Yahoo Finance

Yahoo Finance Did Hays plc’s (LON:HAS) Recent Earnings Growth Beat The Trend?

Want to participate in a short research study? Help shape the future of investing tools and receive a $20 prize!

Assessing Hays plc’s (LON:HAS) past track record of performance is a useful exercise for investors. It allows us to understand whether the company has met or exceed expectations, which is a great indicator for future performance. Below, I assess HAS’s latest performance announced on 30 June 2018 and evaluate these figures to its historical trend and industry movements.

Check out our latest analysis for Hays

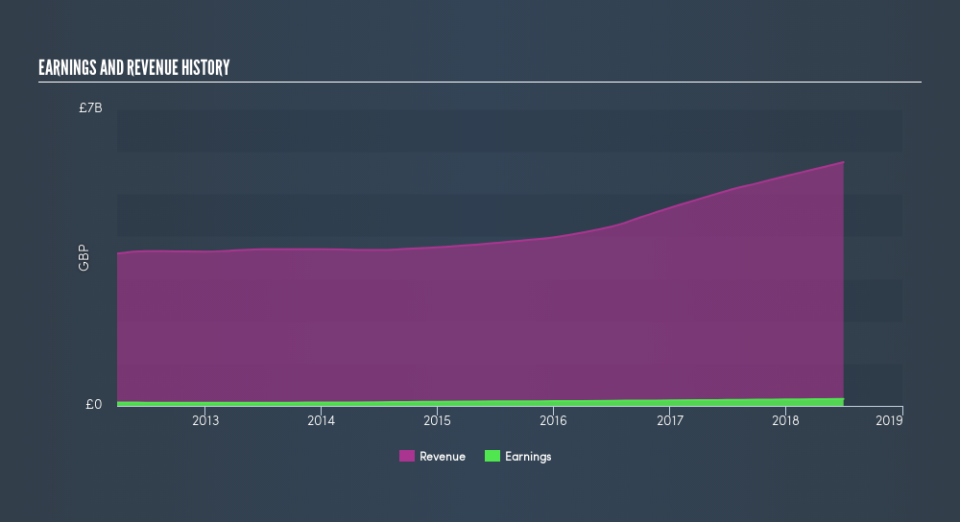

How Did HAS’s Recent Performance Stack Up Against Its Past?

HAS’s trailing twelve-month earnings (from 30 June 2018) of UK£166m has jumped 19% compared to the previous year.

Furthermore, this one-year growth rate has exceeded its 5-year annual growth average of 16%, indicating the rate at which HAS is growing has accelerated. How has it been able to do this? Well, let’s take a look at if it is merely a result of an industry uplift, or if Hays has seen some company-specific growth.

In terms of returns from investment, Hays has invested its equity funds well leading to a 24% return on equity (ROE), above the sensible minimum of 20%. Furthermore, its return on assets (ROA) of 11% exceeds the GB Professional Services industry of 9.5%, indicating Hays has used its assets more efficiently. However, its return on capital (ROC), which also accounts for Hays’s debt level, has declined over the past 3 years from 36% to 33%.

What does this mean?

Though Hays’s past data is helpful, it is only one aspect of my investment thesis. Positive growth and profitability are what investors like to see in a company’s track record, but how do we properly assess sustainability? I suggest you continue to research Hays to get a better picture of the stock by looking at:

Future Outlook: What are well-informed industry analysts predicting for HAS’s future growth? Take a look at our free research report of analyst consensus for HAS’s outlook.

Financial Health: Are HAS’s operations financially sustainable? Balance sheets can be hard to analyze, which is why we’ve done it for you. Check out our financial health checks here.

Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

NB: Figures in this article are calculated using data from the trailing twelve months from 30 June 2018. This may not be consistent with full year annual report figures.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.