Yahoo Finance

Yahoo Finance For Clues About Palladium, Look to… North Macedonia?

(Bloomberg Opinion) -- “The Balkans” — according to remark often attributed to Winston Churchill — “produce more history than they can consume.” Precious-metal traders betting on the record surge in palladium prices might want to draw a similar lesson.

That’s because production and consumption of palladium and its sister-metal platinum in one tiny Balkan state are giving crucial clues to the way producers of automobile catalytic converters use the two elements. This in turn is likely to affect the path of prices for both metals.

As we’ve written, there are strong fundamental underpinnings to the extraordinary rally that’s seen palladium prices increase nearly fivefold in the past four years, at a time when platinum is up a mere 25%. Both metals have extensive industrial uses in the converters that strip carbon monoxide and nitrogen oxides from car exhausts. Supply and demand dynamics have conspired recently to push up palladium prices at the expense of platinum.

Sales of new diesel cars, which tend to use more platinum, have been hit by the aftermath of the diesel emissions-testing scandal, putting the preponderance of demand on palladium-heavy gasoline vehicles. At the same time, South Africa’s platinum-mining industry has been struggling with low profitability, which has helped to keep supply of its palladium byproduct back from the market. Meanwhile, vehicle-emissions standards have been tightening in Europe, China and other countries, increasing demand for catalysts to clear up exhaust fumes.

The normal solution to this sort of situation is substitution. Palladium had few uses until the rise of the catalytic converter in the 1970s pushed chemists to try it out as an alternative to platinum. At some point, the current price mismatch between the two metals should cause the pendulum to swing the other way, so that manufacturers reformulate their autocatalysts to use less palladium and more cheap platinum.

That’s the theory, at any rate. The question is whether substitution is actually happening.

Matthew Turner, a former precious metals analyst at Macquarie Group, has spotted one way for traders to keep an eye on that question. Johnson Matthey Plc, one of the world’s biggest producers of platinum-group metals, operates a major catalytic converter plant in Skopje, the capital of the Balkan republic of North Macedonia.

This offers a unique window into the generally secretive business of autocatalyst recipes. North Macedonia has no domestic supply of platinum-group metals, and local new-car sales amount to only a few thousand units a year. That’s handy, because the country breaks out the metals it’s importing in standard trade disclosures, giving investors a pretty good proxy for the proportions being used in Matthey’s emissions-control devices.

The figures won’t reassure palladium bears. If anything, matters are heading in the opposite direction. From a period a few years ago when the ratio between platinum and palladium imports was around 3:1, for much of the past year it’s tightened to around 1.8:1, implying a yet more palladium-dense catalyst mix. Trailing 12-month platinum imports in October, the last month for which data is available, were up just 3.9% from two years earlier; those of palladium were up 61%.

It would be wise to treat this information with a smidgen of caution. While catalysts are North Macedonia’s biggest export, the country still accounts for less than 10% of the global cross-border trade in such products — and that’s only a small part of the catalyst market as a whole, when you factor in domestic consumption.

The data also only tell you about the activity of one plant, which might not be representative of the industry as a whole. Importantly, the Skopje factory was set up to produce diesel catalysts, so gives us few clues as to what’s happening in the gasoline end of the autocatalyst market.

On top of that, Matthey is itself a major player in the platinum-group metals trade, and is no doubt wise to any efforts to use this data as a window on its commercial secrets. If it moves some excess palladium inventory to the Balkans, it’s not impossible that it could end up getting cheaper prices on its platinum from traders watching the North Macedonian trade figures — which could be useful, if you were planning to switch to a more platinum-dense catalyst mix.

Still, the resilience of North Macedonian palladium imports should give anyone expecting this bubble to deflate overnight reason to pause.

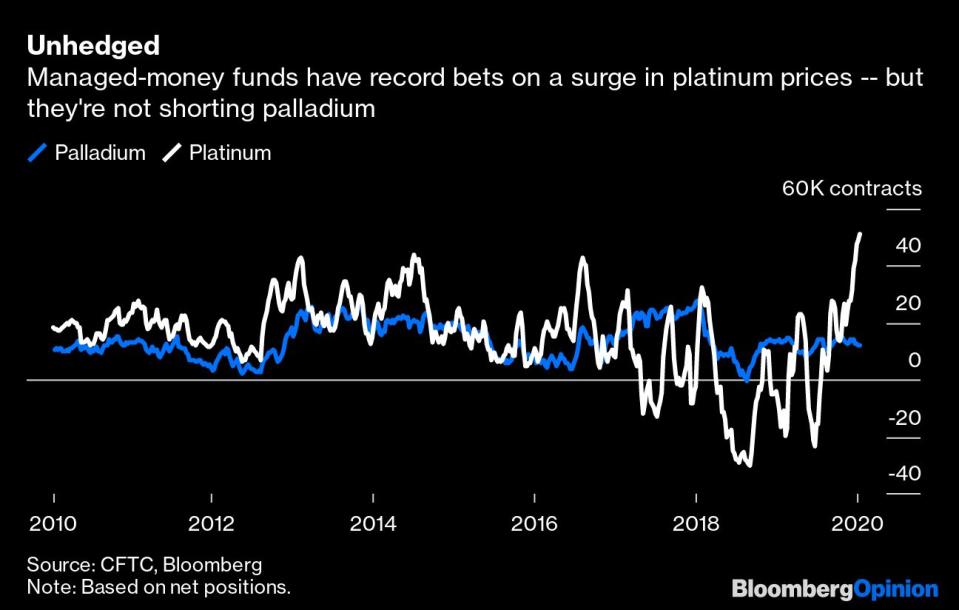

Most automobiles have just five grams or so of autocatalysts in them, meaning that even current prices have only driven your car’s platinum-group metal content up from around $150 to $300 — well below the $1,000 you’d spend to replace the converter itself. And for all the potential for a boost in platinum prices — the net long position held by hedge funds is now at a record high — there’s just no sign yet of a supply surge or a change in the chemistry mix that would be needed to end palladium’s boom.

Without that sort of catalyst, prices could be elevated for a while.

To contact the author of this story: David Fickling at dfickling@bloomberg.net

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

For more articles like this, please visit us at bloomberg.com/opinion

Subscribe now to stay ahead with the most trusted business news source.

©2020 Bloomberg L.P.