Well, that's all from us today. Louis Ashworth will be back in the morning bright and early.

Thanks for following along!

What to look forward to tomorrow:

Interim results: Eddie Stobart

Full-year: Barratt Developments

Economics: BoE’s Bailey, Ramsden and Vlieghe at Treasury select committee (UK); ADP employment change, factory orders (US)

04:19 PM

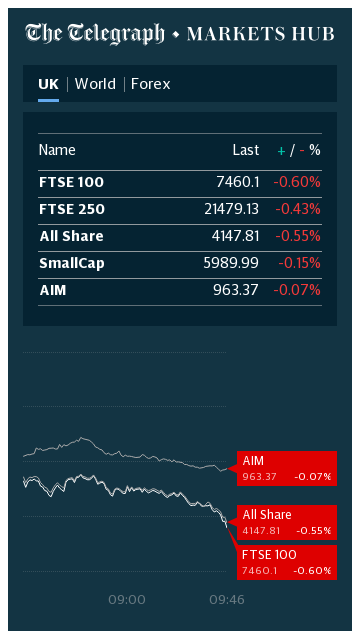

FTSE 100 skids to 3-month low

The FTSE 100 hit a three-month low today, closing 1.7pc lower, as the pound rallied against the dollar. Poor performance from banking and energy stocks also hurt the index.

Diageo, GlaxoSmithKline, AstraZeneca, Ashtead and Unilever all derive a large portion of their revenue from overseas, so the push higher in the pound usually hits the stocks. The declines in Royal Dutch Shell, BP, HSBC and Lloyds are weighing on the British benchmark too.

Mining stocks such as Fresnillo, Glencore, Anglo American and BHP Group are some of the best performers on the FTSE 100. The well-received manufacturing data from China overnight has lifted metal prices and in turn the mining companies.

Neil Wilson of Markets.com said: "A stronger pound undoubtedly took the wind out of the sails and a bit of a catchup trade was in play after the market was closed for the bank holiday on Monday, meaning it didn’t take part in the mild sell-off across Europe yesterday.

"But the FTSE’s troubles are not a new phenomenon. We’re trading today where it first ventured in March 1998 and Scotland still had a World Cup finals to look forward to. The dim and distant past in other words.

Since striking a post-Covid peak in early June, rather than kicking on in August, the FTSE 100 has rather majestically shrugged off the rally in global and US stocks and serenely plunged to its weakest since May. "

Morrisons to double number of florists after demand booms for blooms

Morrisons is doubling the number of florists in its stores after demand boomed for blooms as customers sought to cheer themselves up during lockdown, my colleague Simon Foy writes.

The Bradford-based grocer is to hire 180 qualified professional florists this autumn by installing 60 new flower stations across its stores, taking the total to more than 100.

The stalls will employ 300 people overall.

Flowers were a lockdown bestseller as families sought some cheer during the pandemic. Online searches for flowers have almost tripled in the past few months, according to Google data, and Morrisons is selling more than four million stems per week.

Ted Baker founder Ray Kelvin has appointed a nominee to the company's board to represent him, 18 months after the former boss resigned over misconduct allegations, which he denied.

PA has the details:

Colin La Fontaine Jackson will be a nominee director for Mr Kelvin, who still owns nearly 12pc of the business. It is part of a "relationship agreement" which lets the company tap into Mr Kelvin's expertise.

Ted Baker said it "brings the benefits of access to Ray's unique brand experience and insight, while at the same time introducing clear guidelines that will ensure board independence is maintained and that the interests of shareholders are prioritised and protected".

03:34 PM

US stocks push higher

Wall Street stocks have gained in the last hour ahead of key US manufacturing data after closing the books on a buoyant August.

The major US indices enjoyed their best August since the mid-1980s in the wake of extraordinary fiscal and monetary efforts from Washington to boost the economy after coronavirus shutdowns.

DOW 28474.96 +0.16%

SPX 3509.68 +0.27%

NDX 12227.5 +0.97%

RTY 1568.84 +0.45%

VIX 26.29 -0.45%

03:26 PM

German Parliament opens investigation into Wirecard scandal

The German parliament is set to hold an in-depth investigation into the collapse of Wirecard as questions mount over why the government failed to prevent massive corporate fraud at the payments firm.

The probe will increase pressure on German chancellor Angela Merkel and her deputy Olaf Scholz ahead of next year's Bundestag elections.

03:18 PM

Handover

With only a few minutes until the European close, it’s time for me to hand over to my colleague LaToya Harding, who will steer the blog into the evening. Thanks for following along today!

02:58 PM

Market moves

Not long left until the European close – and it looks certain to be a dismal one for the FTSE 100.

02:35 PM

US manufacturing expands at fastest pace since late 2018

Activity in America’s factories grew at the fastest pace since late 2018 as new orders soared, according to the Institute for Supply Management.

Its purchasing managers’ index rose to 56 from 54.2 in July, where a reading above 50 indicate growth. Its measure of orders jumped to the highest level since 2004.

Tax hikes risk trashing the economic recovery so the Chancellor should wait for several years before trying to plug the hole in the public finances, economists have told MPs.

“We are only six months into this crisis, we still don't know what is going to happen next in terms of Covid. Even if we don’t get second waves we are not very clear on where the economy is going to go, but we are pretty clear that it is going to be weak for some period,” he told the Treasury Select Committee.

The Nasdaq has opened as a fresh record high as tech stocks extended their march higher, led by Zoom.

Meanwhile the Dow Jones and the S&P 500 opened in negative territory.

US market data

12:53 PM

Wizz Air warns it may need to ‘park planes’ through winter

Wizz Air - REUTERS/Andrew Boyers/File Photo

Britain’s second-biggest airline has warned it may have to “park planes” to preserve cash as the Covid crisis wreaks havoc on the industry during the leaner winter months.

My colleague Oliver Gill reports:

Wizz Air also said if ongoing travel restrictions are continue over the next three months, it will continue to fly at 60pc capacity rather than the 80pc previously guided.

Despite the downgrade, the FTSE 250 airline, which specialises in low-cost flights to eastern and central Europe, repeated an assertion that it will be a “structural winner” from the Covid crisis.

Despite industry criticism, the Government has continued to reintroduce a quarantine on arrivals from countries that are experiencing an increase in infection rates.

Airline stocks rank among the hardest hit as a result of the pandemic. Wizz, however, has fared comparatively better than the likes of IAG, the owner of British Airways, and low-cost peer easyJet.

12:31 PM

Brazil suffers record quarterly contraction

Brazil’s economy shrank by 9.7pc during the second quarter, a record fall prompted by the devastating economic impact of Covid-19.

Activity dropped across the board as the virus paralysed public spending and slowed production activity.

President Jair Bolsonaro (who himself contracted the virus) has spent billions of dollars on stimulus efforts, which have included direct payouts and employment subsidies. Together, they have put the country in a stronger economic position than several of its neighbours, despite it having one of the world’s worst outbreaks.

12:02 PM

Consumer credit grows for first time since pandemic

A housing “mini-boom” and a surge in credit card spending as shoppers recovered their mojo for the first time since the pandemic struck fostered hopes of a V-shaped recovery on Tuesday.

My colleague Russell Lynch reports:

The Bank of England’s latest money and credit data for July - when bars and restaurants followed shops in reopening for the first time since the outbreak - showed households willing to borrow for the first time since February as the economy reawakens.

After four months of net repayments, households borrowed an extra £1.2bn over the month in personal loans and credit card debt - more than the average £1.1bn seen in the 18 months to February.

The Bank’s data also showed credit card borrowing of £622m during July, the highest rise in a single month since June 2018.

The AA has requested more time to continue talks with takeover suitors as the prospect of a bidding war stalled for the debt-laden breakdown firm.

My colleague Oliver Gill reports:u

A deadline for potential bidders to make an offer for the company has been extended by 28 days to Sept 29, the former FTSE 250 company announced on Tuesday.

Shares tumbled more than a tenth amid speculation that two of the three bidders have opened discussions about joining forces.

Warburg Pincus is holding preliminary discussions with a consorti

m led by Centerbridge Partners and Towerbrook Capital Partners, Sky News reported on Monday evening.

Meanwhile, speculation was growing that the third party, Platinum Equity, may not make a bid.

William Hill in talks over merger with US partner Caesars – Bloomberg

Bookmaker William Hill is shifting focus to concentrate on merging its US operations with partner Caesars Entertainment, Bloomberg reports.

The news service says:

Joe Asher, US chief executive officer for William Hill, confirmed the company is in discussions with Caesars about combining their sports-betting and online-gaming businesses. Caesars already owned 20pc of William Hill’s US arm under in a deal cut two years with Eldorado Resorts, which took over Caesars in July.

“There’s a lot of opportunity in there, and we think that we’ve got some really powerful assets in this space, so obviously it’s an ongoing subject of discussion,” Asher said in an interview.

Combined, the U.S. sports and online-gaming operations of the two could generate $700 million in revenue next year, Caesars said previously.

10:56 AM

Market moves

The FTSE 100 is continuing its downwards slide, currently off about 1.2pc. London’s blue-chips are sticking out like a sore thumb compared to European equities, which are all pushing slightly higher.

Plenty of pressure is coming from the pound, which has risen 0.65pc against the dollar today and is dragging on London’s international earners:

10:46 AM

FTSE reshuffle looms

Today marks the final session of movements before the latest reshuffle of London’s top indices. Movements will be announced tomorrow, based on today’s closing prices.

Last week, FTSE Russell (which provides the indices), announced the indicative moves based on prices as of 21st August.

It said ITV will likely lose its FTSE 100 spot, while B&M European Retail is likely to be promoted.

On the FTSE 250, it proposed the following additions (excluding ITV):

CMC Markets

Diversified Gas & Oil

Hipgnosis Songs Fund C *

Indivior

JPMorgan Euro Small Co. Trust

Premier Foods

Vectura Group

And the following deletions (ecluding B&M):

Bank of Georgia Group

Equiniti Group

Go-Ahead Group

Hammerson

PayPoint

PPHE Hotel Group

There should be a fairly clear sense of the state of play at the close today, but we’ll have to wait for tomorrow for confirmations.

Workers at hip replacement maker Smith & Nephew have been given vibrating bracelets to keep them away from colleagues in a bid to get back to the office.

My colleague Hasan Chowdhury reports:

Staff were issued with devices made by British robotics firm Tharsus to help them stay two metres apart and prevent the spread of coronavirus.

The Watford-headquartered firm held a three-week trial of Tharsus’s Bump system, which vibrates in what the manufacturer calls a “gentle, non-intimidating” way if two employees get too close.

Smith & Nephew has used the system in laboratories and warehouses, and on its manufacturing floor.

Tharsus claims it does not track workers’ movements. However, its products do collect data which allow companies to monitor behaviour and identify potential hotspots where social distancing could prove difficult.

Eight ways landlords can protect themselves from a recession: Until now most renters and buy-to-let owners have been cushioned from the worst of the crisis thanks to mortgage payment holidays and job support schemes – however a fallout is expected when both end in October.

09:22 AM

Mortgage approvals hit 66.3k in July

The UK’s mortgage market showed continued signs of a rebound in July, with approvals for home loans reaching 66,300 – about 10pc below pre-virus levels.

The Bank of England said:

On net, households borrowed an additional £2.7 billion secured on their homes. This was higher than the £2.4 billion in June but below the average of £4.2 billion in the six months to February 2020. The increase on the month reflected a slight increase in gross borrowing to £17.4 billion in July, below the pre-Covid February level of £23.7 billion and consistent with the recent weakness in mortgage approvals.

09:01 AM

Lloyd’s of London called to ditch fossil fuel insurance

Lloyd’s of London faces calls to protect the climate by axing insurance for fossil fuel projects to as it reopens its underwriting room today following the Covid pandemic.

My colleague Michael O’Dwyer reports:

Insurers at the 334-year-old market have provided cover to controversial projects including the proposed Adani Carmichael coal mine in Australia and the Trans Mountain tar sands pipeline in Canada. Financial services firms face growing pressure to cut ties with the fossil fuel industry by refusing to offer insurance and ending investments in projects and firms that are big polluters.

Zurich, which is not part of the Lloyd’s market, reportedly decided in July not to renew its cover for the Trans Mountain pipeline. The project is opposed by environmental campaigners and some indigenous groups.

At least 19 insurers had adopted policies restricting the cover they provide to the coal industry by May 2020, according to research from climate campaign group Insure our Future.

The UK’s finalised manufacturing PMI is in. It shows a minor overall slip compared to the preliminary reading, coming in at 55.2 (the ‘flash’ figure was 55.3).

That’s the highest since 2018, while the output sub-gauge rose to its highest level since April 2014.

IHS Markit, which gathered the data, said:

Manufacturing production rose at the fastest pace since May 2014, reflecting solid expansions across the consumer, intermediate and investment goods sub-sectors. The steepest growth was registered in the intermediate goods category, whereas investment goods producers saw the lowest pace of growth.

It found:

Underpinning the scaling-up of output was the fastest increase in new orders since November 2017

Manufacturing employment declined at one of the steepest rates during the past 11 years

Input price inflation accelerated to a 20-month high

Business sentiment regarding future output prospects remained positive

IHS Markit’s Rob Dobson said:

The recovery of the UK manufacturing sector gathered pace in August…

However, companies report that the current bounce is mainly driven by the restarting of manufacturers’ operations and reopening of clients as COVID-19 restrictions continue to be relaxed. Backlogs of work fell at an increased rate, hinting at spare capacity, and the labour market remains worryingly weak, with job losses registered for the seventh straight month. The downturn in employment may have further to run as the government’s furlough scheme is phased out unless demand rises sharply.

08:22 AM

City of London launches consultation on statue removals

Robert Milligan - REUTERS/John Sibley/File Photo

The City of London Corporation has launched a consultation, seeking view on whether it should take down statues and landmarks with links to racism and slavery.

The memorials could be re-sited, reinterpreted or retained depending on the responses collected, Andrien Meyers, co-chair of the City’s Tackling Racism Taskforce, said. Street and building names could also be changed.

“We know that historical symbols continue to have an impact today and we want to understand how people feel about this aspect of our cultural history,” Meyers said.

Statues and memorials with links to slavery and racism have been targeted globally, with some toppled by protesters and others removed by civic authorities or property owners.

It adds:

One City statue targeted for removal by a petition in June is a huge monument to William Beckford, twice Lord Mayor of London in the 1760s and the largest slave owner of his time.

His statue stands in the Guildhall, the ornate seat of the City of London Corporation. The government rejected the petition on the grounds it was a matter for the local authority.

08:12 AM

Eurozone manufacturing growth holds steady

The overall final manufacturing PMI for the eurozone stood at 51.7 – meaning growth continued, albeit at a slightly slower pace of acceleration than during July.

IHS Markit, which gathered the data, said:

Growth was again widespread, with all three market groups registering an improvement in operating conditions compared to the previous month. The consumer goods category was again the bestperforming, retaining a solid pace of expansion. Relatively modest gains were seen in the intermediate and investment goods categories.

It found:

Country level data indicated some divergent trends in manufacturing performance

Continued gains in new business led to a slight increase in backlogs of work

Latest data showed that job numbers were cut for a sixteenth successive month, albeit at the slowest rate since March

Competitive pressures led to a fourteenth successive monthly fall in output charges

Confidence about the future continued to pick up

Chris Williamson, IHS Markit’s chief business economist, said:

Caution is warranted in assessing the likely production trend, however, as so far it would have been surprising to have seen anything other than a rebound in output and sentiment. Worryingly, order book growth cooled slightly in August, and there are indications that firms are bracing for a near-term weakening of demand…

In short, manufacturing is currently being buoyed by a wave of pent up demand, but capacity is being scaled back. The next few months’ data will be allimportant in assessing the sustainability of the upturn.

07:57 AM

Mixed picture for Europe’s manufacturing

Finalised manufacturing purchasing manager’s index readings for the eurozone have offered a bit of a mixed picture this morning: as flash figures indicated, France’s factory rebound appears to have stalled, while Spain is in a similar spot – with both falling below the growth threshold of 50.

Meanwhile, Germany and Italy were still recording healthy growth,

Here are the figures:

Spain: 49.9

Italy: 53.1

France: 49.8

Germany: 52.2

07:32 AM

Apple now bigger than entire FTSE 100

With London stocks dropping at the open today, it’s official: Apple is now bigger than the entire FTSE 100.

The tech giant is valued at £1.647 trillion, compared to the roughly £1.625 trillion combined valuation of the blue-chips.

Apple has passed the milestone following its 4-for-1 stock split, which took place on Friday – splitting all its shares into four, meaning they are ““more accessible to a broader base of investors”. The split sent the iPhone maker’s price higher.

The FTSE 100 has dropped at the open, despite rises for its European peers. That reflects London’s blue-chips playing slightly catch-up with yesterday’s losses on the continent, as well as the impact of a rising pound.

Bloomberg TV - Bloomberg TV

06:54 AM

Saga confirms equity raise

Over-50s holiday operator Saga has sent out a regulatory filing confirming the equity raise plans it announced at the weekend.

As we reported on Sunday, the group’s former boss is planning to pump as much as £100m into the business and mount a dramatic return to its board:

Sir Roger De Haan will stump up the lion’s share of a £150m equity raise by Saga, with other investors asked to supply the rest as part of efforts to restore its fortunes.

The son of Saga’s founder Sidney De Haan, Sir Roger sold it to private equity group Charterhouse for £1.35bn in 2004 after 20 years at its helm.

He will take a 20pc stake and replace Patrick O’Sullivan as its non-executive chairman under proposals which the business said are well advanced.

Saga said that the 71-year-old will serve for an expected term of three years. Euan Sutherland will remain in place as chief executive.

Dunelm performance ‘materially ahead’ of expectations

Dunelm

Furniture and homewares retailer Dunelm said sales had been “strong” over the past two months, leaving its year-to-date performance “materially ahead” of its initial expectations.

Year-on-year sales growth during July was at 59pc, which the FTSE 250 group attributed to pent up demand and the timing of its summer sale. Sales were up 24pc in August.

The group said:

This performance reflects the strength of our proposition within a resilient homewares market, positive footfall growth to our mainly out-of-town superstores and continued strong growth in our home delivery offer.

It added that it remains “very difficult to provide any meaningful guidance on the future outlook”, given current uncertainty about by the economy, and the risk of further lockdowns.

06:21 AM

Agenda: Dollar hits two-year low

Good morning. The dollar has hit a two-year low as investors digest new Federal Reserve comments that suggested rates will stay low for an extended period.

The dollar edged lower against a basket of major currencies early on Tuesday. The dollar index fell 0.08pc, with the pound rising to $1.341 and the euro up 0.02pc to $1.194.

The Dow Jones and S&P 500 fell on Monday, with the latter climbing down from Friday’s record high as the prospect of Chinese intervention in TikTok’s sale hit shares in prospective bidders Microsoft and Walmart.

The Nasdaq hit a record, with shares in Apple and Tesla rising after their stock splits and Zoom's shares soaring after bumper results.

Major Asian share indexes edged lower on Tuesday in mostly muted trading after a retreat overnight on Wall Street.

Australia's benchmark led the decline, falling more than 2pc Tuesday ahead of a Reserve Bank of Australia decision that is expected to keep interest rates unchanged.

Newly released manufacturing data from Japan showed factory activity slightly improved, though still in contraction.

The Japanese government reported that the seasonally adjusted unemployment rate for July stood at 2.9pc, little changed from recent months.

Tokyo’s Nikkei 225 index lost 0.1pc to 23,107.90 and the Hang Seng in Hong Kong also fell 0.1pc, to 25,171.86. South Korea’s Kospi gained 1pc to 2,349.32. The Shanghai Composite index was virtually flat, at 3,397.14.

The S&P/ASX 200 dropped 2.1pc to 5,931.30 ahead of the RBA's policy announcement.

Coming up today

Manufacturing PMIs for many major economies including the UK and US are out today, while mortgage approvals and lending numbers for the UK will give an idea of the strength of the housing market.

Yahoo Finance

Yahoo Finance