Yahoo Finance

Yahoo Finance Earnings growth of 6.2% over 3 years hasn't been enough to translate into positive returns for Canadian Solar (NASDAQ:CSIQ) shareholders

The truth is that if you invest for long enough, you're going to end up with some losing stocks. But long term Canadian Solar Inc. (NASDAQ:CSIQ) shareholders have had a particularly rough ride in the last three year. So they might be feeling emotional about the 69% share price collapse, in that time. And over the last year the share price fell 64%, so we doubt many shareholders are delighted. The falls have accelerated recently, with the share price down 40% in the last three months.

Since Canadian Solar has shed US$83m from its value in the past 7 days, let's see if the longer term decline has been driven by the business' economics.

Check out our latest analysis for Canadian Solar

To paraphrase Benjamin Graham: Over the short term the market is a voting machine, but over the long term it's a weighing machine. One imperfect but simple way to consider how the market perception of a company has shifted is to compare the change in the earnings per share (EPS) with the share price movement.

During the unfortunate three years of share price decline, Canadian Solar actually saw its earnings per share (EPS) improve by 20% per year. Given the share price reaction, one might suspect that EPS is not a good guide to the business performance during the period (perhaps due to a one-off loss or gain). Alternatively, growth expectations may have been unreasonable in the past.

Since the change in EPS doesn't seem to correlate with the change in share price, it's worth taking a look at other metrics.

Revenue is actually up 27% over the three years, so the share price drop doesn't seem to hinge on revenue, either. This analysis is just perfunctory, but it might be worth researching Canadian Solar more closely, as sometimes stocks fall unfairly. This could present an opportunity.

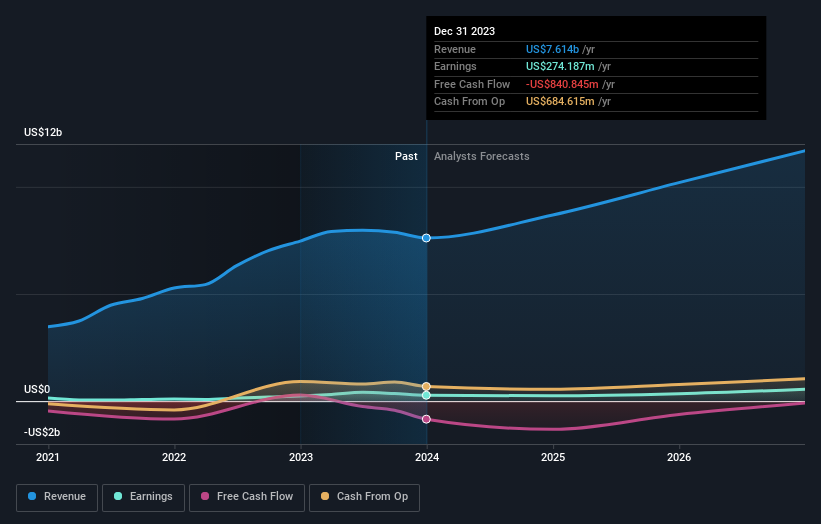

The graphic below depicts how earnings and revenue have changed over time (unveil the exact values by clicking on the image).

We know that Canadian Solar has improved its bottom line lately, but what does the future have in store? So it makes a lot of sense to check out what analysts think Canadian Solar will earn in the future (free profit forecasts).

A Different Perspective

Canadian Solar shareholders are down 64% for the year, but the market itself is up 21%. Even the share prices of good stocks drop sometimes, but we want to see improvements in the fundamental metrics of a business, before getting too interested. Unfortunately, last year's performance may indicate unresolved challenges, given that it was worse than the annualised loss of 5% over the last half decade. Generally speaking long term share price weakness can be a bad sign, though contrarian investors might want to research the stock in hope of a turnaround. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. Consider for instance, the ever-present spectre of investment risk. We've identified 2 warning signs with Canadian Solar , and understanding them should be part of your investment process.

But note: Canadian Solar may not be the best stock to buy. So take a peek at this free list of interesting companies with past earnings growth (and further growth forecast).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.