Yahoo Finance

Yahoo Finance Central Garden & Pet (CENT) Up 39% in a Year: What Lies in 2022?

Central Garden & Pet Company CENT appears well poised for growth, thanks to its robust business strategies. CENT has been strengthening its position in the pet supplies, and lawn and garden supplies space via prudent acquisitions for a while. The retailer is developing new products, advancing digital capabilities, optimizing supply chain and focusing on marketing activities. These endeavors will continue aiding the overall performance in 2022.

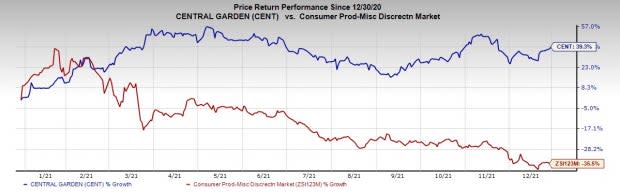

Shares of this presently Zacks Rank #2 (Buy) player have surged 39.3% in a year against the industry’s 36.5% decline. The Zacks Consensus Estimate for Central Garden & Pet’s next financial-year sales and EPS suggests growth of 3% and 10.4%, respectively, from the corresponding year-ago reported figures. A VGM Score of A further exhibits strength.

Let’s Analyze Further

To reinforce its footprint, Central Garden & Pet continues to be a disciplined buyer in the garden and pet areas. In fact, acquisitions are a key component of CENT’s strategy. The retailer has expanded its business via more than 60 acquisitions since 1992. Through these buyouts, management aims to enhance its manufacturing capabilities, operating synergies and distribution network as well as advance its key capabilities in digital and e-commerce domains. Certainly, these acquisitions are enriching Central Garden & Pet’s portfolio and customer base, fueling the top line in turn.

Some notable acquisitions in the recent past include that of D&D Commodities Ltd. (D&D), a leading provider of premium bird feed, in June 2021; Green Garden Products, a leading provider of vegetable, herb and flower seed packets, seed starters and plant nutrients, in February 2021; and Hopewell Nursery, a leading live goods grower, in January 2021.

Image Source: Zacks Investment Research

Speaking of its digital initiatives, the buyout of DoMyOwn.com is steadily advancing CENT’s digital capabilities to deliver a strong omni-channel performance. The purchase of DoMyOwn.com, a fast-growing online retailer of professional-grade control products, is fortifying the buyer’s position in the control product space. The deal adds best-in-class e-commerce fulfillment platform and digital capabilities to Central Garden & Pet’s portfolio, thus helping the same cater to rising e-commerce demand. CENT also partnered with the leading e-commerce platform of Profitero, Inc. This partnership provides CENT with a full view of its e-commerce business across eight retail partners.

Central Garden & Pet intends to develop differentiated products, improve sales capacity, respond to channel shifts and become more cost-effective. Unique packaging, point-of-sale displays, logistic capabilities and a high level of customer service are also key catalysts.

Bottomline

Driven by these strengths, CENT’s both garden and pet businesses are consistently performing well. While the Garden segment is benefiting from recent accretive buyouts and higher gardening activities, the Pet unit is aided by significant contributions from dog treats and chews, distribution, outdoor cushions and animal health.

Wrapping up, we believe, all the aforementioned initiatives will keep yielding favorable results ahead.

Don’t Miss These Solid Consumer Discretionary Bets Too

Delta Apparel DLA, the manufacturer of activewear and lifestyle apparel products, sports a Zacks Rank #1 (Strong Buy) at present. The stock has surged 40.2% in the past year. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Delta Apparel’s next financial-year sales and EPS suggests growth of 9.3% and 12.4%, respectively, from the year-ago corresponding figures. DLA has a trailing four-quarter earnings surprise of 95.5%, on average.

Kontoor Brands KTB, a lifestyle apparel company, flaunts a Zacks Rank of 1 at present. The stock has increased 25.2% in the past year. KTB has an expected EPS growth rate of 8% for three-five years.

The Zacks Consensus Estimate for Kontoor Brands’ next financial-year sales and EPS suggests growth of 7.8% and 13.3%, respectively, from the year-ago corresponding figures. KTB has a trailing four-quarter earnings surprise of 22.2%, on average.

Under Armour UAA, the designer and marketer of athletic footwear, apparel and accessories, has a Zacks Rank of 2, currently. UAA has a trailing four-quarter earnings surprise of 244.5%, on average. Shares of UAA have jumped 20.8% over the past year.

The Zacks Consensus Estimate for Under Armour’s next-year sales and EPS suggests respective growth of 6.1% and 5% from the year-ago corresponding readings. UAA has an expected EPS growth rate of 25% for three-five years.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Central Garden & Pet Company (CENT) : Free Stock Analysis Report

Delta Apparel, Inc. (DLA) : Free Stock Analysis Report

Under Armour, Inc. (UAA) : Free Stock Analysis Report

Kontoor Brands, Inc. (KTB) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research