Yahoo Finance

Yahoo Finance

CREDIT SUISSE: Don't worry, China is no Lehman Brothers in the making

Reuters

China's debt boom is back on. The question is whether it ends in a bang or a whimper.

The world's second largest economy added 2.34 trillion yuan ($362 billion) of new debt in March, far exceeding the median forecast of 1.4 trillion yuan ($220 billion) in a Bloomberg survey.

It prompted George Soros to say that the debt explosion in China "eerily resembles what happened during the financial crisis in the U.S. in 2007-08, which was similarly fueled by credit growth," according to Bloomberg.

"Most of the money that banks are supplying is needed to keep bad debts and loss-making enterprises alive," he said.

He added that the unsustainable situation can maintain itself for several years, just like in the US in 2005 and 2006, so the inevitable crash doesn't have to come immediately.

It's a view echoed by Credit Suisse's emerging markets debt analysts. Whenever there's a rapid build up of debt, sooner or later it comes to an end.

Here's Credit Suisse (emphasis ours)

Where opinion is divided is on how this will play out. At one end of the spectrum is acute financial crisis – a ‘Lehman moment’ reminiscent of the US in 2008, when banks failed and paralyzed credit markets. Other economists predict a chronic, Japan-style malaise in which growth slows for years or even decades.

At present, a period with a Japan-style malaise (and it is debatable how bad that really is) seems to us a more likely end-game for China (it has not quite ended in Japan just yet) than a ‘Lehman moment’ – because of the government’s (and the central bank’s) will and capacity to obviate the Lehman-scenario.

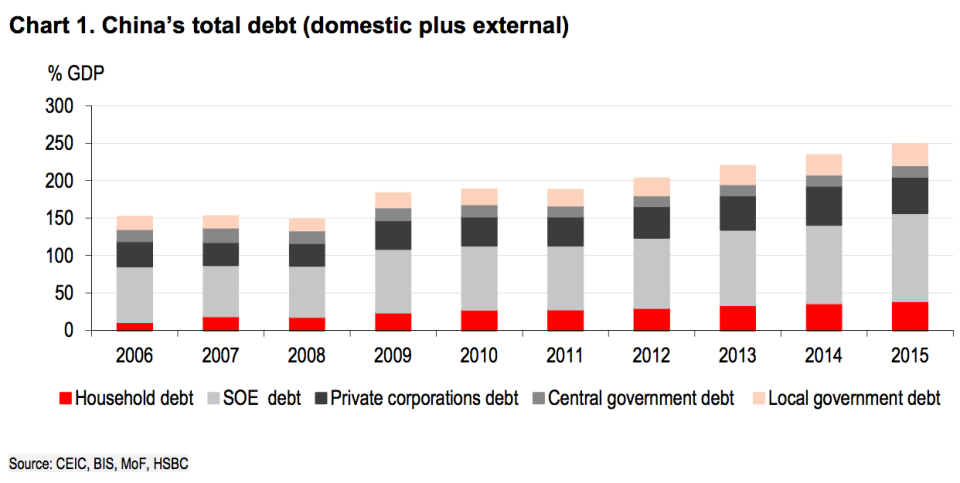

Here's how China reached a 249% debt-to-GDP ratio according to HSBC:

Reuters

Credit Suisse places its trust in China's policymakers to spot the problem and avoid a Lehman-style collapse:

Because of the interventionist inclinations of the Chinese policymakers, the end-game for the rapid buildup of leverage that has been underway in China since 2008 is more likely to be a Japan-style gradual (and multi-year) malaise in the domestic banking system than a “Lehman moment”

That said, a Japanese-style long-term economic malaise doesn't sound like a positive outcome either for China or the rest of the world.

NOW WATCH: How ISIS makes over $1 billion a year

See Also:

Goldman Sachs nails the staggering size of China's debt in 3 simple charts

China's rapidly ageing population is an economic ticking timebomb

SEE ALSO: George Soros: China's debt binge resembles that in the US before the recession