Yahoo Finance

Yahoo Finance Civil service pensions: what they are and how they work

If you work in the public sector, you will have a workplace pension scheme like most other eligible employees in the private sector.

There is, however, a separate additional pension system for public sector workers, who account for about 20pc of the workforce and include NHS workers, teachers, military personnel, civil servants and police. Civil service pensions are designed to provide an income when you retire, but they differ from mainstream schemes for private sector workers.

Including both defined benefit schemes and defined contribution schemes, the civil service pension is considered very generous

Here we explain everything you need to know about civil service pensions and how they work. In this guide we cover:

What are civil service pensions?

Civil service pensions are for individuals who work in the public sector. In total there are now six types of civil service pension in operation, as the original scheme has been overhauled and reformed through the years.

There’s Classic, Classic Plus, Premium, Nuvos, Alpha and Partnership.

Which scheme you are a member of depends on when you joined the civil service.

However, you may be a member of one or more if you’ve worked in a role for a significant period of time and the schemes have changed over that period.

When this happens, you are usually given the option to remain in the existing scheme or to join the new one. If you decide to change, you can leave your existing savings in the old schemes, which is how you can end up with several schemes in tow.

If you join the civil service today, you will be given the choice to enrol in the Alpha or the Partnership scheme.

How do they work?

Like pensions in the private sector, for the civil service pension you and your employer will make contributions to your pension.

The majority of the contribution will be made by your employer, which for most civil service pensions schemes in operation is paid at 28.97pc of earnings.

No matter what part of the pension scheme you’re in, the employer makes the same contributions, according to how much you earn.

The amount you as the employee contributes is much lower, sitting between 4.6pc and 8.05pc depending on your annual salary.

The longer you work for the civil service, the more valuable your pension becomes and the higher the income you will receive.

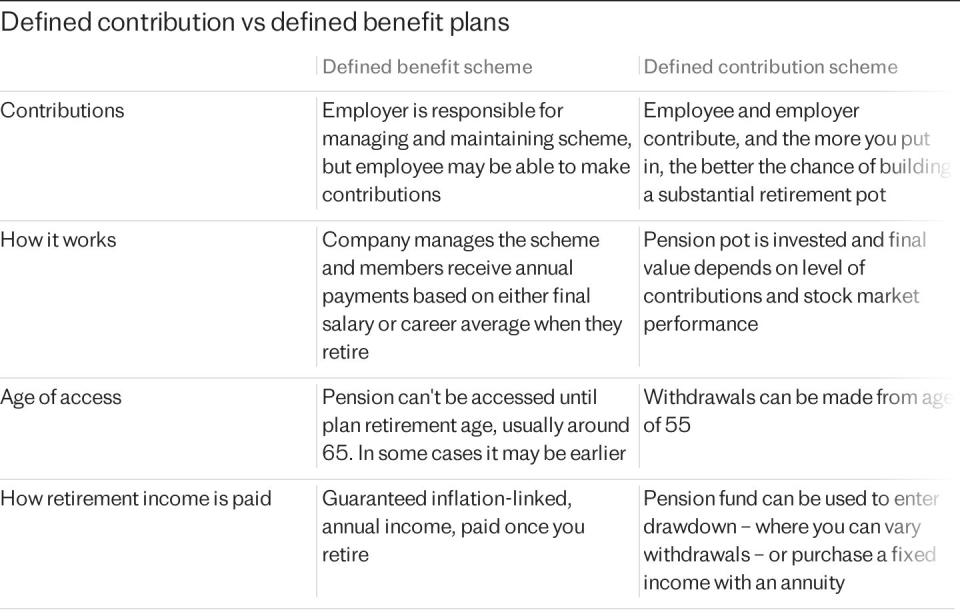

A civil service pension is similar to other workplace pensions in that your money is tied up in the scheme until retirement.

Should you leave the public sector, contributions will stop and your money will remain where it is until you start withdrawing an income from it – or transfer it.

You can claim your pension after you have stopped working entirely, or taken partial retirement.

This means you can choose to start taking an income from your pension if you’re still working, as long as you’ve reached the eligible age. This will depend on the scheme you’re a member of.

At this stage, if you’re a member of Classic, Classic Plus, Premium, Nuvos or Alpha, you will be able to draw on your civil service pension and will receive a guaranteed level of income.

These are defined benefit pension schemes, the most generous of all as they guarantee an inflation-linked income in retirement.

The pension income you receive will be worked out using a proportion of your final pensionable earnings for every year of service – not including breaks.

Ahead of your retirement date you will have an idea what your retirement income will be as your annual statement will feature a summary of your civil service pension benefits, up to the date of the statement each year, based on your current salary.

You can usually choose to give up part of your pension for a tax-free lump sum.

Sometimes you can take partial retirement which means you carry on working on a part-time basis and receive a portion of your pension for the days you don’t work.

For those in the Partnership pension your income in retirement will depend on the size of the pot you have accrued, as it’s a defined contribution scheme.

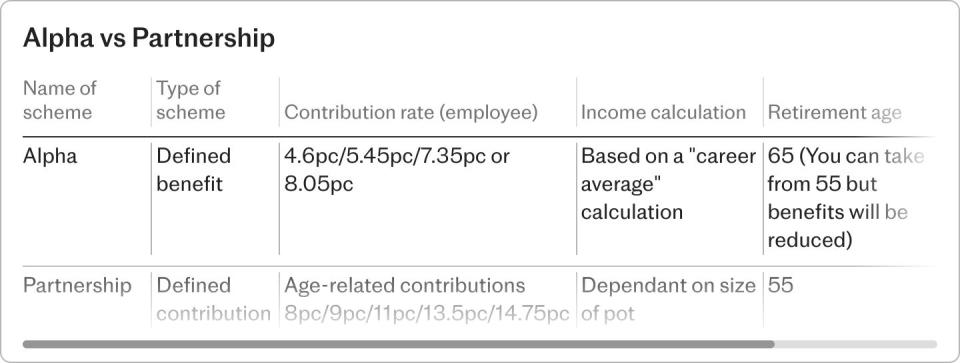

What is the civil service Alpha scheme?

The civil service Alpha pension scheme became the default scheme for individuals in April 2015. Most employees can join Alpha and all eligible new joiners will automatically be enrolled into the scheme.

It’s a defined benefit scheme which means it will pay a guaranteed amount. While most defined benefit schemes pay an income based on your final salary when you come to retire, and the number of years of service, Alpha is slightly different.

Income is calculated based on a “career average” calculation, which is the average of your salary over the course of your career.

You build up your pension by adding 2.32pc of your pensionable earnings each year.

You can start taking benefits from the Alpha scheme at 65. However, while you can take your pension before age 65, your benefits will be reduced to take account of early payment. The minimum pension age in Alpha is age 55.

What is the civil service Partnership scheme?

Since 2002, new joiners to the public sector have had the option of joining a scheme called Partnership, which is a defined contribution pension scheme.

This is different to a defined benefit scheme. Instead of a guaranteed payout, your pension contributions are invested in a mixture of stocks and bonds, which means the value of the pot fluctuates every day and there is a risk that a saver can run out of money in retirement without a guaranteed income.

You and your employer contribute a percentage of your pensionable earnings to the scheme to build up a pot to use in retirement.

Your employer will contribute a percentage of your pensionable earnings, which is tiered according to your age at the beginning of the tax year (as at the last April 6).

If you are under 31 you get 8pc, for 31 to 35-year-olds the contribution rate is 9pc, for 36 to 40-year-olds it’s 11pc and for 41-45-year-olds you get 13.5pc.

If you’re aged 46 or over the rate is 14.75pc.

These contributions are made even if you don’t save into your pension from your salary. But if you do, they will pay in further – up to 3pc of your pensionable earnings.

The contributions made by you and your employer will be invested in the partnership default fund: the Legal & General Pathway fund. There is the option, however, to choose your own investments from the range available.

You can start taking benefits from the Partnership scheme at 55 and you don’t have to retire to receive your pension.

How do they compare?

These schemes are different beasts entirely. Alpha is a defined benefit scheme which guarantees a specified income in retirement, and Partnership is a defined contribution pension and so your income in retirement is at the mercy of the stock market and its performance.

You might, however, choose to opt out of Alpha and join the Partnership pension scheme if you prefer to be in control of your pension fund and have more flexibility when it comes to retiring and when you can withdraw money.

Barry McKay of pension specialist Barnett Waddingham said: “For younger workers it’s almost a no-brainer to choose the safety and likely more generous payouts offered by a defined benefit scheme and select Alpha.

“But for someone older who has already built up a decent income in their defined benefit scheme, they may want to choose to start saving in the Partnership scheme which allows access at age 55 without reductions – rather than 65 with Alpha. That’s useful if you wanted to retire early and to plug the gap between retirement and age 65 when you start receiving the income from Alpha.

“While Partnership doesn’t offer the security of a defined benefit scheme, it still offers comparatively generous employer contribution rates.”

What will the civil service pension increase be in 2024?

There is a statutory requirement to increase the main public service pensions in operation each April in line with prices. The rules state that the increase is to be measured according to the annual increase in the Consumer Price Index (CPI) in the year to the preceding September (just like the increases to state pensions).

Civil service pensions increased by 6.7pc in April, which was tied to the inflation rate recorded in September 2023.

These adjustments to annual payouts ensures that the income from these pension schemes can keep pace with the rising cost of living.

There are a few exceptions where you might not see the total annual increase in your pension. For example, if you’ve retired partway through the year. If this is the case then your increase will be prorated, so you’ll get a portion of the annual increase based on how many months in that year you’ve been retired.

Is the civil service pension considered good?

Since most of the schemes are defined benefit pensions, the civil service pension is considered extremely generous.

Defined benefit – or final salary pensions – are considered the most generous kind of pension as they pay out an income in retirement which isn’t dependent on the performance of the stock market like most kinds of pension schemes.

Sometimes described as gold-plated, civil service pensions guarantee a specified income based on your final salary when you come to retire, and the number of years of service.

There are also benefits for your loved ones after you’ve gone, as when you die a proportion of your pension can be passed on. The terms of this benefit differs between the various schemes so it will depend on which one you’re a member of.

The Partnership scheme is not considered quite so generous, since it’s a defined contribution scheme, which means that what you receive in retirement is dependent on contributions and the growth of the pension fund.

Yet this is still considered as superior to workplace schemes in the private sector because employer contributions are much higher.

Richard Gibson of Barnett Waddingham, said: “In all the schemes offered to those in the public sector, the contribution rates are significantly higher than the bare minimum rates of the auto-enrolment scheme that exists for private sector employees.

“Crucially as a public sector worker you have the option to choose a gold-plated defined benefit scheme which is one of very few available these days.”