Yahoo Finance

Yahoo Finance With EPS Growth And More, Mears Group (LON:MER) Makes An Interesting Case

Investors are often guided by the idea of discovering 'the next big thing', even if that means buying 'story stocks' without any revenue, let alone profit. Unfortunately, these high risk investments often have little probability of ever paying off, and many investors pay a price to learn their lesson. Loss making companies can act like a sponge for capital - so investors should be cautious that they're not throwing good money after bad.

Despite being in the age of tech-stock blue-sky investing, many investors still adopt a more traditional strategy; buying shares in profitable companies like Mears Group (LON:MER). Even if this company is fairly valued by the market, investors would agree that generating consistent profits will continue to provide Mears Group with the means to add long-term value to shareholders.

View our latest analysis for Mears Group

How Fast Is Mears Group Growing Its Earnings Per Share?

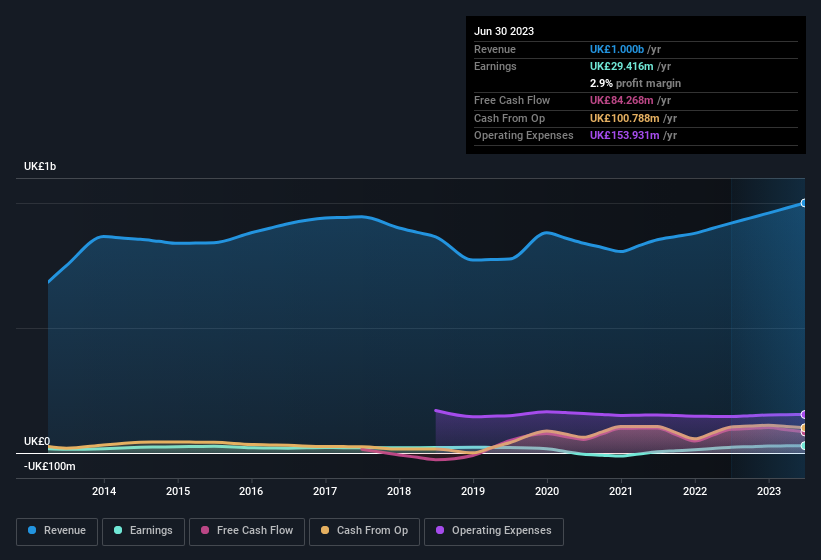

Mears Group has undergone a massive growth in earnings per share over the last three years. So much so that this three year growth rate wouldn't be a fair assessment of the company's future. As a result, we'll zoom in on growth over the last year, instead. Mears Group's EPS skyrocketed from UK£0.20 to UK£0.31, in just one year; a result that's bound to bring a smile to shareholders. That's a commendable gain of 49%.

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. Mears Group maintained stable EBIT margins over the last year, all while growing revenue 8.8% to UK£1.0b. That's progress.

You can take a look at the company's revenue and earnings growth trend, in the chart below. To see the actual numbers, click on the chart.

While we live in the present moment, there's little doubt that the future matters most in the investment decision process. So why not check this interactive chart depicting future EPS estimates, for Mears Group?

Are Mears Group Insiders Aligned With All Shareholders?

It's said that there's no smoke without fire. For investors, insider buying is often the smoke that indicates which stocks could set the market alight. Because often, the purchase of stock is a sign that the buyer views it as undervalued. However, small purchases are not always indicative of conviction, and insiders don't always get it right.

Mears Group top brass are certainly in sync, not having sold any shares, over the last year. But more importantly, Independent Chairman Jim Clarke spent UK£83k acquiring shares, doing so at an average price of UK£2.76. It seems at least one insider has seen potential in the company's future - and they're willing to put money on the line.

Does Mears Group Deserve A Spot On Your Watchlist?

You can't deny that Mears Group has grown its earnings per share at a very impressive rate. That's attractive. The growth rate should be enticing enough to consider researching the company, and the insider buying is a great added bonus. So on this analysis, Mears Group is probably worth spending some time on. Still, you should learn about the 2 warning signs we've spotted with Mears Group (including 1 which makes us a bit uncomfortable).

Keen growth investors love to see insider buying. Thankfully, Mears Group isn't the only one. You can see a a curated list of British companies which have exhibited consistent growth accompanied by recent insider buying.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.