Yahoo Finance

Yahoo Finance Is CPPGroup Plc's (LON:CPP) CEO Paid At A Competitive Rate?

In 2016 Jason Walsh was appointed CEO of CPPGroup Plc (LON:CPP). First, this article will compare CEO compensation with compensation at similar sized companies. Next, we'll consider growth that the business demonstrates. And finally - as a second measure of performance - we will look at the returns shareholders have received over the last few years. This method should give us information to assess how appropriately the company pays the CEO.

See our latest analysis for CPPGroup

How Does Jason Walsh's Compensation Compare With Similar Sized Companies?

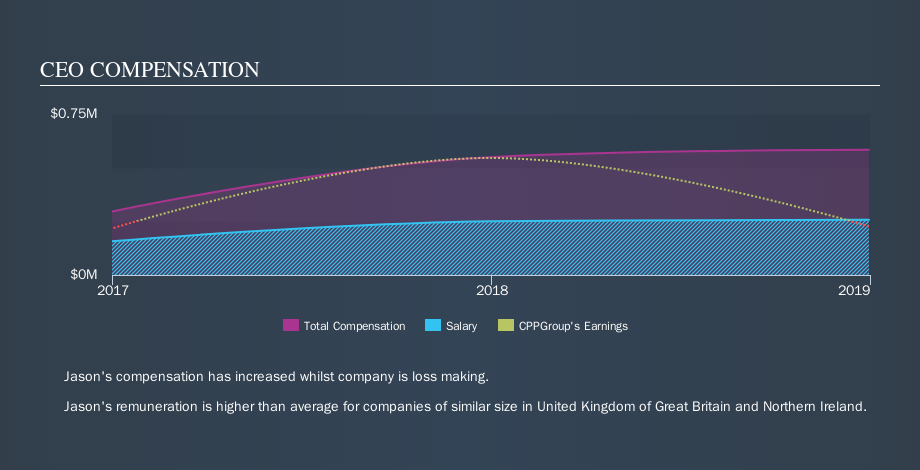

At the time of writing our data says that CPPGroup Plc has a market cap of UK£39m, and is paying total annual CEO compensation of UK£583k. (This number is for the twelve months until December 2018). While this analysis focuses on total compensation, it's worth noting the salary is lower, valued at UK£257k. We examined a group of similar sized companies, with market capitalizations of below UK£162m. The median CEO total compensation in that group is UK£256k.

It would therefore appear that CPPGroup Plc pays Jason Walsh more than the median CEO remuneration at companies of a similar size, in the same market. However, this fact alone doesn't mean the remuneration is too high. We can better assess whether the pay is overly generous by looking into the underlying business performance.

You can see, below, how CEO compensation at CPPGroup has changed over time.

Is CPPGroup Plc Growing?

On average over the last three years, CPPGroup Plc has shrunk earnings per share by 33% each year (measured with a line of best fit). In the last year, its revenue is up 16%.

Sadly for shareholders, earnings per share are actually down, over three years. There's no doubt that the silver lining is that revenue is up. But it isn't sufficiently fast growth to overlook the fact that earnings per share has gone backwards over three years. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. You might want to check this free visual report on analyst forecasts for future earnings.

Has CPPGroup Plc Been A Good Investment?

Given the total loss of 25% over three years, many shareholders in CPPGroup Plc are probably rather dissatisfied, to say the least. It therefore might be upsetting for shareholders if the CEO were paid generously.

In Summary...

We examined the amount CPPGroup Plc pays its CEO, and compared it to the amount paid by similar sized companies. We found that it pays well over the median amount paid in the benchmark group.

We think many shareholders would be underwhelmed with the business growth over the last three years.

Over the same period, investors would have come away with nothing in the way of share price gains. Some might well form the view that the CEO is paid too generously! Whatever your view on compensation, you might want to check if insiders are buying or selling CPPGroup shares (free trial).

Important note: CPPGroup may not be the best stock to buy. You might find something better in this list of interesting companies with high ROE and low debt.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.