Yahoo Finance

Yahoo Finance Big Risks Will Hound Japan’s Longest Bonds Even as Supply Falls

(Bloomberg) -- Japan’s super-long bond issuance looks set to drop, but it’s a case where less still means more than the market may be able to handle.

Most Read from Bloomberg

Democrats Weigh Mid-July Vote to Formally Tap Biden as Nominee

Trump Immunity Ruling Means Any Trial Before Election Unlikely

Beryl Becomes Earliest Ever Category 5 Hurricane in Atlantic

‘Upflation’ Is the Latest Retail Trend Driving Up Prices for US Consumers

Trump Isn't Going to Like the Supreme Court's Immunity Decision

The government appears to be striving to calm down a market that’s wracked by rising yields, and is considering decreasing sales of longer-dated debt and boosting offerings of shorter maturities. The problem is that the elevated risk of large capital losses for the longest bonds means that the supply of those securities will have a greater risk-adjusted impact on the market.

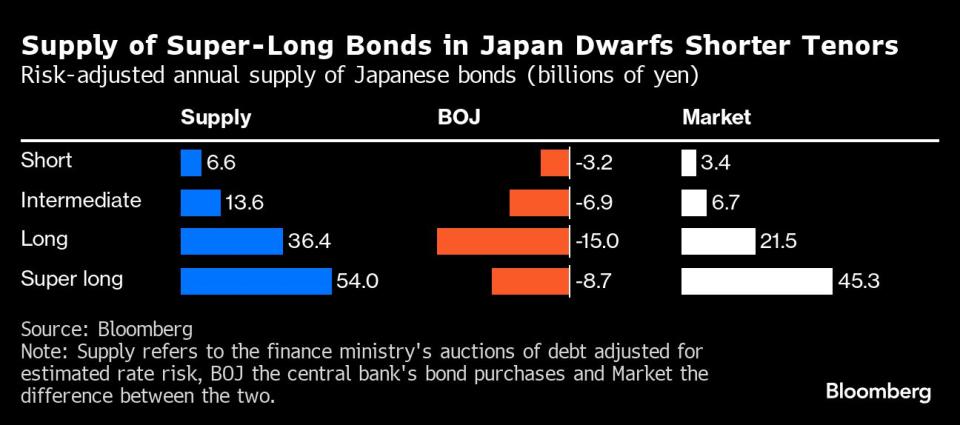

Supply of super-long debt is projected to total almost ¥30 trillion ($186 billion) in the fiscal year started April 1, according to the Ministry of Finance’s issuance plan and its communication with market participants. But for bond investors trying to keep track of risky assets in their portfolios, that figure may understate the potential losses from holding Japanese government notes with tenors longer than 10 years that tend to be more sensitive to the market’s interest-rate outlook.

The stark challenges facing Japan’s policymakers underscore the difficulty of exiting decades of radical stimulus and making Bank of Japan policy ‘normal.’ The central bank wants to cut its holdings of government bonds that ballooned to more than half of all outstanding debt, but it needs to juggle two somewhat conflicting goals: trying to keep borrowing costs from surging and hurting the economy, while preventing the yen from weakening even more on speculation it will raise rates only very slowly.

The degree of market concern toward Japan’s super-long debt can be seen in the gap between 30-year and benchmark 10-year yields. The spread expanded to about 122 basis points last week, the widest since late 2022, and more than twice as much as its equivalent in France, where concern over increased fiscal outlays spurred a selloff in bonds.

The risk of holding super-long debt now is more like if supply were much larger, Bloomberg analysis shows. Even after taking account the Bank of Japan’s debt purchases, investors face potential losses of ¥45.3 billion on each one basis-point rise in longer-maturity bond yields this fiscal year, compared with ¥21.5 billion for 10-year notes using that analysis. This happens just as the BOJ is expected to announce at the end of this month a plan to cut bond buying.

“There is an oversupply of super-long bonds,” said Ayako Sera, a market strategist at Sumitomo Mitsui Trust Bank Ltd. in Tokyo. “The BOJ’s purchases have been providing some anchoring for their yields, but that anchor is about to come loose.”

Not all indicators in Japan are pointing to gloom in the super-long debt market. A 20-year bond auction last week, for example, drew a higher cut-off price than traders estimated, signaling solid investor demand.

Still, uncertainty over how much the BOJ will decrease its bond buying and elevated inflation in Japan partly fueled by the weak yen mean any rally in super-long debt may be short-lived.

“Auctions could come out decent, but in the long run super-long bond yields are biased higher,” said Shoki Omori, chief desk strategist at Mizuho Securities Co. in Tokyo. “Sectors like 20-year are going to underperform unless the reduction in issuance is big.”

--With assistance from Saburo Funabiki and Masahiro Hidaka.

Most Read from Bloomberg Businessweek

The Fried Chicken Sandwich Wars Are More Cutthroat Than Ever Before

Japan’s Tiny Kei-Trucks Have a Cult Following in the US, and Some States Are Pushing Back

RTO Mandates Are Killing the Euphoric Work-Life Balance Some Moms Found

The FBI’s Star Cooperator May Have Been Running New Scams All Along

©2024 Bloomberg L.P.