Yahoo Finance

Yahoo Finance Emmi's (VTX:EMMN) Upcoming Dividend Will Be Larger Than Last Year's

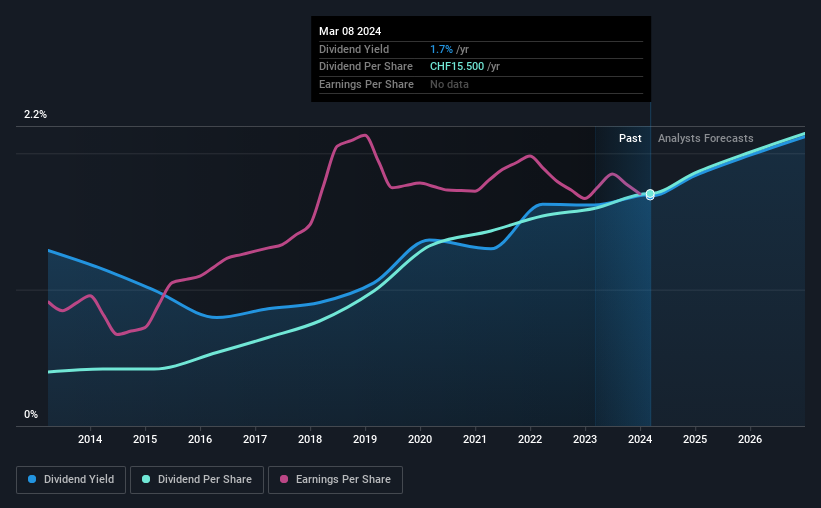

Emmi AG's (VTX:EMMN) dividend will be increasing from last year's payment of the same period to CHF15.50 on 17th of April. This takes the annual payment to 1.7% of the current stock price, which unfortunately is below what the industry is paying.

Check out our latest analysis for Emmi

Emmi's Earnings Easily Cover The Distributions

Even a low dividend yield can be attractive if it is sustained for years on end. The last dividend was quite easily covered by Emmi's earnings. This means that a large portion of its earnings are being retained to grow the business.

Looking forward, earnings per share is forecast to rise by 37.8% over the next year. Assuming the dividend continues along recent trends, we think the payout ratio could be 37% by next year, which is in a pretty sustainable range.

Emmi Has A Solid Track Record

The company has a sustained record of paying dividends with very little fluctuation. Since 2014, the annual payment back then was CHF3.60, compared to the most recent full-year payment of CHF15.50. This means that it has been growing its distributions at 16% per annum over that time. We can see that payments have shown some very nice upward momentum without faltering, which provides some reassurance that future payments will also be reliable.

Emmi May Find It Hard To Grow The Dividend

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. Let's not jump to conclusions as things might not be as good as they appear on the surface. It's not great to see that Emmi's earnings per share has fallen at approximately 4.4% per year over the past five years. Declining earnings will inevitably lead to the company paying a lower dividend in line with lower profits. Earnings are forecast to grow over the next 12 months and if that happens we could still be a little bit cautious until it becomes a pattern.

In Summary

Overall, it's great to see the dividend being raised and that it is still in a sustainable range. The earnings coverage is acceptable for now, but with earnings on the decline we would definitely keep an eye on the payout ratio. The payment isn't stellar, but it could make a decent addition to a dividend portfolio.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Without at least some growth in earnings per share over time, the dividend will eventually come under pressure either from competition or inflation. Businesses can change though, and we think it would make sense to see what analysts are forecasting for the company. Is Emmi not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.