Yahoo Finance

Yahoo Finance Egdon Resources plc (LON:EDR) On The Verge Of Breaking Even

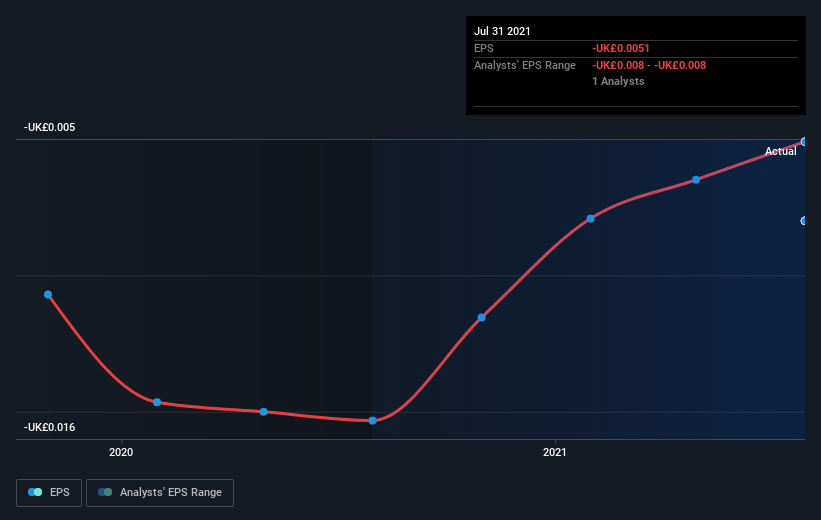

With the business potentially at an important milestone, we thought we'd take a closer look at Egdon Resources plc's (LON:EDR) future prospects. Egdon Resources plc, together with its subsidiaries, engages in the exploration and production of hydrocarbons in the United Kingdom. On 31 July 2021, the UK£8.3m market-cap company posted a loss of UK£1.7m for its most recent financial year. Many investors are wondering about the rate at which Egdon Resources will turn a profit, with the big question being “when will the company breakeven?” We've put together a brief outline of industry analyst expectations for the company, its year of breakeven and its implied growth rate.

View our latest analysis for Egdon Resources

Consensus from 2 of the British Oil and Gas analysts is that Egdon Resources is on the verge of breakeven. They anticipate the company to incur a final loss in 2021, before generating positive profits of UK£1.0m in 2022. The company is therefore projected to breakeven around 12 months from now or less. How fast will the company have to grow to reach the consensus forecasts that anticipate breakeven by 2022? Working backwards from analyst estimates, it turns out that they expect the company to grow 94% year-on-year, on average, which signals high confidence from analysts. Should the business grow at a slower rate, it will become profitable at a later date than expected.

We're not going to go through company-specific developments for Egdon Resources given that this is a high-level summary, but, take into account that by and large energy companies, depending on the stage of operation and resource produced, have irregular periods of cash flow. So, a high growth rate is not out of the ordinary, particularly when a company is in a period of investment.

Before we wrap up, there’s one aspect worth mentioning. Egdon Resources currently has no debt on its balance sheet, which is quite unusual for a cash-burning oil and gas company, which typically has high debt relative to its equity. This means that the company has been operating purely on its equity investment and has no debt burden. This aspect reduces the risk around investing in the loss-making company.

Next Steps:

There are too many aspects of Egdon Resources to cover in one brief article, but the key fundamentals for the company can all be found in one place – Egdon Resources' company page on Simply Wall St. We've also compiled a list of key factors you should further examine:

Historical Track Record: What has Egdon Resources' performance been like over the past? Go into more detail in the past track record analysis and take a look at the free visual representations of our analysis for more clarity.

Management Team: An experienced management team on the helm increases our confidence in the business – take a look at who sits on Egdon Resources' board and the CEO’s background.

Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.