Yahoo Finance

Yahoo Finance Is Cisco Systems Inc's Stock Getting Overvalued?

Shares of Cisco (NASDAQ: CSCO) rose 27% this year, outperforming the S&P 500's 20% gain. That rally was surprising, since Cisco -- one of the biggest networking equipment makers in the world -- is generally considered a slow-growth investment.

So after that rally, should investors wait for a pullback before buying Cisco? Let's take a closer look at its growth and valuations to find out.

Image source: Cisco.

How fast is Cisco growing?

In fiscal 2017, Cisco's revenue (excluding the sale of its set-top box business) fell 2%, its net income dropped 11%, and its earnings per share declined 10%. Revenue from its core switching and routing businesses -- which accounted for nearly half its top line -- respectively fell 5% and 4%.

Cisco's collaboration and data center revenues also declined. Its higher-growth wireless and security businesses respectively posted 5% and 9% sales growth, but they couldn't offset the weakness of its other businesses. For the current year, analysts expect Cisco's revenue and earnings to respectively rise 1% and 3%.

Those growth figures look mediocre, but some encouraging figures during the first quarter brought back the bulls. Its revenue fell 2% annually, but its recurring revenues accounted for 32% of that total -- a three percentage point jump from the prior-year quarter. Its service revenues also rose 1%, partly offsetting a 3% decline in its product revenues.

Deferred revenue, a key indicator of forward demand, rose 10% to $18.6 billion. Within that total, its deferred product revenue rose 16%, driven by subscription-based and software offers, as its deferred service revenue grew 5%.

But do those valuations match up?

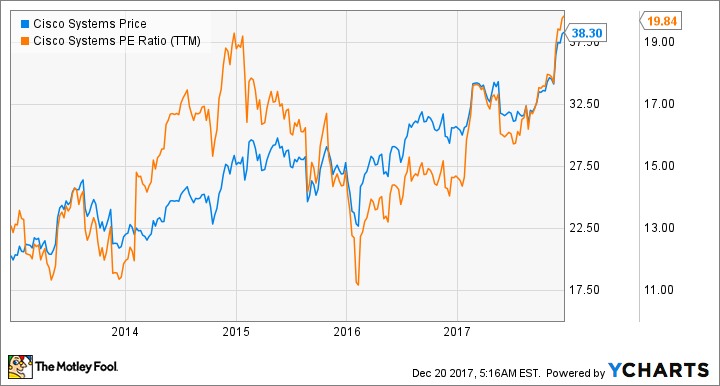

Cisco trades at 20 times earnings, which is lower than the industry average of 36 for communication equipment providers. But if we look at the long-term chart, we'll notice that Cisco's stock and its P/E ratio are both at a multi-year high.

Source: YCharts

This is troubling because Cisco's earnings growth rate has actually slowed down dramatically over the past few years:

Source: YCharts

Cisco's forward P/E of 16 looks more reasonable, but it's not necessarily cheap for a company with 3% earnings growth. Meanwhile, Cisco's price-to-sales ratio of 4 is also double the industry average P/S of 2.

Why is Cisco hitting multi-year highs?

I believe investors are mainly buying Cisco for two reasons -- its dividend and lower corporate tax rates. Its forward dividend yield of 3%, which is supported by a payout ratio of 59%, easily beats the S&P 500's 1.9% yield.

Cisco's dividend and stable business model makes it an ideal income play in a low-interest rate environment. But as interest rates rise, bonds will become more attractive and cause dividend stocks with higher valuations -- like Cisco -- to sell off.

The recent reductions in US corporate taxes -- which cut the 35% rate to 21%, and taxes on repatriated income from 35% to a range between 8% to 15.5% -- could allow Cisco to bring a large portion of its cash home for buybacks, dividends, and domestic acquisitions. Cisco finished last quarter with $71.6 billion in cash, cash equivalents, and investments, but just $2.5 billion of that total was available in the US.

That's definitely a positive catalyst, but there's no guarantee that Cisco will actually repatriate its cash from low-tax countries like Ireland, which has a corporate tax rate of just 12.5%. Therefore, these two bullish reasons for buying Cisco are a bit wobbly.

Mind the other challenges

Meanwhile, Cisco's core business faces tough challenges. Its market shares in the switching and routing businesses continue to drop, as both businesses lose ground to rivals like Huawei, Juniper Networks, and Arista Networks (NYSE: ANET).

Cisco also faces the growing threat of disruptive new technologies, like "white box" SDNs (software-defined networks) which use cheaper generic hardware and open-source cloud software. These solutions undermine Cisco's ability to lock in customers with hardware and software bundles, and reduce the amount of networking hardware companies have to buy.

Arista is a major threat in this market, since it sells cheaper multilayer network switches for white box networks. Its hardware runs on an open-source Linux-based OS, and its FlexRoute software replaces physical routers with software-based solutions.

The key takeaways

Cisco isn't a risky stock, but its valuations look a bit lofty at these levels. Investors should realize that the stock might be trading at a premium on lower interest rates and corporate tax cuts instead of bullish optimism for its core business, so it might be prudent to wait for a pullback before buying.

More From The Motley Fool

Leo Sun has no position in any of the stocks mentioned. The Motley Fool owns shares of and recommends Arista Networks. The Motley Fool recommends Cisco Systems. The Motley Fool has a disclosure policy.