Yahoo Finance

Yahoo Finance With EPS Growth And More, Macquarie Group (ASX:MQG) Is Interesting

It's only natural that many investors, especially those who are new to the game, prefer to buy shares in 'sexy' stocks with a good story, even if those businesses lose money. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.'

In contrast to all that, I prefer to spend time on companies like Macquarie Group (ASX:MQG), which has not only revenues, but also profits. While that doesn't make the shares worth buying at any price, you can't deny that successful capitalism requires profit, eventually. Loss-making companies are always racing against time to reach financial sustainability, but time is often a friend of the profitable company, especially if it is growing.

Check out our latest analysis for Macquarie Group

How Quickly Is Macquarie Group Increasing Earnings Per Share?

As one of my mentors once told me, share price follows earnings per share (EPS). Therefore, there are plenty of investors who like to buy shares in companies that are growing EPS. Over the last three years, Macquarie Group has grown EPS by 15% per year. That's a pretty good rate, if the company can sustain it.

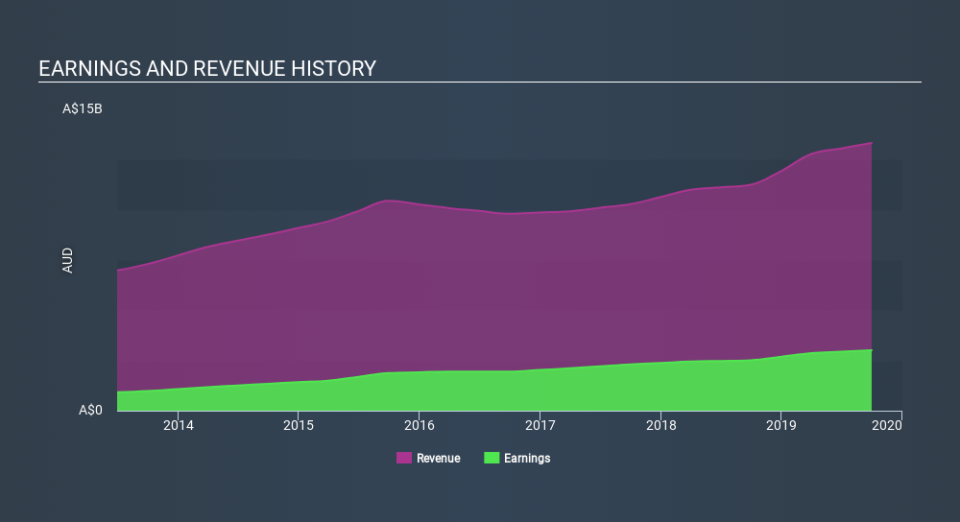

I like to see top-line growth as an indication that growth is sustainable, and I look for a high earnings before interest and taxation (EBIT) margin to point to a competitive moat (though some companies with low margins also have moats). I note that Macquarie Group's revenue from operations was lower than its revenue in the last twelve months, so that could distort my analysis of its margins. While we note Macquarie Group's EBIT margins were flat over the last year, revenue grew by a solid 19% to AU$13b. That's progress.

In the chart below, you can see how the company has grown earnings, and revenue, over time. To see the actual numbers, click on the chart.

While we live in the present moment at all times, there's no doubt in my mind that the future matters more than the past. So why not check this interactive chart depicting future EPS estimates, for Macquarie Group?

Are Macquarie Group Insiders Aligned With All Shareholders?

Like the kids in the streets standing up for their beliefs, insider share purchases give me reason to believe in a brighter future. That's because insider buying often indicates that those closest to the company have confidence that the share price will perform well. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

The good news is that Macquarie Group insiders spent a whopping AU$6.1m on stock in just one year, and I didn't see any selling. And so I find myself almost expectant, and certainly hopeful, that this large outlay signals prescient optimism for the business. Zooming in, we can see that the biggest insider purchase was by CEO, MD & Executive Voting Director Shemara Wikramanayake for AU$5.6m worth of shares, at about AU$120 per share.

On top of the insider buying, it's good to see that Macquarie Group insiders have a valuable investment in the business. Notably, they have an enormous stake in the company, worth AU$383m. This suggests to me that leadership will be very mindful of shareholders' interests when making decisions!

Does Macquarie Group Deserve A Spot On Your Watchlist?

One important encouraging feature of Macquarie Group is that it is growing profits. Better yet, insiders are significant shareholders, and have been buying more shares. That makes the company a prime candidate for my watchlist - and arguably a research priority. You still need to take note of risks, for example - Macquarie Group has 2 warning signs we think you should be aware of.

As a growth investor I do like to see insider buying. But Macquarie Group isn't the only one. You can see a a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.