Yahoo Finance

Yahoo Finance If EPS Growth Is Important To You, Bell Equipment (JSE:BEL) Presents An Opportunity

It's common for many investors, especially those who are inexperienced, to buy shares in companies with a good story even if these companies are loss-making. Sometimes these stories can cloud the minds of investors, leading them to invest with their emotions rather than on the merit of good company fundamentals. Loss-making companies are always racing against time to reach financial sustainability, so investors in these companies may be taking on more risk than they should.

Despite being in the age of tech-stock blue-sky investing, many investors still adopt a more traditional strategy; buying shares in profitable companies like Bell Equipment (JSE:BEL). Even if this company is fairly valued by the market, investors would agree that generating consistent profits will continue to provide Bell Equipment with the means to add long-term value to shareholders.

View our latest analysis for Bell Equipment

Bell Equipment's Improving Profits

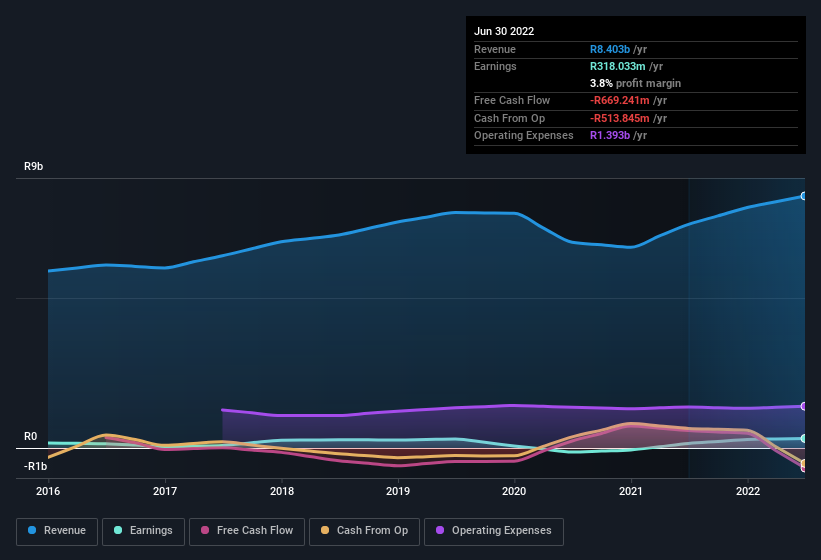

Even with very modest growth rates, a company will usually do well if it improves earnings per share (EPS) year after year. So EPS growth can certainly encourage an investor to take note of a stock. Outstandingly, Bell Equipment's EPS shot from R1.57 to R3.33, over the last year. Year on year growth of 111% is certainly a sight to behold.

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. Bell Equipment maintained stable EBIT margins over the last year, all while growing revenue 13% to R8.4b. That's encouraging news for the company!

In the chart below, you can see how the company has grown earnings and revenue, over time. Click on the chart to see the exact numbers.

Bell Equipment isn't a huge company, given its market capitalisation of R1.4b. That makes it extra important to check on its balance sheet strength.

Are Bell Equipment Insiders Aligned With All Shareholders?

Investors are always searching for a vote of confidence in the companies they hold and insider buying is one of the key indicators for optimism on the market. This view is based on the possibility that stock purchases signal bullishness on behalf of the buyer. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

It's nice to see that there have been no reports of any insiders selling shares in Bell Equipment in the previous 12 months. Add in the fact that Leon Goosen, the Group Chief Executive & Executive Director of the company, paid R205k for shares at around R12.82 each. Decent buying like this could be a sign for shareholders here; management sees the company as undervalued.

Is Bell Equipment Worth Keeping An Eye On?

Bell Equipment's earnings per share have been soaring, with growth rates sky high. Growth-minded people will be intrigued by the incredible movement in EPS growth. And indeed, it could be a sign that the business is at an inflection point. If that's the case, you may regret neglecting to put Bell Equipment on your watchlist. What about risks? Every company has them, and we've spotted 3 warning signs for Bell Equipment (of which 2 don't sit too well with us!) you should know about.

There are plenty of other companies that have insiders buying up shares. So if you like the sound of Bell Equipment, you'll probably love this free list of growing companies that insiders are buying.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here