Yahoo Finance

Yahoo Finance If You Like EPS Growth Then Check Out CDL Investments New Zealand (NZSE:CDI) Before It's Too Late

It's only natural that many investors, especially those who are new to the game, prefer to buy shares in 'sexy' stocks with a good story, even if those businesses lose money. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.'

In the age of tech-stock blue-sky investing, my choice may seem old fashioned; I still prefer profitable companies like CDL Investments New Zealand (NZSE:CDI). While profit is not necessarily a social good, it's easy to admire a business that can consistently produce it. While a well funded company may sustain losses for years, unless its owners have an endless appetite for subsidizing the customer, it will need to generate a profit eventually, or else breathe its last breath.

View our latest analysis for CDL Investments New Zealand

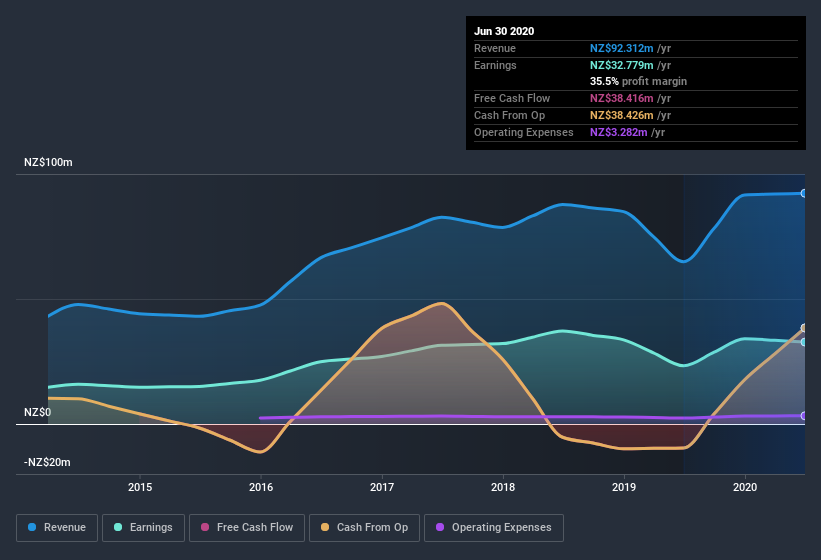

CDL Investments New Zealand's Improving Profits

Even modest earnings per share growth (EPS) can create meaningful value, when it is sustained reliably from year to year. So it's no surprise that some investors are more inclined to invest in profitable businesses. Like a falcon taking flight, CDL Investments New Zealand's EPS soared from NZ$0.084 to NZ$0.12, over the last year. That's a commendable gain of 40%.

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. While CDL Investments New Zealand's EBIT margins are down, it's not all bad news as revenues are, at least, stable. Does that sound particularly bullish? No, it does not.

The chart below shows how the company's bottom and top lines have progressed over time. To see the actual numbers, click on the chart.

Since CDL Investments New Zealand is no giant, with a market capitalization of NZ$286m, so you should definitely check its cash and debt before getting too excited about its prospects.

Are CDL Investments New Zealand Insiders Aligned With All Shareholders?

I like company leaders to have some skin in the game, so to speak, because it increases alignment of incentives between the people running the business, and its true owners. As a result, I'm encouraged by the fact that insiders own CDL Investments New Zealand shares worth a considerable sum. To be specific, they have NZ$27m worth of shares. That's a lot of money, and no small incentive to work hard. That amounts to 9.6% of the company, demonstrating a degree of high-level alignment with shareholders.

Should You Add CDL Investments New Zealand To Your Watchlist?

For growth investors like me, CDL Investments New Zealand's raw rate of earnings growth is a beacon in the night. Further, the high level of insider ownership impresses me, and suggests that I'm not the only one who appreciates the EPS growth. So this is very likely the kind of business that I like to spend time researching, with a view to discerning its true value. Of course, just because CDL Investments New Zealand is growing does not mean it is undervalued. If you're wondering about the valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

Of course, you can do well (sometimes) buying stocks that are not growing earnings and do not have insiders buying shares. But as a growth investor I always like to check out companies that do have those features. You can access a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.