Yahoo Finance

Yahoo Finance Cash Isas – A comprehensive guide

If you have money to save then a cash Isa should be one of your considerations. It works in a similar way to a savings account, except that you’re limited to how much you can pay in each year (up to £20,000), and the interest your money earns will remain tax-free.

There are several types of cash Isas to choose from and they’re offered by lots of banks and building societies, as well as National Savings & Investments.

If you’re not sure quite where to start, Telegraph Money will explain the basics of cash Isas in this guide, which will cover:

Introduction to cash Isas

Cash Isas were launched in 1999 with the aim of helping savers reduce their tax bills.

While they went out of fashion when savings rates were at record lows – as there was little risk of savers earning enough in interest to trigger a tax bill – recent rising rates means they have an important role to play once again.

With savings rates reaching upwards of 6pc last year, and with many still above 5pc, more people are breaching their “personal savings allowance” (more on this below) with far smaller amounts of savings – and are therefore at risk of having to pay tax on their interest.

If you’re trying to keep some of your cash out of the taxman’s clutches – not just now, but years in the future – the idea of saving tax-free in an Isa is likely to be very attractive.

Benefits of a cash Isa

Cash Isas allow you to pay in up to £20,000 a year, and earn interest free of income tax.

By sheltering money in a cash Isa you can keep more of the interest you earn in your own hands – and cash Isas are tax-free for life. As your savings grow, building with compound interest, an Isa means you can shelter more and more interest from the tax man.

This is particularly important in the current economic climate. Laith Khalaf, from AJ Bell, said: “For the first time in over a decade, tax on cash interest rates has become a serious problem for savers. With interest rates expected to stay higher for longer, and tax bands frozen, consumers need to take steps to protect themselves from tax.”

What’s more, cash Isas are easy to set up, and simple to operate.

Mr Khalaf added: “These vehicles are good for storing money that you might need at the drop of a hat. Unlike a stocks-and-shares Isa, the value of your cash Isa will never fall.”

Here we take a closer look at how Isas work.

Types of cash Isas available

While cash Isa interest rates have likely peaked, you can still get your hands on a competitive inflation-busting deal. There are several different types of cash Isa on the market, so make sure you know which one suits you best before you part with your savings.

Fixed-rate cash Isas

If you are happy to lock your money away, better rates are likely to be available on fixed-rate Isas, compared to variable cash Isas. However, they require you to commit to locking your money away for a set period of time, typically between one and five years.

If you need to withdraw your money before the end of the fixed term you’re likely to face a penalty – often, providers will charge you a certain amount of interest on the sum you’re withdrawing.

Variable-rate cash Isas

Also known as “easy-access” Isas, with this type of account you can usually get your hands on your money whenever you need it, penalty-free. That being said, individual accounts may have their own, more restrictive withdrawal rules.

The main drawback to this kind of cash Isa is that rates can change at any time – so you could find yourself earning a lower rate of interest at any time.

You also need to keep a close eye for any bonus rates which may bump up the interest rate when you first open the account. If there is one, make a note to move your money to a more competitive deal once the bonus drops away.

Notice cash Isas

Isas with a notice period tend to have slightly better rates than easy-access accounts (but this isn’t always the case). In theory, the longer the notice period, the higher the rate of interest is likely to be.

Be aware that with a notice Isa, you must give a certain number of days’ notice before you can withdraw your funds. This can vary, but is most commonly between 30 days to 180 days. You need to bear this in mind if you think there might be a scenario when you’ll need to get fast access to your cash.

Regular cash Isas

Specific terms will vary, but they commonly have a set amount that you can pay in each month – sometimes a deposit is required in order to get the advertised interest rate. You might be able to make withdrawals, but those offering a higher rate might not allow them.

Note that the advertised interest rate might sound high, but as you’re usually restricted to gradually paying in relatively low amounts, the actual interest you’ll earn will be fairly low.

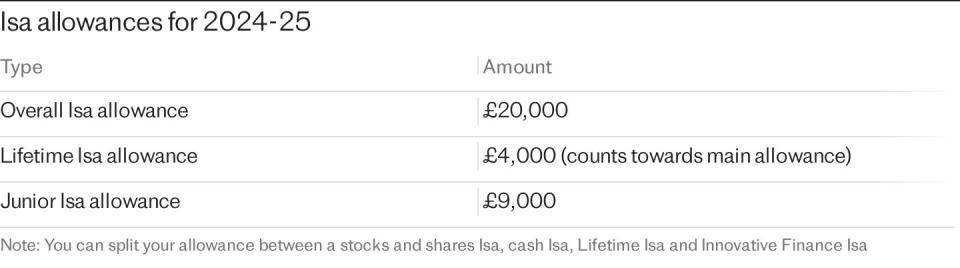

Lifetime Isas

Technically, lifetime Isas are their own separate type of Isa – they have a different deposit limit (£4,000), and the money is meant to fund either your first home or retirement. However, we are mentioning them here since there are cash Isa options. You can find out more in our guide to Lisas.

Junior cash Isas

For children under the age of 18, parents or guardians have the option to open a Junior Isa for them – there are cash Isa options, as well as Junior stocks and shares Isas.

How to choose the right cash Isa for you

There are certain savers who would do well to consider a cash Isa.

Mr Khalaf said: “Cash Isas are well suited to those building up a rainy day fund, and those saving for short-term spending needs – with the money needed in the next five years or so.”

But how do you decide which type is right for you?

If you require some flexibility and think you might need to take money out of the account often, an easy-access cash Isa is likely to be the best option for you.

Rates tend to be higher on fixed-rate cash Isas, but you need to be happy about the idea of locking your cash away for the full period. Generally speaking, the longer you fix for, the higher the rate.

That said, it’s important to be wary of locking savings away for too long, as you risk missing out if savings rates go up. You could find yourself stuck in an account that is no longer competitive. Telegraph Money compiles the best savings rates every week.

When you’ve found a cash Isa that’s right for you it’s worth getting your skates on, as the top deals may not hang around for long. Rachel Springall, finance expert at Moneyfactscompare.co.uk, said: “Offers can change quickly, so speed is crucial to grab a top rate.”

After tucking money away in a cash Isa it’s key to review it regularly to ensure it’s still paying a competitive rate.

Ms Springall added: “Inflation eats away at savers’ hard-earned cash, so it’s worth keeping this in mind when comparing accounts to ensure you’re earning a decent real return.”

Understanding the tax benefits

One of the biggest benefits of a cash Isa is the fact that this vehicle protects your savings from tax.

As a saver, you need to take care not to breach your “personal savings allowance”. This is the limit on interest you can earn tax-free, and applies to the interest you earn across all accounts.

Your allowance depends on your tax band – i.e. the highest rate of income tax you pay. It is £1,000 for a basic-rate taxpayer, and just £500 for a higher-rate taxpayer. Additional-rate taxpayers pay tax on all their interest.

Now that savings rates are higher and income tax thresholds are frozen, more people are breaching their personal savings allowance; smaller pots of savings are earning more money, while people’s allowances are reducing if they get dragged into a higher tax band. This is when sheltering your hard-earned savings in a cash Isa becomes so much more important.

FAQs

How much can I have in a cash Isa each year?

Under current rules, the annual Isa allowance is £20,000. You can opt to put up to £20,000 in one Isa, or split it among several. This £20,000 allowance has not changed since 2017.

What has changed, as of April 6, 2024, are the rules on paying into multiple Isas of the same type (with the exception of a lifetime Isa). Previously, in any one tax year, you could only open – and pay into – one of each type of Isa. Minor reforms mean it’s now possible to subscribe to more than one of the same type of Isa in a single tax year. This could, for example, involve you paying into two cash Isas if you so wish.

Note that if you don’t use your Isa allowance, you lose it, as it cannot be carried over to the next tax year.

Can I transfer my cash Isa?

Yes. If you have a cash Isa, you are allowed to move your money between providers at any time – and you can also move it to a different type of Isa, as long as the provider accepts transfers. But you must follow the official “Isa transfer” rules to ensure the funds remain under the protection of the tax-free wrapper.

If you withdraw money from your cash Isa to your bank account before putting it into a new cash Isa, your hard-earned savings will lose their tax-free status while they’re not held in an Isa, and the deposit will also be deducted from your Isa allowance. Transferring existing Isa savings directly between providers won’t incur these problems.

Ms Springall said: “You must ensure you transfer the cash in accordance with the rules to keep its tax-free wrapper. But note that not every cash Isa will allow transfers in from cash Isas – or stocks and shares Isas.”

Be sure to check this ahead of making any move.

In any one tax year, you can make as many transfers as you wish. Also note that following new rules which kicked in from April 6 2024 you can now make partial transfers of Isas.

What happens to my cash Isa if I move abroad?

Rules state that when you go overseas you are no longer allowed to pay into your Isa after the end of the tax year that you move.

Beyond this date, for tax purposes you are no longer a British resident and will not be eligible for an Isa. The only exception is if you are a Crown employee working abroad, such as a diplomat, civil servant or member of the armed forces.

You need to let your Isa provider as soon as you stop being a British resident.

The good news is that even if you no longer live in the UK, any existing Isas you have will remain open and active and you will be able to go on benefiting from tax relief on any cash held in your accounts. You are also still allowed to transfer your Isa to another provider.

Note though that the tax rules may be different in the country you’ve moved to, and that you could be required to pay tax in your new country on the money earned from your Isa – you need to check this.

If you do return to the UK and become a British resident once again, you will be able to start paying into your Isa (subject to the annual £20,000 allowance).