Yahoo Finance

Yahoo Finance Does Enzo Biochem (NYSE:ENZ) Have A Healthy Balance Sheet?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Enzo Biochem, Inc. ( NYSE:ENZ ) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Enzo Biochem

What Is Enzo Biochem's Debt?

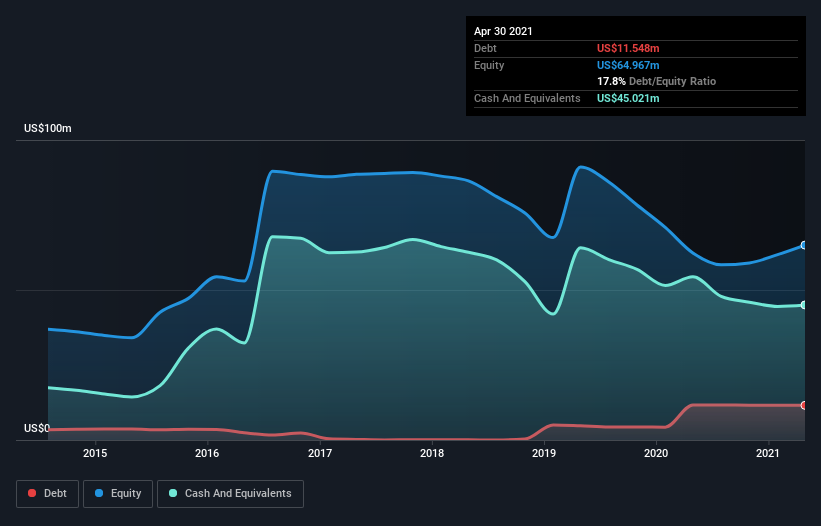

The chart below, which you can click on for greater detail, shows that Enzo Biochem had US$11.5m in debt in April 2021; about the same as the year before. But on the other hand it also has US$45.0m in cash, leading to a US$33.5m net cash position.

How Strong Is Enzo Biochem's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Enzo Biochem had liabilities of US$29.2m due within 12 months and liabilities of US$19.4m due beyond that. Offsetting this, it had US$45.0m in cash and US$11.5m in receivables that were due within 12 months. So it actually has US$7.84m more liquid assets than total liabilities. However, we were notified by a company representative on July 15, 2021, that $7 million of its outstanding bank loan was forgiven which brings down its total liabilities to US$22.2m and means it has almost US$15m more liquid assets than total liabilities.

This surplus suggests that Enzo Biochem has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Succinctly put, Enzo Biochem boasts net cash, so it's fair to say it does not have a heavy debt load! When analysing debt levels, the balance sheet is the obvious place to start. But it is Enzo Biochem's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot .

In the last year Enzo Biochem wasn't profitable at an EBIT level, but managed to grow its revenue by 45%, to US$112m. With any luck the company will be able to grow its way to profitability.

So How Risky Is Enzo Biochem?

Although Enzo Biochem had an earnings before interest and tax (EBIT) loss over the last twelve months, it made a statutory profit of US$1.3m. So taking that on face value, and considering the cash, we don't think its very risky in the near term. Keeping in mind its 45% revenue growth over the last year, we think there's a decent chance the company is on track. There's no doubt fast top line growth can cure all manner of ills, for a stock. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should be aware of the 2 warning signs we've spotted with Enzo Biochem .

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.