Yahoo Finance

Yahoo Finance If I’d invested £10k in Greggs shares two years ago here’s what I’d have today

Greggs (LSE: GRG) shares have smashed it since the pandemic. I don’t hold the high street bakery chain in my portfolio, but I wish I did. Now I’m wondering if it’s the right time to buy.

The Greggs share price has soared by 47.1% in the last two years. The stock would have turned a £10,000 investment into £14,710. With dividends, the total would be closer to £15,500.

Of course, with hindsight we might all be millionaires. Lately, Greggs shares have slowed. They’re up just 2.93% over the last 12 months. Over the same period, the FTSE 250 as a whole grew 5.72%.

Investors love Greggs, judging by the traffic on our site, but there’s an issue here. Maybe they love it a little too much.

FTSE 250 growth stock

There’s certainly a lot to like. 2023 saw “another year of rapid growth and strong progress”, in the words of CEO Roisin Currie. Total sales jumped 19.6% to £1.81bn, as Greggs expanded its network of stores beyond 3,000. It also sold more per store, with like-for-like sales up a tasty 13.7%. Pre-tax profits jumped 13% to £167.7m.

In October 2021, it announced ambitious plan to double sales within five years and it has made a strong start. If it disappoints, the backlash could be brutal, which brings me to that issue I mentioned.

The shares are a bit expensive. Trading at 22.34 times earnings they’re 70% higher than the FTSE 250 average of 13.1 times. Markets have priced a lot of growth in there. If it doesn’t come through, the share price could take a hit.

I’m pretty optimistic about Greggs’ prospects. It’s a high street fixture now. It survived pandemic lockdowns and has thrived during the cost-of-living crisis. As a purveyor of cheap treats, it might have benefited as shoppers traded down.

The shares could do even better when people have a bit more cash to spend. Although there’s a danger they could trade up to something pricier instead.

It also pays dividends

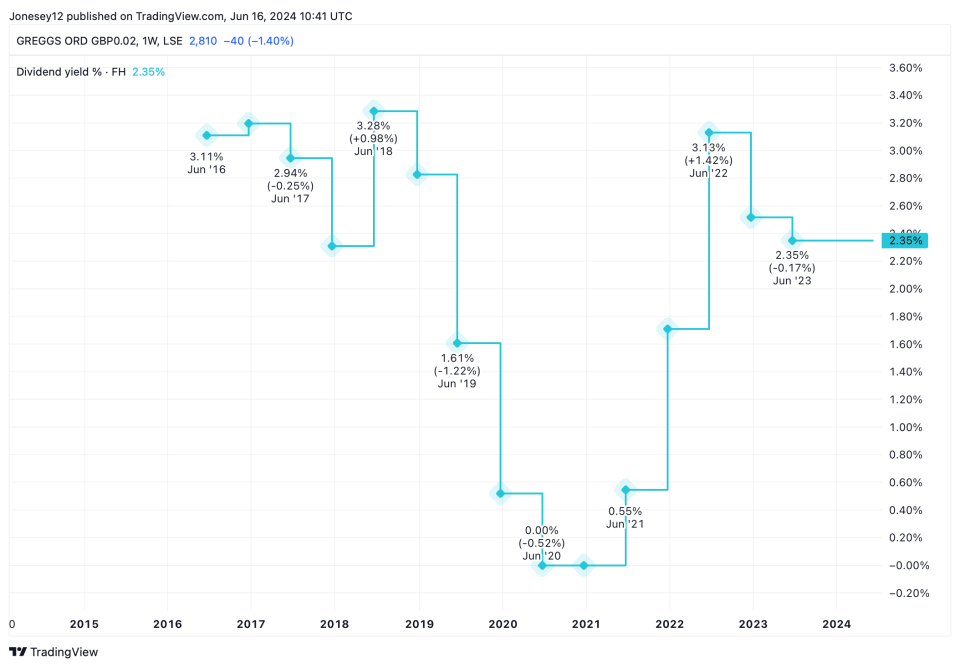

Greggs isn’t just about growth. It pays dividends too. While the yield is just 2.21% the board has worked hard to reward shareholders after being forced to drop shareholder payouts during the pandemic. Here’s what the charts say.

Chart by TradingView

The board increased the 2023 dividend by 5% from 59p to 62p per shares, and paid a special dividend of 40p on top. It could easily afford that, with net cash from operating activities after lease payments up 29% to £257m.

Yet I don’t think it’s the right time for me to buy Greggs today. That high valuation seems to suggest that its shares have gone as far as they can for now. They’ve been idling since full-year results were published in March. Investors may have got a little bit too carried away.

There’s also the underlying risk that all those messages about healthy eating and processed foods finally get through. Greggs’ ironic cult status may now be priced into its valuation. But what if shoppers decide the joke isn’t funny anymore? I wouldn’t want to be holding the shares if tastes change, and won’t buy it. I can find better value on the FTSE 250 today.

The post If I’d invested £10k in Greggs shares two years ago here’s what I’d have today appeared first on The Motley Fool UK.

More reading

Harvey Jones has no position in any of the shares mentioned. The Motley Fool UK has recommended Greggs Plc. Views expressed on the companies mentioned in this article are those of the writer and therefore may differ from the official recommendations we make in our subscription services such as Share Advisor, Hidden Winners and Pro. Here at The Motley Fool we believe that considering a diverse range of insights makes us better investors.

Motley Fool UK 2024