Yahoo Finance

Yahoo Finance Balfour Beatty (LON:BBY) Takes On Some Risk With Its Use Of Debt

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital. So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies Balfour Beatty plc (LON:BBY) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for Balfour Beatty

How Much Debt Does Balfour Beatty Carry?

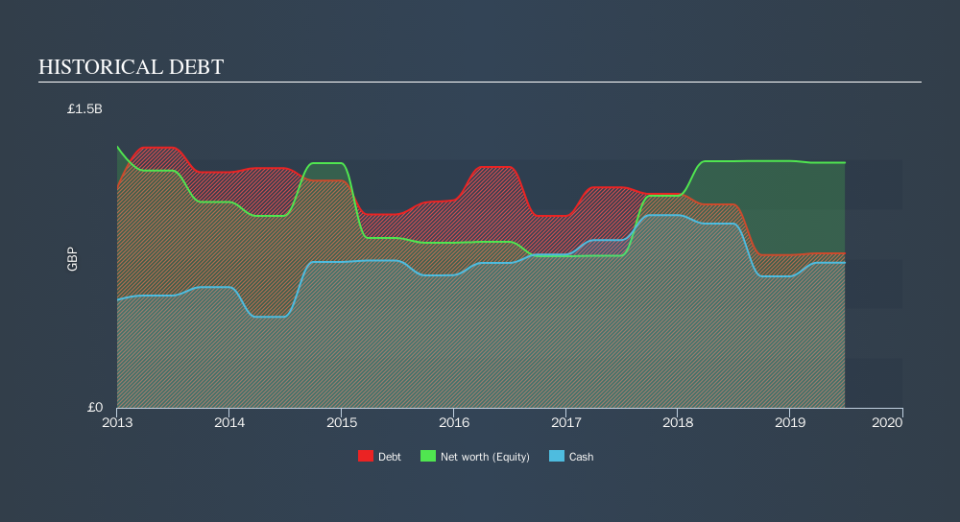

You can click the graphic below for the historical numbers, but it shows that Balfour Beatty had UK£776.0m of debt in June 2019, down from UK£1.02b, one year before. However, because it has a cash reserve of UK£730.0m, its net debt is less, at about UK£46.0m.

How Strong Is Balfour Beatty's Balance Sheet?

According to the last reported balance sheet, Balfour Beatty had liabilities of UK£2.29b due within 12 months, and liabilities of UK£1.30b due beyond 12 months. Offsetting this, it had UK£730.0m in cash and UK£1.29b in receivables that were due within 12 months. So its liabilities total UK£1.57b more than the combination of its cash and short-term receivables.

This is a mountain of leverage relative to its market capitalization of UK£1.58b. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

While Balfour Beatty's low debt to EBITDA ratio of 0.32 suggests only modest use of debt, the fact that EBIT only covered the interest expense by 4.1 last year does give us pause. But the interest payments are certainly sufficient to have us thinking about how affordable its debt is. Importantly, Balfour Beatty grew its EBIT by 81% over the last twelve months, and that growth will make it easier to handle its debt. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Balfour Beatty can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Over the last three years, Balfour Beatty saw substantial negative free cash flow, in total. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

We feel some trepidation about Balfour Beatty's difficulty conversion of EBIT to free cash flow, but we've got positives to focus on, too. For example, its EBIT growth rate and net debt to EBITDA give us some confidence in its ability to manage its debt. When we consider all the factors discussed, it seems to us that Balfour Beatty is taking some risks with its use of debt. While that debt can boost returns, we think the company has enough leverage now. Above most other metrics, we think its important to track how fast earnings per share is growing, if at all. If you've also come to that realization, you're in luck, because today you can view this interactive graph of Balfour Beatty's earnings per share history for free.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.