Yahoo Finance

Yahoo Finance Earnings growth of 53% over 1 year hasn't been enough to translate into positive returns for Altice USA (NYSE:ATUS) shareholders

It's not a secret that every investor will make bad investments, from time to time. But it would be foolish to simply accept every extremely large loss as an inevitable part of the game. So spare a thought for the long term shareholders of Altice USA, Inc. (NYSE:ATUS); the share price is down a whopping 71% in the last twelve months. That'd be enough to make even the strongest stomachs churn. We note that it has not been easy for shareholders over three years, either; the share price is down 56% in that time.

Since Altice USA has shed US$323m from its value in the past 7 days, let's see if the longer term decline has been driven by the business' economics.

See our latest analysis for Altice USA

There is no denying that markets are sometimes efficient, but prices do not always reflect underlying business performance. One flawed but reasonable way to assess how sentiment around a company has changed is to compare the earnings per share (EPS) with the share price.

During the unfortunate twelve months during which the Altice USA share price fell, it actually saw its earnings per share (EPS) improve by 53%. It's quite possible that growth expectations may have been unreasonable in the past.

It's surprising to see the share price fall so much, despite the improved EPS. So it's easy to justify a look at some other metrics.

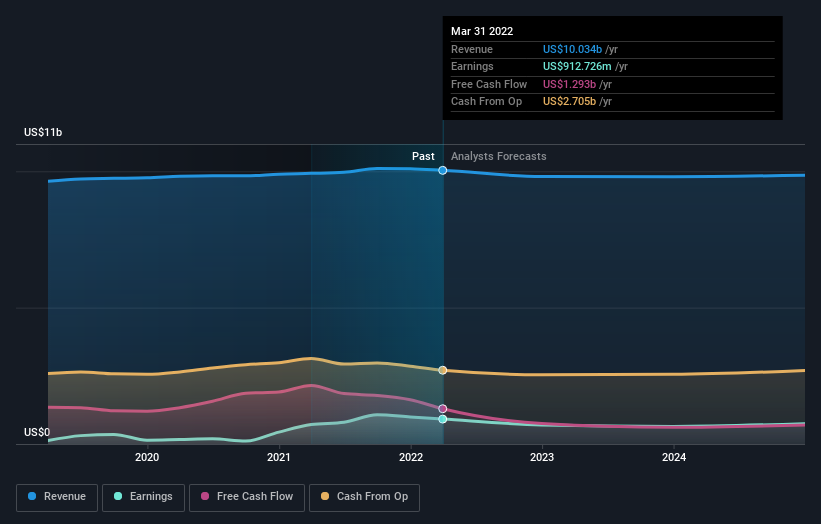

Revenue was pretty flat on last year, which isn't too bad. But the share price might be lower because the market expected a meaningful improvement, and got none.

The company's revenue and earnings (over time) are depicted in the image below (click to see the exact numbers).

We consider it positive that insiders have made significant purchases in the last year. Even so, future earnings will be far more important to whether current shareholders make money. If you are thinking of buying or selling Altice USA stock, you should check out this free report showing analyst profit forecasts.

A Different Perspective

The last twelve months weren't great for Altice USA shares, which performed worse than the market, costing holders 71%. The market shed around 14%, no doubt weighing on the stock price. The three-year loss of 16% per year isn't as bad as the last twelve months, suggesting that the company has not been able to convince the market it has solved its problems. Although Baron Rothschild famously said to "buy when there's blood in the streets, even if the blood is your own", he also focusses on high quality stocks with solid prospects. While it is well worth considering the different impacts that market conditions can have on the share price, there are other factors that are even more important. Consider risks, for instance. Every company has them, and we've spotted 2 warning signs for Altice USA you should know about.

Altice USA is not the only stock insiders are buying. So take a peek at this free list of growing companies with insider buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on US exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.