Yahoo Finance

Yahoo Finance Does Triple-S Management (NYSE:GTS) Have A Healthy Balance Sheet?

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Triple-S Management Corporation (NYSE:GTS) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Triple-S Management

What Is Triple-S Management's Net Debt?

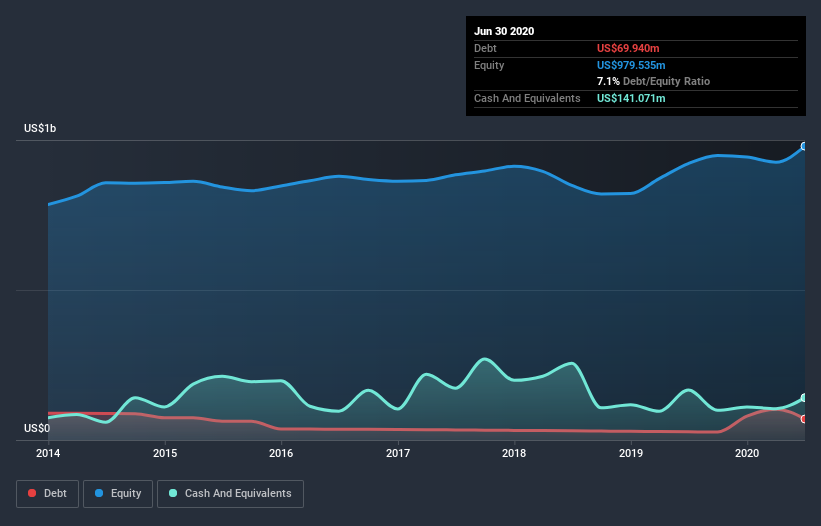

The image below, which you can click on for greater detail, shows that at June 2020 Triple-S Management had debt of US$69.9m, up from US$27.3m in one year. However, it does have US$141.1m in cash offsetting this, leading to net cash of US$71.1m.

How Strong Is Triple-S Management's Balance Sheet?

The latest balance sheet data shows that Triple-S Management had liabilities of US$1.53b due within a year, and liabilities of US$508.5m falling due after that. Offsetting this, it had US$141.1m in cash and US$301.3m in receivables that were due within 12 months. So it has liabilities totalling US$1.60b more than its cash and near-term receivables, combined.

The deficiency here weighs heavily on the US$428.4m company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we definitely think shareholders need to watch this one closely. After all, Triple-S Management would likely require a major re-capitalisation if it had to pay its creditors today. Triple-S Management boasts net cash, so it's fair to say it does not have a heavy debt load, even if it does have very significant liabilities, in total.

The good news is that Triple-S Management has increased its EBIT by 9.1% over twelve months, which should ease any concerns about debt repayment. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Triple-S Management will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. While Triple-S Management has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Happily for any shareholders, Triple-S Management actually produced more free cash flow than EBIT over the last three years. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Summing up

Although Triple-S Management's balance sheet isn't particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of US$71.1m. The cherry on top was that in converted 126% of that EBIT to free cash flow, bringing in US$71m. So we don't have any problem with Triple-S Management's use of debt. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For instance, we've identified 1 warning sign for Triple-S Management that you should be aware of.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.