Yahoo Finance

Yahoo Finance Chinese Bond Traders Fear ‘Dagger to the Heart’ as Yields Vanish

(Bloomberg) -- Chinese bond traders have few things to celebrate despite this year’s unprecedented market rally.

Most Read from Bloomberg

Microsoft Orders China Staff to Use iPhones for Work and Drop Android

Biden’s Biggest Donors Left Powerless to Sway Him to End Bid

Zyn Imitators Rush In as Online Sales Halt Worsens US Shortage

Rich Chinese Return to Hong Kong as Singapore Steps Up Scrutiny

Asia’s Richest Banker Gets Caught in Adani-Hindenburg Crossfire

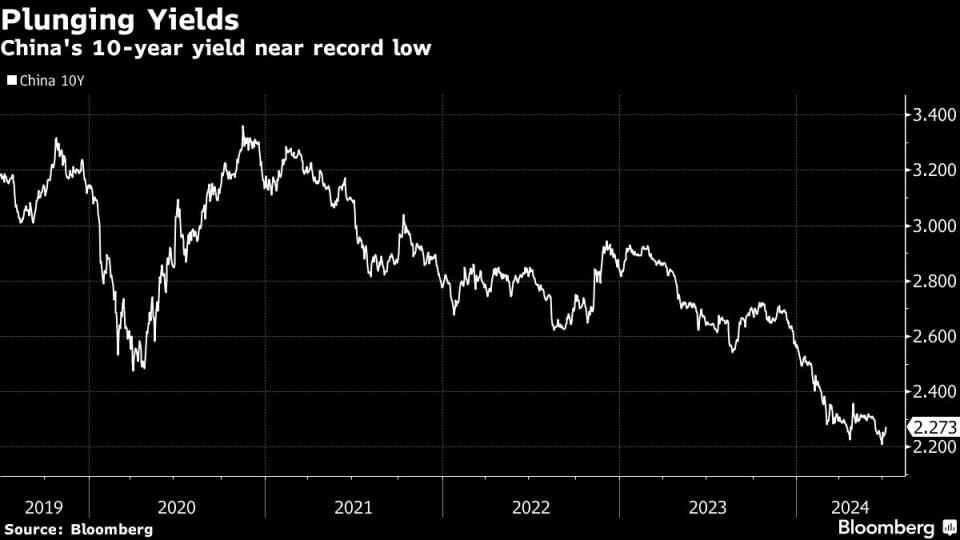

A sluggish economy has pushed the nation’s sovereign bond yields to record lows, sparking anxiety across trading desks at securities firms, banks and fund managers that ever lower rates will dry up trading and cost them their jobs.

In just the past week China’s central bank has taken two major steps to tighten its grip on short- and long-term yields, moves that may reduce opportunities to profit from market volatility even if borrowing costs don’t immediately plunge further from here.

It’s a landscape well-known to fixed-income professionals across the globe, which in the post-financial crisis era was mired in rock-bottom and even negative interest rates. China’s traders are now studying how their counterparts in Japan, in particular, weathered decades of minuscule yields.

“The downtrend may persist for many years, before we reach the limits of ultra-monetary easing and rates hit zero,” Zhu Zhenxin, chief economist of Asymptote Investment Research, wrote in a report last week.

The gloomy outlook is casting a pall on the industry, already contending with increased Communist Party control, sinking salaries and a slump in dealmaking.

Lawrence, who works in fixed income at a big brokerage in Beijing, described it as “a dagger to the heart.” He anticipates the bond market will shrink drastically should yields hit zero, with little participation from retail investors or asset managers, leading to severe job losses.

His firm is studying what happened in Japan, where rates are now finally on the rise after 17 years, to get “mentally prepared,” he said, asking that his full name not be used discussing private matters.

Compounding their worries is a growing wave of pay cuts and layoffs as China’s $66 trillion finance industry struggles to comply with President Xi Jinping’s “common prosperity” campaign. That means any profits traders made from the bond rally this year won’t necessarily translate to a bump in their salary or bonus.

At a big bank’s wealth arm in Shanghai, weekly meetings are often spent fretting about how long their bond careers will last, according to John Wang, a trader who asked his company name not be disclosed discussing a private matter.

China’s soaring bond prices are little consolation to traders worried about their long-term prospects. An aggregate index for Chinese debt has gained 3.88% this year, outperforming all regional markets, according to data compiled by Bloomberg.

Alex Hu, who oversees proprietary trading at a mid-sized brokerage in Shenzhen, said treasury bond investments have contributed to the majority of the division’s profits in recent years, but compensation hasn’t kept up. Thanks to the rally — bond prices rose while yields plummeted — Hu’s team was able to hit their 2024 revenue target in May and outperform it by 16% last month. Hu isn’t hopeful of the group’s prospects, after senior managers and executives’ pay were slashed 10% last year.

Hu said he’s grateful his salary hasn’t been cut yet, and that the profits his unit is generating at least mean that his job is safe, for now.

China’s gloom contrasts with Japan, where a return of inflation and slightly higher rates have revived a fixed-income market that had been dormant for decades. Banks and brokerages are scrambling to hire traders, particularly older staff who remember what it was like to trade bonds in the 1990s when debt was in demand and volatility led to more activity and fees.

The precipitous drop in yields is worrying the nation’s central bank, the People’s Bank of China. Policymakers have been seeking to talk up yields for months and are now preparing more drastic actions. The excessively low yields are seen as endangering financial stability and pressuring the yuan.

The PBOC said last week it had signed agreements with banks that have “hundreds of billions” of yuan worth of government bonds at its disposal to borrow. It had earlier signaled it would sell some notes to cool the rally.

That may not be enough to overcome the fundamentals steering the market. Sovereign bond prices have risen on persistent pessimism about the economy and bets on interest rate cuts. Demand was also bolstered as households and companies shifted their funds from bank deposits to investment products that pile into bonds amid a shortage of higher-yielding alternatives.

On Monday, the central bank also said it would add operations in the afternoon, in addition to its traditional morning operations, tightening its control over short-term interest rates and narrowing the interest rate corridor to reduce interbank volatility.

Yields on the onshore 10-year government bonds climbed to 2.285% as of late Monday, the highest in more than a month, yet not far from the record low of 2.18%. Yields on 30-year notes have been trading at around 2.51%, highest in 3 weeks, close to its lowest level since 2005. By contrast, the US 10-year Treasury bond yields about 4.31%.

China watchers had so far been skeptical about the central bank’s ability to guide yields higher. The operations might put a floor under yields in the near term, but the longer-term fundamentals driving yields lower remain intact.

“Irresistible”

Asymptote Investment expects China’s rates will continue to drop as it exits the debt-fueled boom era, with total financing demand gradually slowing. The country’s aging population, which will cut into its workforce and lead to economic growth “changing gears,” as well as the need for monetary easing to counter the slowdown, will weigh on interest rates.

Eventually, monetary easing will allow for higher inflation and a rebound in rates, Zhu said, citing an analysis of historic sovereign rate patterns from major economies, including the US and Germany.

“But before then, the rate downtrend in the long run is almost irresistible,” he wrote.

Others are more optimistic. Yongbin Xu, co-chief investment officer at U-shine Investment Group, said there will still be chances to make a profit, including on yield curve trading, derivatives and shorting. “The high-speed growth has passed, but that is not the end of the world,” he said. “People will keep doing investment and bond trading.”

Game Plan

Still, brokers and banks are stashing away profits to prepare for lean years ahead and potential losses, traders said. Others are seeking to diversify their portfolios to include overseas assets like US Treasuries and commodities like gold.

Heddie Li, an executive of a mid-sized mutual fund in Shanghai, said they trimmed their bond holdings last month to wait out the PBOC intervention and avoid making the wrong bets and go against the central bank.

A top mutual fund house in Shanghai has been studying the scenario of zero interest rates since last year, with economic fundamentals suggesting lower yields are here to stay, according to Ng, a fund manager.

“I don’t think China will necessarily have zero rate like Japan, but we are overdrafting the future returns with no doubt,” he said. “One can’t fight the tide of your times no matter how hard you struggle.”

--With assistance from Qizi Sun.

Most Read from Bloomberg Businessweek

At SpaceX, Elon Musk’s Own Brand of Cancel Culture Is Thriving

How Stocks Became the Game That Record Numbers of Americans Are Playing

©2024 Bloomberg L.P.