Yahoo Finance

Yahoo Finance B&G Foods (BGS) Hurt by Soft Foodservice Sales & High Costs

B&G Foods, Inc. BGS appears in troubled shape, thanks to soft sales trends across its foodservice and industrial segments. The company is battling challenges stemming from persistently high selling, general and administrative (SG&A) expenses, which are exerting pressure on its profitability.

Management's efforts to navigate these difficulties have led to a cautious outlook for the fiscal 2024, with anticipated lower net sales and adjusted earnings. The Zacks Consensus Estimate for the fiscal 2024 earnings has moved down by a penny to 79 cents per share in the past seven days.

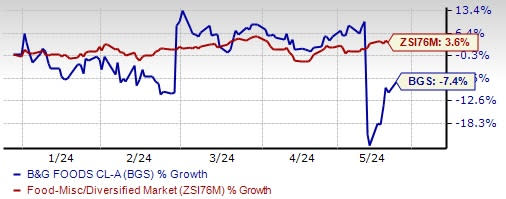

Shares of this Zacks Rank #4 (Sell) company have dropped 7.4% year to date against the industry’s growth of 3.6%. Let’s discuss this in detail.

Image Source: Zacks Investment Research

Soft Performance

The overall food industry has been grappling with category-wide challenges. Being no exception to this pressure, B&G Foods has witnessed soft sales in the past few quarters. The trend continued in first-quarter fiscal 2024, with the top and the bottom line missing the Zacks Consensus Estimate and declining year over year. The downside was due to foodservice trends and increased promotion spending. Softness in the foodservice and industrial businesses is stemming from an overall slowdown in out-of-home traffic and volumes.

Quarterly net sales of $475.2 million declined 7.1%, mainly due to lower unit volumes. Also, lower net pricing and the effects of product mix weighed on net sales. Base business net sales declined 4.4% to $475.3 million due to lower net pricing, an adverse product mix and lower unit volumes in the fiscal first quarter.

High-Cost Environment

B&G Foods has been grappling with higher SG&A expenses for a while now. In first-quarter fiscal 2023, B&G Foods’ SG&A expenses escalated 4% to $48.6 million due to higher general and administrative expenses, consumer marketing costs, acquisition/divestiture-related costs and non-recurring expenses. As a percentage of net sales, SG&A expenses moved up 1.1 percentage points to 10.2% on rise in general and administrative costs, mainly caused by modest inflation in wages, insurance, and other professional services.

Road Ahead Looks Dull

B&G Foods is encountering emerging challenges in food service and experiencing a slower recovery in net sales to retail customers, with anticipation for improvement in the second half of this year. Taking into account such headwinds, management recently lowered its fiscal 2024 outlook.

For the fiscal 2024, the company anticipates net sales in the band of $1.955-$1.985 billion, down from $2.06 billion reported last year. Earlier, BGS expected the metric to come in the range of $1.975-$2.02 billion. Adjusted earnings per share (EPS) for fiscal 2024 are envisioned to be between 75 cents and 95 cents, reflecting a year-over-year decline. The company had earlier expected EPS between 80 cents and $1.00.

As the company seeks to address these fundamental issues, the road ahead appears challenging, emphasizing the importance of strategic decision-making and adaptability in an evolving market landscape.

Top 3 Picks

Vital Farms Inc. VITL offers a range of produced pasture-raised foods. It currently sports a Zacks Rank #1 (Strong Buy). VITL has a trailing four-quarter average earnings surprise of 102.1%. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Vital Farms’ current financial-year sales and earnings suggests growth of 22.5% and 59.3%, respectively, from the year-ago reported numbers.

The J. M. Smucker Company SJM, a branded food and beverage product company, currently carries a Zacks Rank #2 (Buy). SJM has a trailing four-quarter earnings surprise of 7.5%, on average.

The Zacks Consensus Estimate for J. M. Smucker’s current fiscal year earnings indicates growth of 7.6% from the year-ago reported figure.

Utz Brands Inc. UTZ manufactures a diverse portfolio of salty snacks, currently carrying a Zacks Rank #2. UTZ has a trailing four-quarter earnings surprise of 2% on average.

The Zacks Consensus Estimate for Utz Brands’ current financial-year earnings suggests growth of 24.6% from the year-ago reported numbers.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The J. M. Smucker Company (SJM) : Free Stock Analysis Report

B&G Foods, Inc. (BGS) : Free Stock Analysis Report

Vital Farms, Inc. (VITL) : Free Stock Analysis Report

Utz Brands, Inc. (UTZ) : Free Stock Analysis Report