Yahoo Finance

Yahoo Finance Despite delivering investors losses of 54% over the past 3 years, Millicom International Cellular (NASDAQ:TIGO) has been growing its earnings

Millicom International Cellular S.A. (NASDAQ:TIGO) shareholders should be happy to see the share price up 22% in the last month. But that is small recompense for the exasperating returns over three years. Indeed, the share price is down a tragic 56% in the last three years. So it is really good to see an improvement. While many would remain nervous, there could be further gains if the business can put its best foot forward.

Although the past week has been more reassuring for shareholders, they're still in the red over the last three years, so let's see if the underlying business has been responsible for the decline.

View our latest analysis for Millicom International Cellular

There is no denying that markets are sometimes efficient, but prices do not always reflect underlying business performance. By comparing earnings per share (EPS) and share price changes over time, we can get a feel for how investor attitudes to a company have morphed over time.

Millicom International Cellular became profitable within the last five years. We would usually expect to see the share price rise as a result. So given the share price is down it's worth checking some other metrics too.

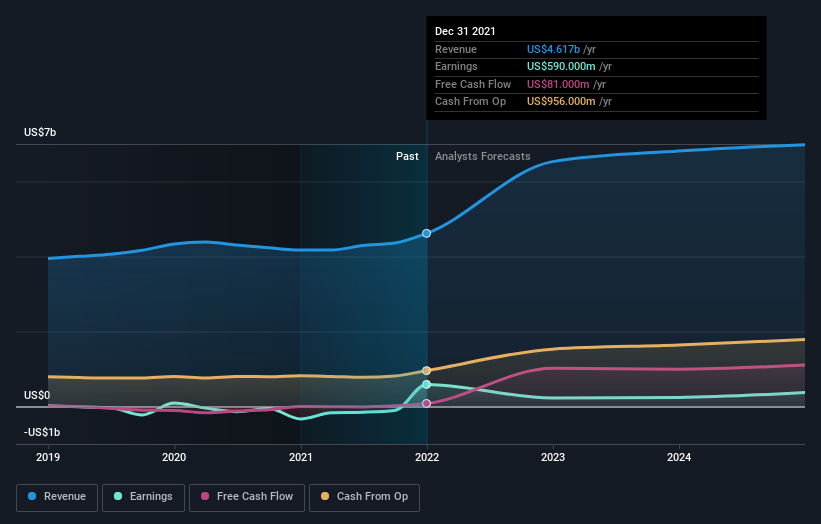

Revenue is actually up 3.2% over the three years, so the share price drop doesn't seem to hinge on revenue, either. This analysis is just perfunctory, but it might be worth researching Millicom International Cellular more closely, as sometimes stocks fall unfairly. This could present an opportunity.

The graphic below depicts how earnings and revenue have changed over time (unveil the exact values by clicking on the image).

It is of course excellent to see how Millicom International Cellular has grown profits over the years, but the future is more important for shareholders. You can see how its balance sheet has strengthened (or weakened) over time in this free interactive graphic.

What about the Total Shareholder Return (TSR)?

We've already covered Millicom International Cellular's share price action, but we should also mention its total shareholder return (TSR). The TSR attempts to capture the value of dividends (as if they were reinvested) as well as any spin-offs or discounted capital raisings offered to shareholders. Dividends have been really beneficial for Millicom International Cellular shareholders, and that cash payout explains why its total shareholder loss of 54%, over the last 3 years, isn't as bad as the share price return.

A Different Perspective

Investors in Millicom International Cellular had a tough year, with a total loss of 33%, against a market gain of about 2.5%. Even the share prices of good stocks drop sometimes, but we want to see improvements in the fundamental metrics of a business, before getting too interested. Regrettably, last year's performance caps off a bad run, with the shareholders facing a total loss of 7% per year over five years. Generally speaking long term share price weakness can be a bad sign, though contrarian investors might want to research the stock in hope of a turnaround. It's always interesting to track share price performance over the longer term. But to understand Millicom International Cellular better, we need to consider many other factors. Case in point: We've spotted 3 warning signs for Millicom International Cellular you should be aware of, and 2 of them can't be ignored.

If you are like me, then you will not want to miss this free list of growing companies that insiders are buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on US exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.