Yahoo Finance

Yahoo Finance This company proves that investors must look beyond past performance to pick winning shares

The past performance of investment trusts can be extremely misleading.

Take, for example, Lowland Investment Company. It has underperformed its benchmark, the FTSE All-Share index, over the past five years.

While the index’s total return is 17pc, the company has returned a hugely underwhelming -3pc. As a result, it is in the bottom quartile of its peer group within the Investment Trust UK Equity Income sector.

Based on its highly disappointing track record, many investors are likely to avoid the trust and look elsewhere.

However, upon more detailed inspection, the company’s lagging performance is largely down to its significant overweight exposure to UK-listed mid and small-cap stocks, in lieu of FTSE 100 shares, that have acted as a drag on its returns due to their enduring unpopularity among investors over recent years.

Indeed, at the time of its first-half results in March, just 47pc of the trust’s net assets were invested in FTSE 100 companies. This compares with 84pc for the FTSE All-Share Index. The remainder of its portfolio was focused on mid-caps, small-caps and AIM-quoted companies versus just 16pc for the benchmark.

Since the UK economy’s outlook has a greater impact on smaller companies than their larger peers, its relatively poor performance has weighed on their returns.

While Lowland’s continued focus on a multi-cap approach which differs materially from that of its benchmark may mean further underperformance over the short run, Questor views it as a positive long-term catalyst.

The UK’s near-pariah status in the investment world is extremely unlikely to persist.

With inflation set to fall rapidly, interest rate rises expected to abate (and even be replaced by interest rate cuts), and the economy’s outlook improving, investors will find it increasingly difficult to ignore the potential of mid and small-cap UK shares.

Indeed, the Bank of England expects inflation to drop to 3.4pc by the middle of next year as the inherent time lags of monetary policy changes finally pass.

The OECD, meanwhile, forecasts that the UK’s economic growth rate will accelerate to match that of the USA in 2024, with both countries set to produce 1pc GDP growth during the year.

Since mid and small-cap UK-listed shares offer wide margins of safety at present due to their grave unpopularity over recent years, there is vast potential for materially higher valuations as investor sentiment improves.

Therefore, investors who continue to back the trust’s contrarian stance, in terms of it investing a larger proportion of its net assets in smaller companies than its benchmark, are set to be handsomely rewarded.

Since the company is a holding within this column’s income portfolio, this bodes well for our future returns.

Of course, Lowland’s income, rather than capital growth, potential is the main reason for its inclusion. Although its shares have declined by 10pc since being added to the portfolio in April 2019, they have paid or declared around 19pc of their initial purchase price in dividends. This equates to a total return of around 9pc.

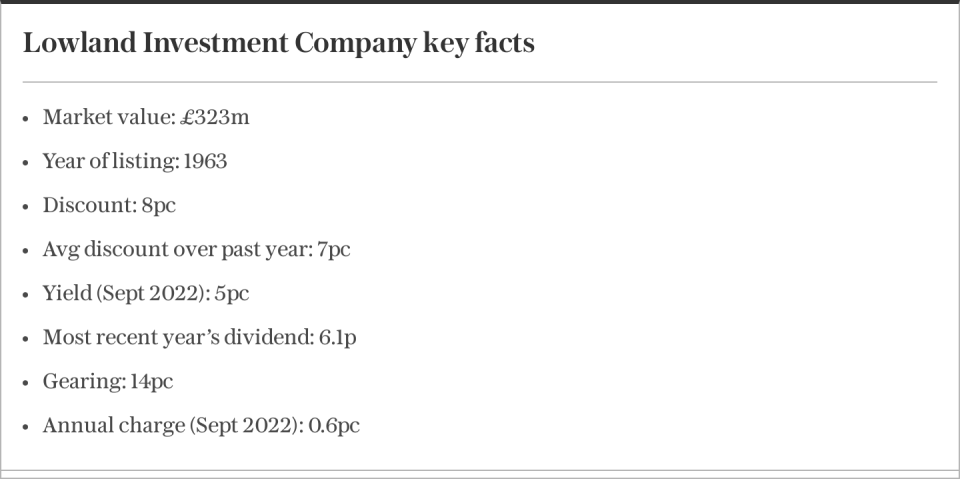

The company currently yields 5pc, which is 1.4 percentage points greater than the FTSE All-Share index’s yield, and has an excellent track record of dividend growth.

In fact, it has raised dividends per share at an annualised rate of 6.9pc over the past 25 years. This is more than twice the annual inflation rate (RPI) of 3.2pc over the same period. It has also either maintained or increased dividends in every year since its inception 60 years ago.

The trust currently trades at an 8pc discount to net asset value. This represents good value for money given its income appeal and the prospect of improving capital returns over the long run. It is, though, not particularly challenging to find UK-focused companies that trade at a larger discount to net asset value.

Where the trust has obvious relative appeal is in its gearing ratio, which stands at around 14pc. This will magnify returns in what this column expects to be a rising stock market, albeit with greater share price volatility along the way.

Therefore, while the trust has disappointed over recent years, Questor believes it is well positioned to capitalise on improving investor sentiment towards UK-listed mid and small-cap stocks.

Their dependence on the domestic economy means they are set to benefit from its improving outlook, while the trust’s attractive yield and large discount enhance its overall appeal.

The company technically remains a ‘hold’ given its place in our income portfolio, but would otherwise be classed as a ‘buy’.

Questor says: hold

Ticker: LWI

Share price at close: 121p

Read the latest Questor column on telegraph.co.uk every Sunday, Tuesday, Wednesday, Thursday and Friday from 6am.

Read Questor’s rules of investment before you follow our tips