Yahoo Finance

Yahoo Finance Bear of the Day: Papa Johns International (PZZA)

Papa John’s International PZZA, the pizza delivery and takeout shop with nearly 6,000 locations globally has struggled in recent years with flat sales growth and falling profits.

In 2024, the stock has been collapsing, and its stock price is approaching four-year lows, reflecting extremely bearish investor sentiment.

While I do believe Papa John’s will still be around in the future, the company is overvalued based on its floundering growth rates and was recently downgraded to a Zacks Rank #5 (Strong Sell) rating.

Because of these bearish factors, I think investors should avoid Papa John’s International stock for now and seek better opportunities in the market.

Image Source: TradingView

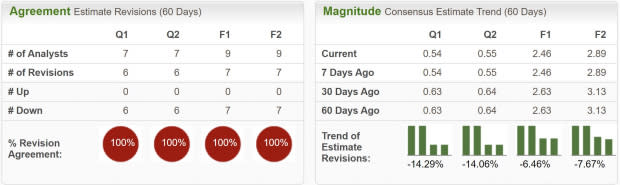

PZZA: Collapsing Earnings Estimates

Analysts have unanimously lowered earnings estimates for PZZA across timeframes. Current quarter earnings estimates have fallen by -14.3% over the last month, and current year earnings estimates by -6.5%.

Current year earnings are forecast to fall -9.2% YoY.

Papa John’s International has a Zacks Rank #5 (Strong Sell) rating and sits in the bottom 38% (145 out of 248) of the Zacks Industry rank.

Image Source: Zacks Investment Research

Papa John's Elevated Valuation

As of today, Papa John’s International has a one year forward earnings multiple 20.1x, which is below the market average and below its 10-year median of 29x.

However, those higher valuations of the past reflected higher growth estimates, so unless the company can turn that around, we could see that multiple fall even further.

Image Source: Zacks Investment Research

Bottom Line

As of today, I think there are far better opportunities in the stock market than Papa Johns, and thus investors should focus on those prospects.

However, I will say that I do believe Papa John’s International does enjoy an enduring brand that could recover, although the takeout food space grows increasingly competitive. Additionally, with the company paying a dividend yield of 3.8%, income investors could soon be interested.

But I would recommend avoiding the stock until there is a marked improvement in the earnings estimates and Zacks Rank before considering getting involved.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Papa John's International, Inc. (PZZA) : Free Stock Analysis Report