Yahoo Finance

Yahoo Finance Earnings Miss: Momentum Group AB (publ) Missed EPS By 12% And Analysts Are Revising Their Forecasts

Investors in Momentum Group AB (publ) (STO:MMGR B) had a good week, as its shares rose 2.4% to close at kr88.90 following the release of its annual results. Revenues were in line with forecasts, at kr6.1b, although statutory earnings per share came in 12% below what the analyst expected, at kr7.70 per share. Following the result, the analyst has updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. We thought readers would find it interesting to see the analyst latest (statutory) post-earnings forecasts for next year.

See our latest analysis for Momentum Group

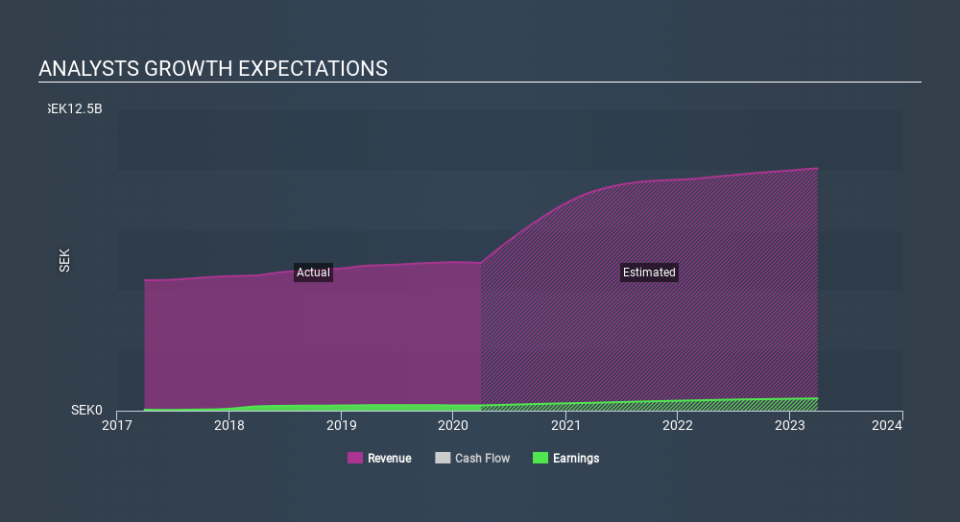

Following the latest results, Momentum Group's lone analyst are now forecasting revenues of kr9.10b in 2021. This would be a sizeable 48% improvement in sales compared to the last 12 months. Statutory earnings per share are forecast to fall 15% to kr6.53 in the same period. Yet prior to the latest earnings, the analyst had been anticipated revenues of kr9.13b and earnings per share (EPS) of kr6.83 in 2021. So it looks like there's been a small decline in overall sentiment after the recent results - there's been no major change to revenue estimates, but the analyst did make a small dip in their earnings per share forecasts.

Despite cutting their earnings forecasts,the analyst has lifted their price target 9.5% to kr115, suggesting that these impacts are not expected to weigh on the stock's value in the long term.

Of course, another way to look at these forecasts is to place them into context against the industry itself. It's clear from the latest estimates that Momentum Group's rate of growth is expected to accelerate meaningfully, with the forecast 48% revenue growth noticeably faster than its historical growth of 3.8%p.a. over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 4.3% per year. Factoring in the forecast acceleration in revenue, it's pretty clear that Momentum Group is expected to grow much faster than its industry.

The Bottom Line

The most important thing to take away is that the analyst downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. Fortunately, they also reconfirmed their revenue numbers, suggesting sales are tracking in line with expectations - and our data suggests that revenues are expected to grow faster than the wider industry. We note an upgrade to the price target, suggesting that the analyst believes the intrinsic value of the business is likely to improve over time.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. At least one analyst has provided forecasts out to 2023, which can be seen for free on our platform here.

Don't forget that there may still be risks. For instance, we've identified 3 warning signs for Momentum Group (1 is concerning) you should be aware of.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.