Yahoo Finance

Yahoo Finance Should You Buy META (META) Ahead of Q1 Earnings?

Meta Platforms META is slated to report first-quarter earnings on Apr 24, 2024. The Zacks Consensus Estimate for earnings is pegged at $4.32, while the Most Accurate Estimate is $4.35, leading to an Earnings ESP of +0.62% for the Zacks Rank #2 (Buy) company.

The social media giant saw a positive earnings estimate revision of a penny for the to-be-reported quarter over the last 7 days and 5 cents over the past month. Analysts increasing estimates right before earnings — with the most up-to-date information — is a good indicator for the stock.

Let’s analyze the Meta stock in detail.

Bull Case Scenario

While Meta is sharing its foundational "Llama" models with developers, proprietary data and product implementations are still private. Meta's user data gives it an edge over peers in training their AI models. This user advantage helps Meta create engaging AI experiences, which leads to increased user engagement and higher advertising revenues, favoring advertiser ROI.

Reels are acting as a tailwind, per some market watchers. A TikTok ban would be a win for this segment’s monetization. Moreover, ad spending growth has remained resilient, buoyed by higher prices.

Per Skai, a leading omnichannel advertising platform, average cost-per-click (CPC) increased 13% year over year in paid search of the digital marketing field in Q4 of 2023. Meta proved to be a key beneficiary of this trend. Spending on product ads on Meta grew massively in Q4 of 2023. We expect this winning trend to have continued in Q1 of 2024.

Factors to Boast About

The stock currently belongs toa top-ranked Zacks industry (top 22%) and a top-ranked Zacks sector (top 31%).

Solid Track of Beating Analysts’ Estimates on Non-Financial Metrics

Meta’s advertising revenues topped analysts’ estimates in the last four quarters for all geographic sectors, except US & Canada. In the previous six quarters, advertising revenues missed only in the September quarter in North America.

Daily Active Users (DAUS) worldwide also topped analysts’ estimates in the last for quarters. Monthly Active Users (MAUS) worldwide also surpassed analysts’ estimates in three out of the last for quarters.

Worldwide average revenue per user (ARPU) breezed past analysts’ consensus estimates in the past four quarters, while the same metric emerged winner for North America in the past five quarters.

Upbeat Growth Compared With the Industry

The current Zacks Consensus Estimate for the yet-to-be-reported quarter indicates substantial earnings growth of 63.6% from the prior-year quarter, way higher than the industry’s growth rate of 28.8%. Revenues are expected to increase 26.6% versus 16.7% of the industry. Meta Platforms delivered an earnings surprise of 19.71%, on average, in the last four quarters. The estimated five-year growth rate of Meta is 19.5% versus 17.1% growth rate of the industry.

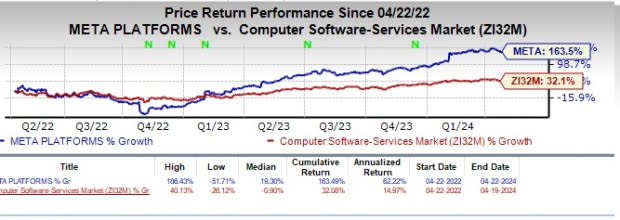

Meta Stock Currently Enjoying High Momentum

The Meta stock has an upbeat Momentum Score of A and returned about 40% this year and 127% in the past year.

Image Source: Zacks Investment Research

Compelling Valuation

P/E (TTM) of Meta stands at 30.9X versus 34X possessed by the underlying industry. P/E of the upcoming year of the stock stands at 23.8X versus the 28.6X ratio held by the industry.

Wall of Worry

Some valuation metrics like price/sales, price/book and price/cash flow are a little overvalued. Price/Sales of the stock is 9.4X versus 5.2X possessed by the industry. Price/book ratio of the Meta is 8.0X versus 5.3X recorded by the industry. Price/Free Cash Flow is 28.7X versus 21.7X reported by the industry.

Bottom Line

Investors should not be bogged down by the slightly rich valuation of some metrics. Meta’s huge global presence with a dependable user base, continuous innovation on the advertising front, which could boost monetization, a deeper focus on e-commerce advertising solutions, AI initiatives, a strong presence in virtual reality and the Metaverse make the stock a buy.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Meta Platforms, Inc. (META) : Free Stock Analysis Report