Yahoo Finance

Yahoo Finance The Bottom May Be in for British American Tobacco

Warren Buffett (Trades, Portfolio) once said, We get paid, not for jumping over seven-foot bars, but for stepping over one-foot bars.

At 6 times free cash flow with a hidden asset, British American Tobacco PLC (NYSE:BTI) looks like a one-foot bar. As such, I am bullish on the stock.

British American Tobacco is the world's largest tobacco company by assets. It has a dominant economies of scale position and a fast-growing non-combustibles business. Moreover, the company has historically enjoyed recession-resistant demand. Investors have been selling, due to some obvious headline risks, but I believe the stock may have already bottomed.

A glaring value at 6 times free cash flow

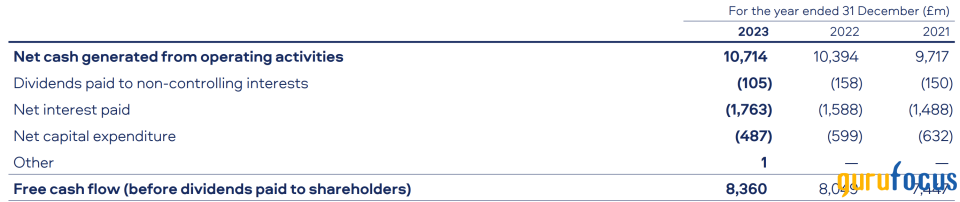

British American Tobacco took a non-cash write-down in 2023, affecting its net income and earnings per share. This had no effect on the company's cash generation. Looking at its free cash flow, it has grown at a 6% compound annual rate over the past two years.

Around 8.36 billion British pounds of 2023 free cash flow translates to $10.45 billion U.S. dollars. At a market cap of $65 billion, British American Tobacco's price-to-free cash flow ratio is just 6.20. This 16% free cash flow yield means the company's 10% dividend is well covered.

The hidden asset

British American owns 25% of ITC Ltd. (BOM:500875), a fast-growing conglomerate in India. ITC's market cap is nearly $66 billion, meaning the stake is worth a whopping $16.50 billion, representing 25% of British American market cap. To get the market to account for this hidden asset, the company has been selling some of its ITC shares at a price-earnings ratio of 25 to buy back its own shares at a normalized price-earnings ratio of 6. I view this as capital allocation at its finest.

A wide moat

Not only is British American Tobacco cheap, but it also has a wide moat. The company's enormous scale gives it bargaining power over its suppliers (in this case, tobacco farmers). This same scale makes the company more efficient than its smaller competitors when distributing its products to gas stations and shops worldwide.

British American Tobacco also operates in an industry with favorable competitive dynamics. Strict regulations and advertising bans keep smaller competitors and new entrants at bay. This is why you see the industry being dominated by oligopoly players British American, Philip Morris International Inc. (NYSE:PM) and Altria Group Inc. (NYSE:MO). However, Altria operates primarily within the United States, whle Philip Morris operates primarily outside the U.S., meaning British American Tobacco only has one major economies of scale competitor in each of its main markets. This is why cigarette prices tend to increase alongside inflation and why the company enjoys such healthy profit margins.

A recession-resistant product

I view British American Tobacco as a cornerstone in my portfolio; it is my only consumer staples company in a portfolio comprised primarily of cyclical companies. Tobacco is an essential product for many consumers, so its demand tends not to fall off in a recession.

For instance, British American Tobacco actually grew its cash from operating activities from year-end 2007 to year-end 2009. The same thing happened during the 2020 unemployment spike. If a recession should rear its ugly head, this consistent cash flow will allow me to redeploy the company's enormous dividends into beaten-down stocks. In effect, I will use the dividends to achieve what Einstein called the eighth wonder of the world, compound interest.

Non-combustibles are growing at a blistering pace

Big tobacco companies are slowly transitioning their product portfolios toward non-combustibles, which are seen as reduced-harm products. This move looks similar to Coca-Cola (NYSE:KO) introducing Diet Coke in the 1980s, a product that helped reduce weight gain and other health consequences of heavy sugar intake. Many people do not realize that nicotine itself does not cause cancer; it is the combustion process that releases carcinogens. I am optimistic that non-combustibles will improve upon the health effects of their predecessor, cigarettes, and lead to a brighter future for all.

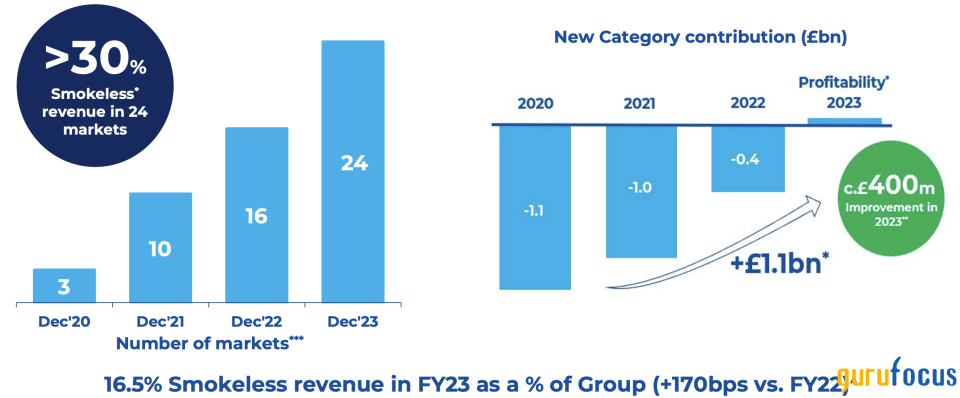

British American Tobacco has a strong portfolio of non-combustibles. The company's new categories segment now makes up 16.50% of its revenue, and it became profitable two years ahead of schedule.

Some believe non-combustible products could be just as profitable as combustible cigarettes as they scale. Evan Tindell of Bireme Capital concluded British American's non-combustibles could enjoy lower sales tax. Moreover, if we look at a scale provider of non-combustibles like Philip Morris, its profitability remains robust. The company's consolidated profit margins are expected to grow over time due to low manufacturing costs associated with non-combustibles.

Risks

British American Tobacco is facing some issues in the U.S., including a potential menthol cigarette ban. However, the government recently reversed course, saying it will take more time to reach a conclusion on the ban. It remains unclear whether or not this ban will ever go through, but I am not worried about it because it just adds to the long list of regulations that big tobacco companies have had to overcome. I think substitution, in this case, would mean consumers simply switch to another product of the same brand or a non-combustible product.

Also, a bunch of illicit vapor products have been circulating in the U.S. As regulators crack down on this, I think British American Tobacco could see an increase in sales. Still, the market seems to be concerned, given the stock's valuation.

Summary

British American Tobacco is a cornerstone of my portfolio. At 6 times free cash flow, it seems as easy as stepping over a one-foot bar, Buffett style. The company has a $16.50 billion hidden stake in ITC, which it has trimmed in order to buy back its own shares. The company operates in a highly regulated oligopoly with an economies of scale position. This, along with its recession-resistant products, allows it to gush cash throughout the economic cycle.

The risks surrounding British American Tobacco's business seem to be dissipating. The non-combustibles business reached profitability two years ahead of schedule, and Philip Morris' results point to healthy margins for these reduced-risk products. Lastly, the U.S. government temporarily cancelled its ban on menthol cigarettes and may crack down on illicit vapor products, boosting sales for the traditional tobacco company. While nobody knows for sure, I think the bottom is already in.

This article first appeared on GuruFocus.