Yahoo Finance

Yahoo Finance The best student bank accounts for 2023

From interest-free overdrafts and cashback, to railcards and even a subscription to a meditation app, there are plenty of freebies and perks on offer from student bank accounts this year.

If you’re heading off to university this year, it makes sense to open a specialist student current account. You’ll benefit from a 0pc overdraft, which will help make budgeting easier, and you could get some freebies too.

As the beginning of the autumn term nears, banks often launch extra incentives to entice students to get their accounts.

In the past couple of weeks alone, Lloyds Bank and Halifax launched a £100 cash offer for students who open their student account and pay in at least £500 by October 31, while Nationwide’s FlexStudent has relaunched with a £100 cashback offer if £500 is deposited by December 15.

These offers join existing £100 cash incentives from HSBC, NatWest and Royal Bank of Scotland (RBS).

Other banks are offering cashback of up to 15pc when shopping with certain retailers, while Santander is giving away a four-year 16-25 railcard worth £100 – handy if you use the train to get home.

Here, Telegraph Money reveals the best student accounts on the market, with help from the analyst Defaqto.

How do student accounts work?

A student bank account works in the same way as a “normal” current account, just with some features that are more suited to those in higher education – namely an interest-free overdraft that lasts throughout your degree.

Note that when your time in higher education has finished, your account will usually convert from a student account to a graduate or standard bank account.

This means you’ll lose the student overdraft facility, meaning you’ll either have to pay off what you’ve borrowed, or face paying interest. Your bank should get in touch in plenty of time before this change takes effect.

Now read: The best-paying part-time jobs for students (that fit around lectures and the pub)

How to open a student bank account

Depending on which provider you choose, you may be able to complete the account opening process completely online.

Every bank will need to verify your identity before the account can be opened, which means you’ll need to send copies or photos of documents such as your passport, driving licence or birth certificate.

In addition, you’ll need proof of being in further education, so you’ll need to provide your UCAS code and either confirmation of an unconditional offer, a letter from your university confirming your place, or proof of A-level results that prove you’ve achieved the grades set out in a conditional offer.

Rules may vary between banks, but you can usually open a student bank account a couple of months before your course is due to start.

The best student bank accounts for 2023

Getting a student account can be an exciting time – particularly if you haven’t had much experience managing your own money before.

The best account choice will depend on your preferences, so think about whether a bank has a branch in your university town, should you want to visit the branch with any questions.

One provider might offer a student account perk that particularly suits you – such as a student railcard, which could save you a lot of money if you’re moving a long way from home.

Weigh up the pros and cons of each option, as we highlight some of this year’s best features.

Read now: The ultimate student renting guide

The best rates

It’s quite unusual for a student current account to pay interest on the account balance – possibly because of the assumption that many students will spend much of their time in their overdraft.

But, if you know you’re unlikely to go into negative numbers, your best bet is TSB, which pays a generous rate of 5pc on balances up to £500. Elsewhere, Lloyds Bank pays 2pc on balances up to £5,000.

With Halifax, you can earn 0.5pc on any account balance.

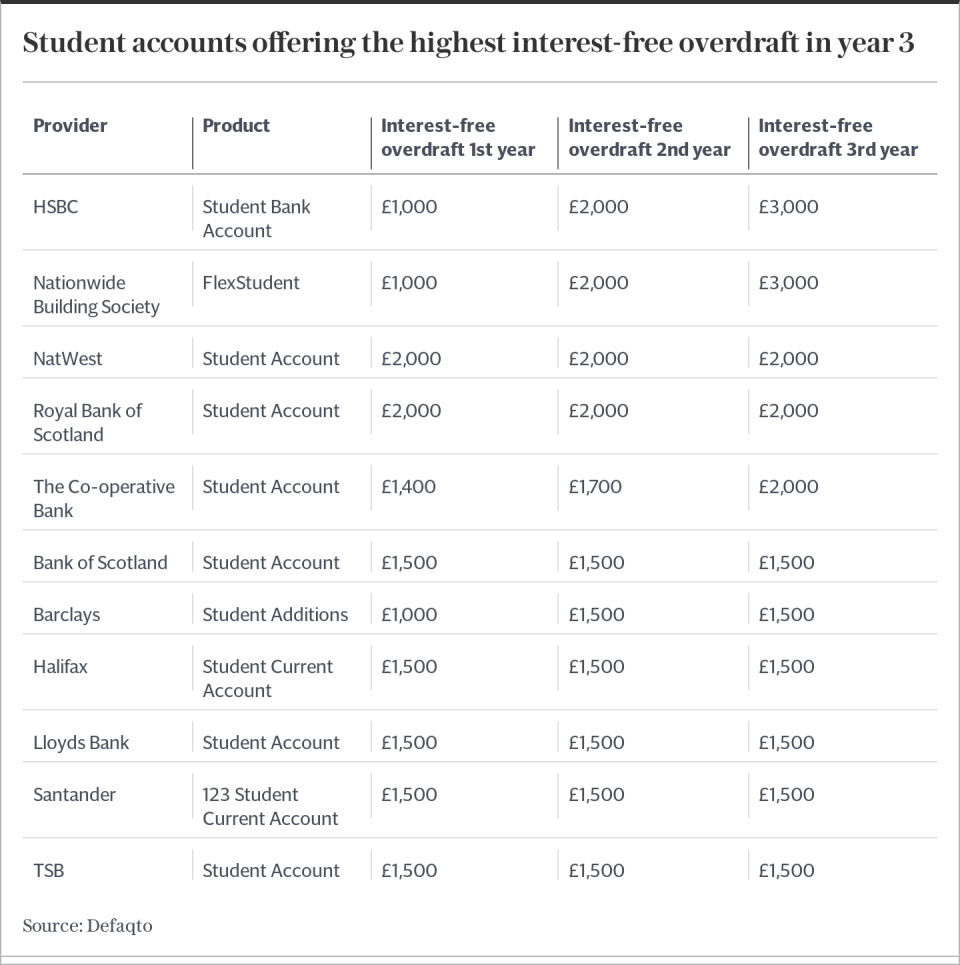

The best overdraft limits

The most generous interest-free overdrafts are with HSBC and Nationwide Building Society, offering up to £3,000 in the third year of study. In year one, they both offer up to £1,000, rising to £2,000 in year two.

A 0pc overdraft is particularly handy for students, who may have expenses to pay such as rent before they receive any student loans or grants. However, care must be taken to ensure you don’t breach the overdraft limit, or you could be liable for fees and interest of up to 40pc.

Some banks offer overdrafts that are “guaranteed”, while others offer “up to” overdrafts, which depend on your credit record.

The HSBC student account offers a guaranteed £1,000 interest-free overdraft in the first year, but the higher limits aren’t guaranteed in later years.

Katie Brain, banking expert at Defaqto, said: “Most students need access to an arranged overdraft to help with their living expenses. It is always important to remember this is a debt that needs to be paid back, so use it sparingly.

“Some providers also require a minimum amount to be credited to the account each term to qualify for an overdraft or extended amount.”

Nationwide and Santander both require customers to pay in at least £500 each term.

The best benefits

The best freebie depends on what you actually want and might use. A free meditation app is of no interest if you don’t want to meditate, and a free railcard has little value if you rarely take the train.

Students looking for some free money – that doesn’t need paying back – should consider Halifax, HSBC, Lloyds Bank, Nationwide, NatWest and RBS.

Last year, NatWest offered an £80 bonus, but this has now been upped to £100. The bank is also providing a free four-year tastecard, which gives 25pc off food or two-for-one meals at certain restaurants (worth £119.96).

HSBC is again offering £100 in free cash, and has added a new perk with a one-year subscription to Headspace, a wellbeing and meditation app (currently worth £34.99).

Halifax and Lloyds Bank offer £100, plus cashback of up to 15pc when shopping with certain retailers.

Nationwide’s offer is currently just the £100 payment.

Santander’s student account offer doesn’t include cash, but it is still valuable – its four-year 16-25 railcard gets you a third off rail travel in the UK. A three-year railcard costs £70 and a one-year card costs £30, meaning you save £100.

You can also sign up for Santander Boosts to receive cashback, offers and prize draws from brands including Tesco, Decathlon and Caffe Nero.

Read now: How to prepare for a job interview (and demolish your competition)

The best for using abroad

If you plan to travel a lot, the only provider with a student account that is fee-free when used overseas is Nationwide.

Using other debit cards abroad can see you get stung with charges of up to 4.75pc, which if you’re going away for several weeks can add up to more than £100.

The best student credit card providers

Student credit cards work in the same way as normal credit cards, except that they accept students.

Given most students will have what’s called a “thin credit file” – that is, little they won’t have held many financial products or have enough information on their file to prove to a bank that they are a trustworthy borrower – often your only credit card choice will be the same provider as your student current account.

Note that student credit cards are likely to have low credit limits and high interest rates, so they’re not ideal for borrowing – if you decide to get one, make sure you can pay it off in full at the end of each month.

Read now: The most common job interview questions – and how you should respond