.2% over the year to March 2021, marking the strongest annual growth rate the UK has seen since August 2007, its report said.

The average UK property value reached a new record high of £256,000 in March 2021, which was £24,000 higher than in March 2020, the month that the UK lockdowns started.

There were also signs that the coronavirus pandemic has had an impact on preferences for different property types.

The average price of detached properties increased by 11.7% in the year to March 2021, in comparison with flats and maisonettes increasing by 5.0% over the same period.

Average house prices increased over the year in England to £275,000 (a 10.2% annual increase), in Wales to £185,000 (an 11.0% uplift), in Scotland to £167,000 (a 10.6% jump) and in Northern Ireland to £149,000 (up by 6.0%).

Sam Beckett continued: (2/2) pic.twitter.com/DW68xKiXkz

— Office for National Statistics (ONS) (@ONS) May 19, 2021

The ONS report said: “Changes in the tax paid on housing transactions may have allowed sellers to request higher prices as the buyers’ overall costs are reduced.”

A stamp duty holiday, which had been due to end in March, was recently extended in England and Northern Ireland.

In Wales, a holiday on the equivalent tax has also been extended until the end of June 2021.

A similar property transaction tax in Scotland ended on March 31 2021.

Within England, Yorkshire and the Humber was the region with the highest annual house price growth, with average prices increasing by 14.0% in the year to March.

The lowest annual growth was in London, where average prices increased by 3.7% over the year.

Average house prices increased over the year in:

▪️ England to £275,000 (10.2%)▪️ Wales to £185,000 (11.0%)▪️ Scotland to £167,000 (10.6%)▪️ Northern Ireland to £149,000 (6.0%)

➡️ https://t.co/2N7mOVpvgN pic.twitter.com/noqyv42n5E

— Office for National Statistics (ONS) (@ONS) May 19, 2021

London’s average house prices remain the most expensive of any region in the UK at an average of £500,000.

Sarah Coles, personal finance analyst at Hargreaves Lansdown, said: “We’re back to the kind of double-figure house price rises we saw in the heady days before the financial crisis.

“And while lenders are far more cautious than they were back in 2007, in this kind of market, there’s still the risk buyers will lose their heads, and make a property mistake that could haunt them for years.”

She added: “In this kind of market, properties often go for well over the asking price – sometimes after a bidding war. It’s far too easy to be sucked into paying thousands of pounds more than you initially planned.

“It’s also easy to start panicking that if you don’t buy now, you never will, because house prices will rise another few thousand pounds next month. This kind of stressed decision-making can lead to horrible mistakes.”

Samuel Tombs, chief UK economist at Pantheon Macroeconomics, said the return of the stamp duty threshold to normal levels later this year “likely will mark a prolonged malaise in the market”.

He continued: “Mortgage rates are higher now than they were pre-Covid, whereas households’ incomes are not. The amount of money left over for housing also likely will decline as households return to pre-Covid expenditure patterns.

“Finally, the surge in house prices is stimulating strong growth in new housing supply, which will bear down on price growth soon. Accordingly, we think that house prices will be marginally below March’s level at the end of this year.”

Jamie Durham, an economist at PwC, said: “There is some risk to the outlook if inflation takes hold in the UK as banks may increase interest rates. This would affect mortgage affordability criteria, lending, and could ultimately weigh on house price growth, though the impact of this will depend on how high inflation rises.”

Mark Harris, chief executive of mortgage broker SPF Private Clients said: “March should have been the month when the stamp duty holiday came to an end and the housing market mini boom started to fizzle out but prices continued to surge.

“With the holiday now extended, and lockdown restrictions continuing to ease, buyers have been given another opportunity to take advantage of the saving.”

Mike Scott, chief analyst at estate agency Yopa said: “We believe that the lifting of Covid-19 restrictions, combined with people’s reassessed post-pandemic housing needs, the ‘accidental savings’ that many have made over the past year and the desire for a post-pandemic fresh start, will keep house prices high for at least for the rest of this year.”

Rachelle Earwaker, an economist at the Joseph Rowntree Foundation (JRF), said: “The largest annual house price increase since 2007 will benefit existing homeowners but make it much harder for renters to get on the property ladder, because deposit requirements rise at the same rate as house prices.

“We know that significant numbers of renters are continuing to grapple with arrears.”